``The highest use of capital is not to make more money, but to make money do more for the betterment of life” - Henry Ford

With the Peso’s impressive gains for 2005, I’ve argued that beyond what is seen (remittances) is a far more important factor in the NOT seen (portfolio flows). And this has been an outgrowth of global excess liquidity in the chase for yields (cash yield premium/interest rate differentials), growing intra-regional economic ties, integration of regional financial markets (e.g. Chiang Mai Initiative ~ currency swaps), dynamic monetary policies (China’s new currency basket) and a technology-enabled “flattening world” which has led to a gradual narrowing of global purchasing power.

As previously argued in my December 5 to 9 edition, (see Philippine Peso Breaks to 2½ High! The Seen and Unseen Variables), ``One must be reminded that the PESO has LAGGED the region such that today’s outperformance could be construed as simply a classic case of cyclical recovery.” In short, a late-in-the-cycle rally for the Philippine currency.

I have received some several quarters or feedbacks about “rising peso hurting our exporters” arguments.

While it is true that appreciating currencies can have to some degree effects that may influence the competitiveness of domestic exports, the ebbs and flows of currencies are NOT the compelling factors in driving export competitiveness.

In the case of

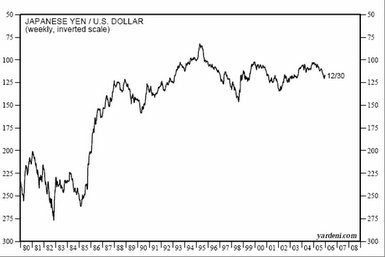

Japanese Yen/USD Historical

Japanese Yen/USD HistoricalAs you can see from the Yen/USD chart above courtesy of www.yardeni.com since sometime 1982 (¥ 275/USD), the Japanese Yen has appreciated by about 140% (!!!!!!!) or 210% (from December 1971 ¥360 to a USD), yet despite the monumental currency appreciation,

According to RTE business,

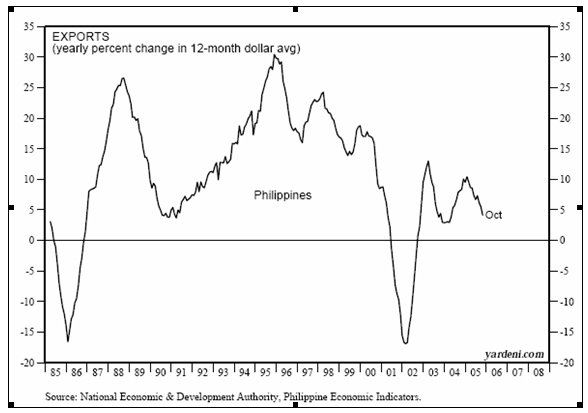

Philippine Exports Yearly % Change

The chart above manifesting of yearly percentage change of local exports courtesy of Dr. Ed Yardeni at www.yardeni.com shows that despite the Peso’s steady depreciation export growth has slowed in recent years or has been in a declining trend since 1995!

What is notable is that the Exports accelerated during the heady expansion days in the early 90’s (ASEAN boom) and collapsed ex-post Asian Financial Crisis!

What could be discerned from the above is that export competitiveness is conspicuously less of an outcome from a depreciating currency, but more of an amalgam of the following: the cost of doing business (infrastructure, wages, etc..), labor productivity, free trade oriented regulations/policies (economic freedom), market access, financial and credit availability, innovative capabilities and cultural acceptance to a globalizing world, aside from macro factors such as aggregate demand, world’s economic growth rate or of the region’s, as well as even monetary policies.

To quote Dr Marc Faber, ``a strong currency has never been a problem in the long run. It forces corporations to become extremely efficient, to innovate and to invent new methods of production. Weak currencies on the other hand are an incentive to compete based on short term favourable exchange rate movements – in nature very much alike protectionist economic policies.”

What could go wrong and offset the present gains are feckless boondoggles masquerading as social service programs meant for short term alleviation and political appeasement which perpetuates the inherent character flaws of the mostly gullible public, particularly of dependency and the client-patronage culture.

For the bankers, I would suggest to aggressively offer instruments on foreign currency hedges to the export/import industry as a niche market.

With the US dollar on a structural downtrend given its unsustainable deficits, foreign currency hedges looks likely a good business to build upon given the juvenile state of the Philippine financial markets.

No comments:

Post a Comment