Yes, I have raised such concern that the Fed may initiate a pause or even a succession of rate cuts on the premise of an adverse US slowdown (see June 5 to 9th edition: US Recession Watch: A Fed CUT in June or August?) highlighted by a continued downdraft by US financial markets benchmarks.

I have also raised the contention that a Fed Pause is likely to occur due to:

One, the political season is back, with congressional elections due later this year, suffering electorates are unlikely to vote for incumbents.

Second, Bernanke’s ideological leanings have been that of the Milton Friedman “monetarist” school of thought, where the salient solution to economic or financial dislocations is to inundate the system with liquidity.

Three, an upcoming economic slowdown or “moderation” under the semantics of the Fed.

Market guru/savant and philanthropist billionaire George Soros foresees a US “hard landing” recession in 2007, AME info quotes Mr. Soros, ``Almost inevitably, they have got to overshoot because they can't stop (raising interest rates) until the economy shows signs of a slowdown. By the time it shows these signs it may be a little too late. I happen to be on the pessimistic side.” So do I.

Except for the 3-month Treasury bills at 4.98% (???), the yield curve has now fully inverted (shorter term yields higher than long term instruments) following the Fed’s 17th rate increase and the decline of the long end of the curve. This marks a restrictive territory for the price of money raising the probabilities of the specter of a recession in the horizon. As for the anomalies in the 3-month Treasury bills, it is said that what keeps its yields from rising is the prevailing onrush to the “flight to quality” mentality.

Yet, a marked slowdown or even a recession is no guarantee of easing inflation as had been in the 70s, ``Economists are also mistaken in their belief that a weakening economy will counteract inflationary pressures. This overlooks the fact that a weakening U.S. dollar will stimulate demand abroad (emphasis mine) at the same time it restrains it here at home. So even as Americans consume less, prices will continue to rise as they are forced to compete with wealthier foreigners for scarce consumer goods.” commented Peter Schiff of Euro Pacific Capital.

In addition, there is a growing popular clamor against such succession of rate hikes. According to the Bloomberg, in a poll conducted by Bloomberg/Los Angeles Times, ``By a 65 percent to 22 percent margin, Americans oppose another rate increase by the central bank, which says such moves are necessary to counter inflation.”

Moreover, while everyone seemed to be focused on rising commodity prices, as the commonly perceived ‘causal’ factor contributing to the groundswell in consumer/producer prices, none has taken into account that rising cost of money (until it stifles demand) has inflationary tendencies too, the amusing Mogambo Guru elaborates, ``And if you think that gingerly raising interest rates will stop a rising inflation, you are wrong, wrong, wrong. Until the rates get so high that they cripple the economy, higher interest rates only produce higher prices, which is de facto inflation: As the producer of goods and services borrows money to finance the on-going business, the higher costs of that borrowing have to be figured into the higher prices of the final output of goods and services so that the business can make a profit. So in the short run, higher interest rates actually cause higher prices. And that's another compelling reason, as if you needed any more reasons, not to let inflation in prices get started by letting inflation in the money supply get started.”

Put differently, raising rates in a measured pace are not going get us anywhere, unless the governing authorities decides to reassert themselves to combat inflation in the truest sense, i.e. regardless of the consequences in the market or the economy, in the same path of the Former Fed Chief Paul Volker in the early 80s or if bond vigilantes compel the Fed to do so by preempting the Fed and sell down US treasuries. However, the magnitude of leverage present in the financial system has had far more consequential impacts relative to the previous regimes as to make it far more parlous.

Finally, immoderate liabilities accrued by the US government will be further burdened by continued rate increases, to quote Daily Reckoning’s Bill Bonner, ``The Fed may want to fight inflation, they say, but its hands are tied. The federal checkbook is overdrawn by some $500 billion this year. In addition, the U.S. Treasury has a trillion-dollar mountain of short-term debt it must refinance in the months ahead. And then, there are the voters themselves, faced with rising interest rates, falling house values and $2.7 trillion worth of adjustable rate mortgages that will be reset in the next 24 months.”

What I am simply saying is that the Fed may succumb to either political or economic or financial pressures or a combination thereof as to take a pause or even reduce its tightening stance. This should, in essence, fuel the anti-US dollar sentiment or dollar diversification theme which would lead to resurgences in the liquidity flows into high return markets as commodities and emerging markets bourses.

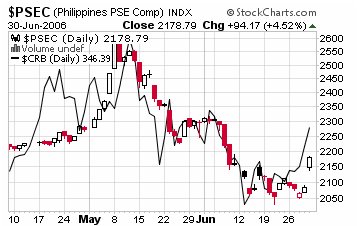

Figure 3 Stockcharts.com: Rebound in Phisix (candle) and CRB Index (line chart)

The recent reaction by the world financial markets practically averred of this phenomenon. Commodities as measured by the CRB index gained 3.4%, Emerging Market stocks rallied mightily, our Phisix climbed an eye-popping 4.5% on Friday to lead Asian bourses on the backdrop of a reversal of foreign outflows seen in most of the week. With Friday’s surge, the Phisix accrued a 3.11% advance over the week.

If the latest “benign Fed” elixir does continue to gain momentum, which I am inclined to think of, we would likely see an interim reversal in the decline of Philippine bonds yields and of the USD/Peso and a rally in the domestic equity market. This will reflect a regional motion, meaning a similar rally in Asian currencies, bond markets and equities.

This does not however write off my long term cyclical view that interest rates will continue to rise in the distant future, underpinned by the well entrenched inflationary variables.

Figure 4 Economagic: Looks like a 40-year trough-to-trough cycle for benchmark treasuries

Figure 4 appears to show of the benchmark US Treasury yields on a 40+ years full trough-to-trough cycle, interspersed into 20+ year trough-to-peak (red arrow), and about 20 years peak-to-trough (blue arrow). The fast shaping advance or trough-to-peak cycle seems to be at work today, despite the recent stimulatory Fed Speak and the stark recoveries across assets in the global financial market.

No comments:

Post a Comment