``Ignoring market risk will mean that, from time to time, performance will be lumpy...The fund is unlikely to outperform benchmarks consistently. Rather, the goal is to outperform on average, most of the time, and over the long run.''- Martin Whitman, manager since 1990 of the $8.3 billion Third Avenue Value Fund.

While I might have been right about rising gold prices, the correlation between non-US equity benchmarks, particularly of the emerging market ones, and rising gold prices appears to have broken down.

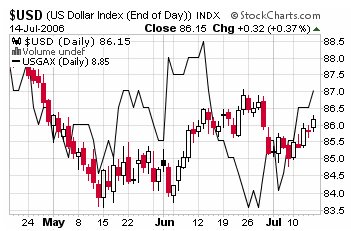

This week, aside from gold and oil, safehaven bets in the US dollar (as measured by its trade weighted index) and US treasuries have rebounded (as measured by Morgan Stanley US Government Securities) as shown in Figure 2.

Figure 2: Stockcharts.com: Rallying US dollar Index and Morgan Stanley Government Securities

In the currency markets, the rise in the US dollar index has resulted to a broadbased decline in Asia’s currencies. The Philippine Peso fell .08% to Php 52.39 against a US dollar from the previous Php 52.35.

The Bond markets have indicated for a slowdown in economic growth and inflation expectations with a hefty decline in US treasury benchmarks across the board. With Fed funds rate at 5.25%, Treasury yields for Notes (2, 5, 10 and 30 years) including the 3-month T-bill have all widened inversions except for the 6-months T-bills which closed basically flat. Aside from signifying a possible slowdown on a tight money backdrop, another Fed hike in August with bond yields at present levels, or a continuing rally in bond prices even at the event of a pause in August, is likely to widen the yield inversion curve growing the risks of a US led recession.

Asian bonds have mostly rallied, including the Philippines. This has likewise been indicative of a possible slowdown of the world economic growth.

Figure 3: kitcometals: Record HIGH for NickelWhile the bond markets suggest of a slowdown in either economic growth or inflation expectations, in the commodities front we are witnessing a strong resurgence following oil’s new highs. Nickel carved out a fresh record high up 15% for the week (see figure 3), followed by a strong finish by copper (+4.7%) silver (+1.1%) and gold (+5.23%). The commodity indices of the CRB-Jeffries closed 2.68% higher to bring year to date gains to about 7.6% while the energy heavy Goldman Sachs Commodity Index surged 3.78% to a NEW record high (see Figure 4)!

Figure 4: Stockcharts.com: Rallying CRB and Record High Goldman SachsContrasting stories, we have here. Unlike in the May selloffs where except for the US dollar all assets had been sold off, today there are emerging dissonances. The bond markets whisper of subdued inflation, and a prospective economic growth slowdown, while the commodity markets remain beneficiaries of the residual inflationary policies. You have a yield curve inversion to reflect a tightened money environment but M2, Bank Credit and Commercial papers continue to expand. You also have rising dollar to corroborate the tightening by central banks however, a rampaging gold offsets this. I have argued to the contrary of the consensus opinion that gold’s fate (see June 19 to 23 edition, Has Gold Found its Bottom? Philippine Mining Index to Lead Phisix Anew?) has not been entirely inversely related to the US dollar. In times of uncertainty, gold and the US dollar may coexist. Not to mention that higher oil prices would translate to more US dollar requirements for oil consuming nations, thereby temporarily propping up the value of the world’s currency reserve.

What does this mixed signal imply? Have the leakages in the financial system found its way to commodities? Are the bond markets wrong? Such that commodities will continue to climb even amidst a muddle through environment and eventually bond yields follows? Or are the commodities markets bound for a belated selloff?

So far one clear indication is that the equity benchmarks have been the unambiguous losers. Global benchmarks have taken a direct hit. Wall Street benchmarks have been significantly down (Dow Jones -3.17%, S & P 500 -2.31%, and Nasdaq -4.35%) and so with most of the world’s major or emerging market benchmarks.

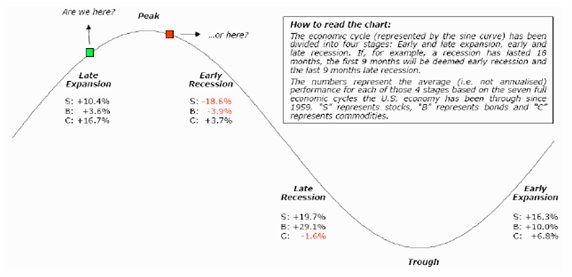

Figure 5: Absolute Partners: Average Returns by stage of the Business cycle

Maybe it depends on the stage of the cycles. According to Niels C. Jensen of the Absolute Partners, based on a study called ``Facts and Fantasies about Commodity Futures1”, by Gary Gorton and K. Geert Rouwenhorst back in 2004 (emphasis mine),

``We make the following observations:

1. As we already pointed out, over an entire economic cycle, stocks and commodities behave quite similarly, at least as far as the total return pattern is concerned.

2. Stocks (and bonds) do much better than commodities in late recessions and early expansions. Late recessions are, in fact, the worst environment for commodities where the average return has been negative.

3. The best environment for commodities is late expansions where the average return both in absolute and relative terms is very attractive.

4. In early recessions, where stock and bond returns really suffer, commodity returns are still quite attractive, at least in relative terms.

``All this leads to the $1 million question: Where in the cycle is the global economy today? Knowing the answer to that may explain the difference between poor and good performance in your portfolio over the next 12-18 months.”

Does the weaknesses in the stockmarkets’ worldwide compounded by the tepid rally in bonds imply that we are now entering into the early stages of a recession? We will see.

One thing I would like to repeat is that the Bernanke Put, i.e. Fed’s willingness to bail out the markets with a flood of liquidity, a possible legacy from Greenspan, remains an open option as argued in my June 5 to June 9 edition, (US Recession Watch: A Fed CUT in June or August?).

Once Wall Street’s benchmarks hit substantial or pivotal lows, you can be assured that not only will the Fed pause but Mr. Bernanke & Co. will embark on an abrupt series of rate cutting spree in fear of “destructive” deflation. The appointment of Henry Paulson formerly top honcho of Goldman Sachs as the Secretary of the US Treasury underscores this interest to protect members of the Financial community. Talk about maintaining special interest groups.

Figure 6: stockcharts.com: Phisix in a Predicament

Finally, relative to the Phisix, it was a curious episode for the Philippine benchmark to rally significantly last Thursday despite the steep losses in Wall Street, which made me think that the gold-phisix correlation could be at work. However, the failure of the mines to perk up gave me less confidence for this outlook. Friday’s 2.27% drop basically reflected the loss of the week (down 2.12%) and validated my doubts. Although, it is too early to call off the relationship: One day or week does not a trend make.

On the fundamental side, Japan’s first interest rate hike in 6 years was accompanied by placating statements of “no intention” of raising rates at consecutive meetings which implies of an orderly pace of tightening. This should reduce the probabilities of a precipitate margin based liquidations of financial assets worldwide.

Second, while my outlook remains for a dovish Fed stance in the face of a deteriorating equity market and softening economy, a continued rally in the commodity markets would most possibly filter into emerging market bourses eventually. If the business cycles study above by Mr. Gary Gorton and K. Geert Rouwenhorst replays itself then possibly commodities are still the place to be in and so with emerging market bourses.

Based on the technical perspective, the outlook remains mixed. Over the short-term especially on Monday, the Phisix may replicate the activities in Wall Street anew and do some backing and filling jobs as it had broken support see Figure 6. The gaps which it had opened would be most likely closed while at the same time trade within the 50-day moving averages (red line) and 200-day moving averages (blue line) over the interim.

I expect some tradeable opportunities in the market despite some interim pressures, simply buy and support and sell on resistances. Keep some long positions on mines and oil for insurance purposes.

No comments:

Post a Comment