``The Masses have never thirsted after truth. They turn aside from evidence that is not to their taste, preferring to deify error, if error seduce them. Whoever can supply them with illusions is easily their master; whoever attempts to destroy their illusion is always their victim.” -Gustave Le Bon, The Crowd

As we have noted last week, “Markets make Opinion”, where “experts” and journalists in complicity draw up to form what is known as the “conventional wisdom”, a simplified explanation for market causalities.

First, the public including local mainstream experts have the tendency to be guided by the “recency bias” or the “rear view mirror” or “anchoring” syndrome, where they extrapolate the most recent past and project them into the future.

Second, the lack of perspective, our experts have been inclined to cite whatever headlines in order justify today’s market’s action. In behavioral finance, such is called “rationalization”.

Third, as we noted last week, it’s all about incentives; the merrier the market, the appearance of a more risk-free environment encourages “experts” to amplify the short-term risk appetites of the average investors.

Yet flurries of short-term trades or overtrading are manifestations of the folly of overconfidence; one of the major reasons why the average investors are left to hold the proverbial empty bag when the cycle reverses.

Nonetheless, such pressures for short-term gains come irrespective of potential risks. Typical brokers encourage investors towards more technical approach to the market, in order to whet their appetites for greater turnovers.

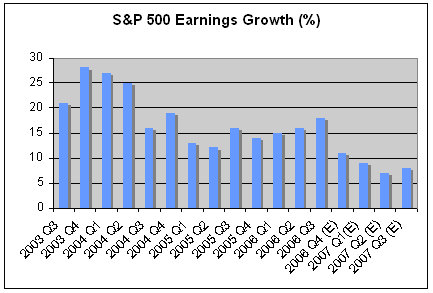

Anyway, Figure 5 is a chart from the normally Panglossian research outfit, the Taipan group which dissects upon the effects of an economic slowdown combined with a declining trend of corporate earnings in the US to the possible performance of US markets in 2007.

Figure 5: Taipan Group: The Coming Earnings Crunch

Let me quote Steven Lord, editor of the Trend Investor of the Taipan Group (emphasis mine), ``The above chart, tracking the earnings of the S&P 500 since the middle of 2003 and applying estimates through the third quarter of 2007 from Thomson Financial, shows the steady decline in year-over-year percentage gains. Companies in the S&P have expanded earnings at a double-digit pace for the last 13 consecutive quarters -- or for the last three years....This leaves the stock market, perched as it is close to record levels, with only one way to move higher -- multiples have to expand. In other words, for stocks to rise significantly from here investors will have to pay “more” for a dollar of earnings in 2007 than they did in 2006, via a re-rating of the market’s overall P/E ratio. With earnings trending down and the economy slowing, awarding a higher P/E ratio is the only way for the market to rise from here. While not impossible -- at roughly 15, the market is hardly overvalued on a P/E basis -- it is clearly a higher risk strategy than we have seen for the past few years.”

Higher price multiple implies for richer valuations which makes today’s approach to the equities market clearly a higher risk strategy as Mr. Lord warns. Yet momentum remains tilted towards an acceleration of prices regardless of economic realities, where multiples could even reach bubble-like proportions as in 2000.

Markets can stay irrational longer than you can remain solvent says the illustrious economist John Maynard Keynes. Yes, today’s market environment may even surprise hard-core technicians that prevailing euphoric sentiments could lead to parabolic or sharply vertical moves; a speculative blowoff top in spite of present risks.

Considering the high-risk proposition of today’s market climate, it is probably best to simply keep your present positions and avoid overtrading and anteing up heavily by chasing prices.

Since the market has palpably been rotating it would be of lesser risk to employ risk capital to issues that have lagged, and hope for a contagion, i.e. if the itch to join the bandwagon trade becomes irresistible. Here position sizing greatly matters.

Moreover, one must keep in mind the basic market tenet that NO TREND GOES IN A STRAIGHT LINE. Such that while I remain bullish with the SECULAR or long term trend cycle of the Phisix, current conditions have raised the risk profile for investors to warrant a more cautious approach to the market.

It is also recommended or advisable to employ the practice of TIGHTENING of your STOPS in case the market does unwind. Remember, the steeper the market climbs, the harder its potential fall.

No comments:

Post a Comment