An election is a moral

horror, as bad as a battle except for blood; a mud bath for every soul

concerned in it—George Bernard Shaw

In this issue

Fear the ‟Trump Trade‟ or a Pushback on Fed Policies? Trump or Harris: The Era of the Bond Vigilantes is Upon us

I. US Election Narrative: Fear the Trump Trade!

II. Market Chaos Erupts after Fed’s September Rate Cut

III. Global Economic War and the Inflation Scorecard: Trump versus Biden-Harris; Trump’s Tariffs as Negotiation Card

IV. Emerging Market and ASEAN Stocks, the PSEi 30 Hit a Record High in Trump’s Term, Philippine Peso Flourished Under Trump!

V. The Biden-Harris Legacy of "Proxy Wars"

VI. Trends in Motion Tend to Stay in Motion: World War III’s Multifaceted Aspects

VII. Global Kinetic Warfare

and the Cold War as Products of the Fed’s and Global Central Bank’s Easy Money

Regime

VIII. Conclusion: Trump or Harris: The Era of the Bond Vigilantes is Upon Us

Fear the Trump Trade or a Pushback on Fed Policies? Trump or Harris: The Era of the Bond Vigilantes is Upon us

Is the "Trump Trade" responsible for recent market convulsions, or does this represent a pushback against the Fed’s actions? Why political-economic trends in motion tend to stay in motion.

I. US Election Narrative: Fear the Trump Trade!

Trump's Rising Election Odds Sends Emerging Markets Into Tailspin, Causes Biggest Stock Drop In 10 Months (Yahoo, October 27)

The Bangko Sentral ng Pilipinas (BSP) might have to do more to support the Philippine economy if former US President Donald Trump returns to power and starts a global trade war, which can hurt the entire world and, in turn, dim local growth prospects. (Inquirer.net, October 28, 2024)

THE RETURN of Donald J. Trump to the US presidency could cause Asian currencies such as the Philippine peso to weaken, analysts said. (Businessworld, October 29, 2024)

At first glance, it may seem that the following headlines or excerpts were conveyed for Halloween.

Then, I realized that the U.S. elections are coming up this week.

Mainstream media has painted an impression that the recent setbacks in the marketplace mean that a Trump win/presidency, or the "Trump Trade," could be detrimental to the markets.

Let us examine what led to this perspective.

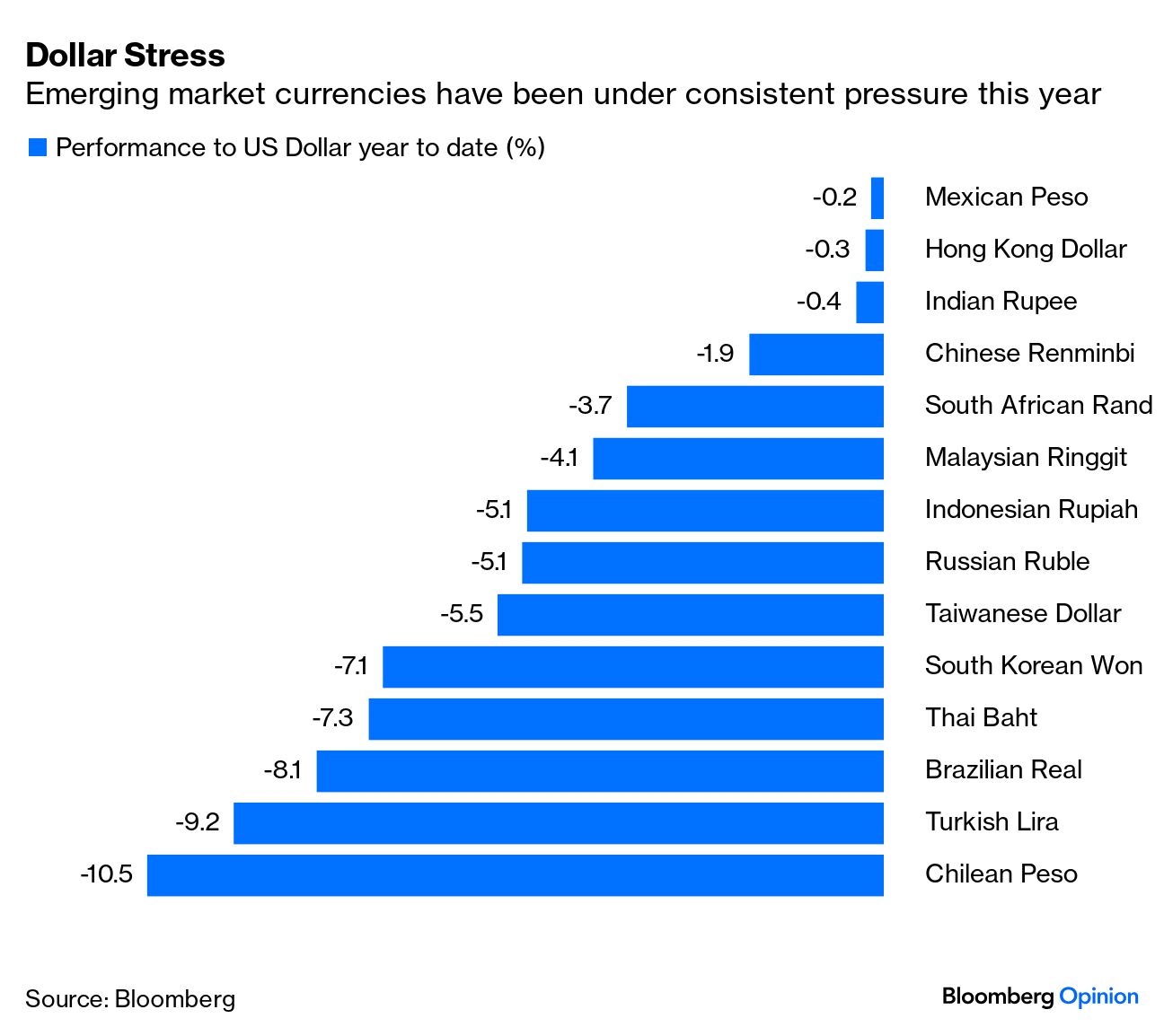

In October, the Bloomberg spot U.S. dollar index surged by nearly 3% compared to the previous month. The S&P 500 slipped by 0.99%, the iShares MSCI Emerging Market ETF (EEM) dived by 3.07%, and the Global X FTSE ASEAN ETF (ASEA) tanked by 3.9%. The U.S. 10-year Treasury yield surged by 48 basis points (12.7%).

Meanwhile, at home, the Philippine peso plunged by 3.6%, and the PSEi 30 plummeted by 1.78%.

The prevailing sentiment in the speculative marketplace has shifted from excessive optimism to risk aversion.

Who else to blame but the leading contender in the prediction markets, Trump!

II. Market Chaos Erupts after Fed’s September Rate Cut

But does this widely accepted perception accurately reflect causation, or is it intended to shift the Overton Window in favor of the opposing contender, Kamala Harris?

Figure 1

The rising 10-year yield actually started just after the US Federal Reserve initiated its 50-basis-point rate cut on September 18th. (Figure 1, topmost chart)

It is rare to witness such a combination of powerful forces ripple through other market indicators.

Figure 2

Rising Treasury yields have been accompanied by an appreciating U.S. dollar index, which has also contributed to increased volatility in the bond market (MOVE Index) and volatility premiums across asset markets—including equities, oil, and foreign exchange—as well as a spike in U.S. Credit Default Swaps (CDS). (Figure 1, middle and lower graphs, Figure 2 topmost and lower images)

Figure 3

This dynamic coincided with a spike in the Economic Surprise Index and gold's widening outperformance against the TLT iShares 20-Year U.S. Treasury bond prices. (Figure 3, middle topmost and middle visuals)

Incredible.

The most striking indicator of the impact of the Fed's rate-cutting cycle that began in September is that it occurred under the loosest financial conditions since at least December 2022. (Figure 3, lowest diagram)

In other words, global financial markets have significantly pushed back against the Fed’s easing policy by effectively re-tightening conditions!

Of course, one could interpret this as "buy the rumor, sell the news."

Still, other factors are at play—such as unrestrained public spending, surging debt levels, escalating debt servicing costs, geopolitics and more!

Nevertheless, resonating with the "Overton Window" during the pandemic in support of lockdowns and vaccines, the Gramsci-cult elite-controlled media shifted the rhetoric to blame Trump’s predilection for tariffs.

III. Global Economic War and the Inflation Scorecard: Trump versus Biden-Harris; Trump’s Tariffs as Negotiation Card

First and foremost, yes, while it is true that global trade restrictions did rise in during Trump 1.0 (2017-2021) regime, his successors, the Biden-Harris tandem, pushed for MORE trade barriers, which hit a record high in at least 2022!

Figure 4

As the IMF chart reveals, the global economic conflict spans both parties, with both candidates appearing inclined toward de-globalization.

(Note this shouldn’t be seen in a simplistic lens but related to geopolitical developments)

Second, financial easing amidst the loosest monetary conditions translates to a potential comeback of inflation, which aligns with the perspective that Trump’s trade war results in higher inflation.

However, that shouldn’t hold water; inflation under Trump’s administration was milder than the inflation epidemic during the Biden-Harris administration.

Consequently, with higher inflation came higher interest rates as well.

Third, Trump’s push for tariffs represents a carryover from his 2016 campaign trail.

He used tariffs as leverage for negotiation but eased up on strict currency regulations, as noted in this Yahoo article.

Trump has likened his tariff plan to a new "ring around the collar" of the US, with tariffs often described not as part of negotiations but with those high duties as an end goal in themselves to protect US industry…

He promised during that campaign to impose tariffs, renegotiate NAFTA, and withdraw from the Trans-Pacific Partnership. "Promise kept," PolitiFact said of all three.

Trump also took action on a fourth promise to declare China a currency manipulator but ended up compromising, according to the group.

IV. Emerging Market and

ASEAN Stocks, the PSEi 30 Hit a Record High in Trump’s Term, Philippine Peso

Flourished Under Trump!

Figure 5

Fourth, stock markets haven’t been exactly hostile to Trump.

The ASEAN ETF (ASEA) reached an all-time high in 2018 or during the early phase of his administration, and the Emerging Markets ETF (EEM) also hit a milestone that year and also surged to a fresh record toward the close of Trump’s term. Both markets, however, eventually succumbed to the pandemic recession.

Similarly, the Philippine PSEi 30 hit a significant peak in January 2018, also coinciding with Trump’s administration.

On the currency front, the Philippine peso rallied from October 2018 to the end of 2021.

In fact, contrary to contemporary analysis, the USDPHP fell by 3.7% from January 20, 2017, to January 20, 2021 (Trump’s tenure).

In contrast, under the Biden-Harris administration, the USDPHP has increased by an astounding 21% from January 20, 2021, to the present (October 31, 2024)!

While past performance does not guarantee future outcomes, the scorecard between the contending parties shows a stark difference in the accuracy of the current predominating narratives.

In a word, propaganda.

Nota Bene: Past performance is not a guarantee of future results. Our purpose is to highlight inaccuracies in media claims. We don’t endorse any candidates.

V. The Biden-Harris

Legacy of "Proxy Wars"

Fifth, the world is on the brink of, or already embroiled in, a form of World War III, fought across multiple spheres.

The U.S. suffered a humiliating defeat in the 20-year Afghanistan War, ultimately withdrawing in the face of a relentless war of attrition led by the Taliban’s guerilla tactics. Both the Trump and Biden administrations negotiated withdrawal terms, but the Biden-Harris administration oversaw a controversial chaotic exit in August 2021.

That aside, a series of conflicts has marked the Biden-Harris administration’s legacy.

The kinetic conflict began with the Russia-Ukraine war in 2022, spread to the Israel-Palestine/Hamas war in 2023, and has since escalated to include confrontations involving Israel-Hezbollah or the "Third Lebanon War," and even the precursory phase of Israel-Iran Conflict in 2024.

Simultaneously, following Obama’s failed "Pivot to Asia," geopolitical tensions have been mounting in the Taiwan Straits, the South China Sea, Central Asia, and other parts of the world.

Notably, these ongoing and emerging conflicts are interconnected.

For example, the U.S. has been supplying not only aid but also arms to its allies to counter hegemonic rivals.

Figure 6

Aside from supplying 70% of conventional weapons, U.S. military aid/grants to Israel soared to all-time highs in 2024! (Figure 6, topmost chart)

That is to say, the current conflicts represent "proxy wars" where the U.S. led NATO forces engage indirectly to pursue hegemonic objectives.

VI. Trends in Motion Tend to Stay in Motion: World War III’s Multifaceted Aspects

The Global Warfare has also entered the economic and financial spheres—seen in the weaponization of the U.S. dollar through asset confiscations targeting so-called "axis of evil" nations, and in the reinforcement of a modern-day "Iron Curtain" marked by significant restrictions on trade, investments, capital flows, and social mobility.

Mounting trade imbalances, which helped fuel the rise in trade barriers from the Trump administration to Biden-Harris, have also laid the groundwork for today’s outbreak of kinetic conflicts.

Geopolitical tensions have surfaced as a growing cold war in other regions as well.

This hegemonic competition to expand sphere of influences has percolated to Africa, Latin America, the South Pacific, and the Global South (BRICs), some of which channeled through mercenary or gang wars and local civil wars. (Dr. Malmgren, 2024)

Ironically, four of the five ASEAN majors, specifically, Indonesia, Thailand, Malaysia and Vietnam recently signed up for the BRICs membership.

The implicit cold war has also extended into previously uncharted areas: underwater territories, space, the Arctic, the Pacific, mineral resources (like rare earth elements), and technological domains such as DNA research, cyberspace, and microchips (Malmgren, 2023).

The point is that these evolving conflicts underscore the interconnectedness of U.S. foreign and domestic policy.

Given the powerful forces behind this trajectory or the "deep state"—including the Military-Industrial Complex, the National Security State, Straussian neoconservatives promoting the "Wolfowitz Doctrine," the energy industrial complex, Big Tech, and Wall Street—it is unlikely these developments will cease, whether under a Trump 2.0 administration or (Biden carryover through) a Harris regime.

Put simply, while media narratives may further lobotomize or impair the public’s critical thinking, potentially deepening societal division, a meaningful change in the U.S. and global sociopolitical and economic landscape remains unlikely if elections continue to focus on what I call as "personality-based politics."

As investor-philosopher Doug Casey rightly observed, "Trends in motion tend to stay in motion until they reach a crisis."

VII. Global Kinetic Warfare and the Cold War as Products of the Fed’s and Global Central Bank’s Easy Money Regime

Lastly, the public tends to overlook that current trends are merely symptoms of deeper issues or mounting disorders stemming from the decadent U.S. dollar standard.

As investor Doug Noland astutely wrote

Bubbles are mechanisms of wealth redistribution and destruction – with detrimental consequences for social and geopolitical stability. Boom periods engender perceptions of an expanding global pie. Cooperation, integration, and alliances are viewed as mutually beneficial. But late in the cycle, perceptions shift. Many see the pie stagnant or shrinking. A zero-sum game mentality dominates. Insecurity, animosity, disintegration, fraught alliances, and conflict take hold. It bears repeating: Things turn crazy at the end of cycles. (bold mine) [Noland, 2024]

Easy money has long fueled, or been instrumental in financing, the global war machine, leading to today's bellicose conditions.

Easy money has also powered the growth of big government and contributed to economic bubbles and their eventual backlash, as evidenced by China’s unparalleled panicked bailout policies to prevent a confidence crisis from imploding.

The push for easy money is likely to persist, whether under a Trump 2.0 or a Harris administration.

As Professor William Anderson noted,

The unhappy truth is that both platforms will need the Federal Reserve System to expand its easy money policies, despite the massive damage the Fed has already done by bringing back inflation. While Harris claims to defer to the “experts” at the Fed, Trump wants the president to have more power to set interest rates. Obviously, neither candidate is acknowledging the economically perilous situation in which the government ramps up spending, which distorts the markets, and then depends upon the Fed to monetize the resulting federal deficits. As the debt grows and the economy becomes progressively less responsive to financial stimulus, the threat of stagflation grows. The present path of government borrowing and spending all but guarantees this outcome, and the candidates have neither the political will nor the economic understanding to do what needs to be done. (Anderson, 2024)

U.S. debt is fast approaching $36 trillion, while global debt reached $315 trillion in Q2 2024 and counting. (Figure 6, middle and lower charts)

"Trends in motion tend to stay in motion until they reach a crisis."

VIII. Conclusion: Trump or Harris: The Era of the Bond Vigilantes is Upon Us

While the "Trump trade" provides a convenient pretext for the current tremors in the global financial market, this narrative relies on inaccurate premises and misleading speculative claims that are unsupported by empirical evidence. Instead, these assertions aim to sway the voting audience ahead of this week’s elections.

In contrast, the current financial market convulsions reflect a significant pushback against the Fed’s and global central banks’ prolonged easy-money policies. As investor Louis Gave of Gavekal recently noted, "Zero rates were a historical aberration that need not be repeated."

Needless to say, regardless of who wins the U.S. presidency, political agendas will continue to advocate for easy money and various forms of social entropy and conflict.

Unfortunately, there is no such thing as free lunch forever.

Although trends in motion tend to stay in motion, the era of the bond vigilantes is upon us.

Things have been turning a whole lot crazy.

___

References

Yahoo Finance, What Trump promised in 2016 on tariffs. And what he delivered (a lot). October 28, 2024,

Dr. Pippa Malmgren The Cold War in Hot Places, March 12, 2024

Dr. Pippa Malmgren WWIII: Winning the Peace, October 28, 2023 drpippa.substack.com

Doug Noland, Vigilantes Mobilizing, Credit Bubble Bulletin, November 1,2024

William L. Anderson The Great Retreat: How Trump and Harris Are Looking Backward, August 30, 2024 Mises.org

Louis-Vincent Gave, Behind The Bond Sell-Off, Evergreen Gavekal October 31, 2024

{kind=link}