Yuan’s Dollar Unpegging Opens Portals for Philippine Economic Advancement

A kaleidoscope of earthshaking global events has failed to take away the limelight from the unwarranted fixation of Filipinos on domestic politics. The terror bombings in Egypt, whose causalities have climbed to 88 fatalities as of this writing and the second series of bombings in London and most importantly, the seismic ‘Yuan revaluation’ or the depegging of the Chinese currency from the US dollar for the first time in more than a decade which is now the du jour topic of the global financial markets.

While the Yuan’s peg has been adjusted by only 2.1% from 8.3 to 8.11 to a US dollar, the move towards a “managed exchange rate regime” alters the framework of its peg from the US dollar to a “basket of currencies” which almost similar to the Singapore dollar model. Second, the currency is now allowed to float within a trading band of +/- .3 percent, with the closing prices determined at the end of the trading day.

What is so significant about the Yuan? According to Morgan Stanley Chief Economist Stephen Roach ``China’s fate is tied far too closely to that of the US. Its export-led growth is dependent on the American consumer; at least a third of all Chinese exports go to the US. Moreover, China’s currency, the renminbi, has been pegged to the US dollar for over a decade. This means the monetary policies of the People’s Bank of China and the Federal Reserve are joined at the hip.” Moreover, according to Andy Xie Asian analyst also for Morgan Stanley ``China has become the biggest trading partner for most East Asian economies, and it has substantially increased its influence in the region.”

In other words, in the context of global trade dynamics, the symbiotic relationship of China, as the world’s principal supply chain, and the United States, as the world’s premier consumer, has been implicitly shaped by an interlocked monetary policy as evidenced by the Yuan/Remimbi peg to the US Dollar. This implies that with the current move to wean away from its interdependence to the US dollar, China is finally adopting an independent monetary policy! In this instance, the central banking skills of the People’s Bank of China (PBOC), China’s central bank, will finally be tested and most importantly, we could probably be at the cusp of a major global structural trade, financial and economic adjustment that essentially would be deal with the extant imbalances that threatens the global economy.

It is true that while the revaluation is miniscule relative to the expected adjustments (anywhere from 15 to 30%), the PBOC is anticipated to adopt ‘baby steps’ in its transition to the new exchange regime, possibly to avoid the risks of having massive disruptions or dislocations in the financial markets that may ripple to the global economy. Further, it is my view that the gradual steps are part of the Chinese central bankers’ learning or experience curve as quasi-independent policy makers.

It is also possible that the recent moves to adjust its currency could be a political statement in response to the souring relationship with Washington as threats of legislated protectionism, particularly the Schumer-Graham China Currency Act (S. 295) which would slap 27.5% tariffs on Chinese imports, are poised to undermine global trade flows. China needs those jobs badly as rising unemployment or displaced workers from former state owned enterprises could stir political instability that may overwhelm the Communist ruling party’s survival (Sounds familiar?).

What’s in it for the financial markets? For one, the diversification away from the US dollar and the pegging to a basket of currencies are definitely bearish indicators for the US dollar and US treasuries.

|

|

| 2004 |

|

| Country | in $ Million |

| 1 | United States | 169,626.20 |

| 2 | Japan | 167,886.40 |

| 3 | Hong Kong | 112,678.40 |

| 4 | South Korea | 90,068.20 |

| 5 | Taiwan | 78,323.80 |

| 6 | Germany | 54,124.30 |

| 7 | Singapore | 26,683.90 |

| 8 | Malaysia | 26,261.10 |

| 9 | Netherlands | 21,488.60 |

| 10 | Russia | 21,232.00 |

Table courtesy of USChina.org

If there would be any clue to the inscrutable ‘basket of currencies’ peg recently adopted by the PBOC, the above table shows of China’s top 10 largest trade partners, which posits that the US $ and Japan ¥ would get a bigger share of the basket pie while Asian Currencies may dominate the basket.

As the Yuan appreciates the cost of imports from China are likely to expand thereby increasing headline inflation pressures in the US. Further, the new Yuan peg construct essentially diminishes China’s need to recycle its trade surpluses to US treasuries, and as well, may raise the odds for a shift out of the US dollar. This in effect removes the artificial bid to the US dollar denominated assets which has, thus far, provided subsidy to the low interest regime in the US today. The lifting of the subsidy would translate to probable cutbacks on US treasury purchases that may lead to falling bond prices or higher yields suggestive of higher interest rate environment which may test the resiliency of the asset-dependent heavily indebted US consumers. Malaysia’s lifting of its ringgit-US dollar peg, just hours after China’s promulgation, may yet underscore this.

For China, the 2.1% revaluation is less likely to affect their economy, since the wage and cost differentials are only a fraction relative to US standards.

Second, after applying administration policies to unsuccessfully slowdown growth to lower the risks of overheating, the revaluation could have been also used as an instrument to temper the fast clip growth momentum as well as to reduce inflation. China’s GDP accelerated to 9.5% in the second quarter, ``spurred by a $39.6 billion trade surplus, rising consumer spending and investment in power plants, mines and factories. The faster-than- expected growth suggests Asia's second-largest economy can withstand a stronger currency, which will make the nation's exports more expensive overseas.” observes Bloomberg’s James Regan.

Further, the tensions arising from its inability to sterilize excess money in buying US dollars in its monetary system may have the heightened risks of excess credit creation as manifested by the emergence of ‘assets bubbles’ and mounting inflation. The revaluation basically gives China an ample room to exercise monetary tools for flexibility purposes.

Third, China’s government has taken steps to increase outflow of capitals prior to the recent revaluation. This is clearly visible with China’s encouragement of its endogenous companies to invest overseas such as Lenovo’s latest acquisition of an IBM division, Haier’s (China’s largest home manufacturer) bid for Maytag (the struggling maker of Hoover vacuums), and the controversial China’s CNOOC (China National Offshore Oil Corp.) tender for Unocal.

The other related notable capital outflow policies are the raising of the limits on the amount of money that students and tourists can bring abroad, as well as the current process of loosening restrictions and repatriation of money for foreign owned companies in China. This implies that China intends to use much of its foreign currency reserves to support its financial sector, secure energy and raw materials, and to expand overseas through acquisitions for brand expansion, distribution channels or showcase their management skills.

Lastly, given the present economic realities such as the surplus capacities brought about by excess business and government investments, rising costs in the coastal areas, transportation bottlenecks, shortage of oil and electricity, China’s present thrusts, according to Simon Hunt of Simon Hunt Strategic Services as excerpted by John Maudlin seems to revolve around ‘focusing on business profitability’, ‘return on capital investment’, ‘value added’ ventures (new technology, more expenditures on R&D and etc.), and expanding inland or rural sectors ``where transport systems have improved, where land costs are a fraction of that in the coastal cities and where wages are one-third or less.” These disadvantages open the doors for opportunities among the region’s low cost producers and other emerging market economies.

Naturally, an appreciating Yuan would translate to more expensive exports for China while reducing import costs that may yet stimulate its domestic demand.

For manufacturing companies in South Korea, Japan and Taiwan, capital investments may shift to lower cost production countries such as Vietnam, India or other emerging economies. Yet if domestic consumption will be augmented by the China’s currency appreciation then regional trading opportunities will undoubtedly accelerate. Further, the trend suggests (as can be seen by China’s table of top trading partners above) that inter-regional ties would likely deepen as trade and investments expand.

For a region that holds about 60% of the world’s population supported by 70% of the global currency reserves, it is of no doubt why our paragon benevolent dictator Mr. Lee Kuan Yew, Singapore’s former Prime Minister in his latest article ‘Rising Asia’ in Forbes forecasts that ``The inevitable surprises will occur, but both China and India are on course for a revival of their glorious civilizations. By 2050 the world's economic center of gravity will move from the Atlantic to the Pacific and Indian oceans.”

Meanwhile, the US is unlikely to recover the hollowed out manufacturing capacities it has lost to the outsourcing/offshoring phenomenon given that its relative price structure is still way above China and the emerging market economies even considering a 30% revaluation of the Chinese currency.

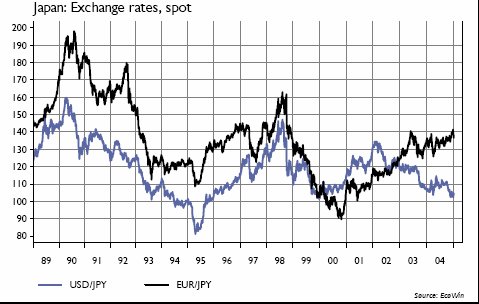

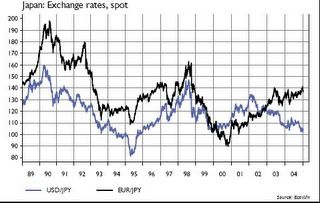

Japan Yen Spot Rates 1989-2004

If history could be a gauge then Japan’s remarkable appreciation from about 150 yen (USD/JPY) in 1998 until 110 today for a 26% rise has not stanched the tide of surpluses in favor of Japan, as shown in the chart above, courtesy of Gavekal Notebooks, “Japanese equities will do a lot better than the economy”. Japan’s foreign currency reserves is the world’s largest for the 67th straight month for June, according to Forbes at US$843 billion and is the largest US Treasury holder at $687.5 billion (May 2005) according US Treasury Department!

To aptly quote Dr. Faber, ``Quite frankly I do not understand the thinking of central bankers. Either they think that a strong currency is a problem or they think that weak currency is a problem. The world would be better off if central bankers collectively resigned and let the market fix exchange rates. Then there would never be a problem, in my opinion. In addition, a strong currency has never been a problem in the long run. It forces corporations to become extremely efficient, to innovate and to invent new methods of production. Weak currencies on the other hand are an incentive to compete based on short term favourable exchange rate movements – in nature very much alike protectionist economic policies. I think the Yen could appreciate to one US$ equal 1 Yen and the Japanese would still have a trade surplus with the US.”

Finally, the Yuan revaluation essentially opens the economic opportunity portals for emerging market economies as the Philippines to take advantage of. While most of us Filipinos are still trapped in the arguments of personality based politics and instant gratification solutions to our economic and financial problems, here we are faced with opportunities to recover our senses, wits and dignity. Simply put, here is the opportunity, what do you do?

``Count your blessings. Once you realize how valuable you are and how much you have going for you, the smiles will return, the sun will break out, the music will play, and you will finally be able to move forward the life that God intended for you with grace, strength, courage, and confidence." Og Mandino, American Essayist and Phychologist, 1923-1996