Deficit-to-GDP ratios decline as the nominal values of the economy’s output and of tax bases generally rise, generating more revenues, while spending—often set in nominal terms in the budget—initially fails to keep up…The early decline in deficits as a share of GDP may not last in the medium term, however, as inflation becomes expected, spending catches up, and the cost of borrowing rises as investors require an inflation risk premium and central bank policy rates are hiked. However, an unexpected bout of inflation will erode part of the real value of government debt persistently, both owing to the initial improvement in fiscal balances and the nominal GDP denominator effect. The effect of inflation also depends on the size of government debt. The larger the debt, the greater potential erosion from inflation…However, unlike inflation surprises, rises in inflation expectations are not associated with a fall in debt ratios, suggesting that inflating debt away is neither a desirable nor a sustainable strategy. Unexpected inflation may offer some breathing room for debt ratios but attempts to keep surprising markets and economic agents have historically proven futile or harmful—Daniel Garcia Macia: IMF Working Paper

In this issue:

BSP’s Off-Cycle/Emergency Hike was about Protecting Deficit Spending via the Philippine Peso

I. BSP’s Off-Cycle/Emergency Hike: It’s about the Peso; BSP versus the NEDA

II. BSP’s Off-Cycle Hike: It’s Primarily Protecting Deficit Spending, 9-Month Deficit Neared the 2022 Levels

III. The Inflationary Potentials from the Capping the USDPHP to Pave Way for Fiscal Dominance

IV. Central Banks are "Dead Wrong:" The USD-Php Could Break the Php 57 level and Power a Rapid Advance

BSP’s Off-Cycle/Emergency Hike was about Protecting Deficit Spending via the Philippine Peso

The latest BSP's off-cycle hike was an emergency move to support the Philippine peso and protect public boondoggles via deficit spending.

I. BSP’s Off-Cycle/Emergency Hike: It’s about the Peso; BSP versus the NEDA

In what they called an "off-cycle decision," the BSP raised its policy interest rate by 25 bps this week.

Inquirer.net October 27, 2023: As its chief had hinted, the Bangko Sentral ng Pilipinas (BSP) resumed hiking its policy rate in an off-cycle decision on Thursday, with the possibility of further tightening in a bid to bring inflation back to target as price pressures continue to build…It was a move that BSP Governor Eli Remolona Jr. had repeatedly telegraphed to the market a few days ahead. The MB was not supposed to convene for a policy meeting until Nov. 16, but Remolona said the BSP “recognized the need for this urgent monetary action” after inflation sizzled to a four-month high of 6.1 percent in September on the back of expensive food items…But Remolona believes the aggressive tightening “has not really affected growth prospects,” adding that the slowdown was mainly due to “waning” of pent-up demand that boosted consumption when the world emerged from pandemic lockdowns. “Monetary policy cannot control supply-side shocks but it can serve to break the link between supply shocks and expectations,” the BSP boss said. “Those supply shocks and second-round effects like transpo fare hikes, that’s what we worry about.”

The BSP chief bumped heads with NEDA's bigwig, who cautioned against further rate hikes.

Philstar.com October 26, 2023: Supply-side driven inflation does not need a monetary response from the monetary board (MB), National Economic and Development Authority Secretary Arsenio Balisacan said…Earlier, Balisacan, who is not a member of the MB, said that further interest rate hikes can further hurt consumers as the country suffers inflation. “There’s really no urgency in creating another round of high-interest rates,...higher interest rates will really put us too far away from our peers in the region,” Balisacan said in an October 5 briefing.

Though "telegraphed, " this "off-cycle" hike—meaning a decision made outside the traditional Monetary Board (MB) policy corridor—signaled alarm: "urgent monetary actions."

Why hike ahead of the MB meeting when everything seems under control? Did the 6.1% September CPI incite this? If so, why have they not implemented it shortly after its announcement? Or could there have been other factors?

The thing is, the decision to hike emerged out of perceived "emergency" conditions.

Yet, authorities appear to engage in the fudging of the actual conditions of the economy. For instance, the use of technical balderdash—"serve to break the link between supply shocks and expectations"—in explaining to the lay public seems disingenuous.

How the heck can higher rates break the link between supply shocks and expectations??? What serves as the crucial link anyway??? Answer: Higher rates affect credit.

Increasing rates should, by the law of demand, diminish the quantity of credit demanded. But as the NEDA chief warned, it could stall the economy.

Interestingly, this schism reveals that leaders of the BSP and NEDA have barely been sharing communications. Amazing.

Anyhow, this explanation by the former BSP head should bridge their "gap."

The rate hike, after all, was all about the Philippine peso.

PNA, May 19, 2023: Ensuring adequate interest rate differential between the Philippines and the US will help put market uncertainties at bay, Bangko Sentral ng Pilipinas (BSP) Governor Felipe Medalla said…“But what we’ll have to be very vigilant about is the extent to which a small differential between our policy rate and the Fed’s could cause significant weakening of the peso, which may actually become the new anchor of inflationary expectations,” he said. Thus, Medalla said that any developments overseas that will affect domestic rate of price increases and result to second round effects are factors that the BSP will definitely consider vis-a-vis its policy stance.

That's right. For the BSP, rate spreads matter.

Or, the narrowing gap between the BSP and FED policies could reduce the incentives of market participants and investors to hold the peso.

Figure 1

As a proxy, the yield spread between the 10-year US Treasury and BVAL Philippine counterpart narrowed to the lowest level since at least 2019.

And instead of lower rates in 2019-20, the present chapter of tightening differentials emerged on a backdrop of rising rates. (Figure 1, top and middle graphs) Do you now see why they panicked?

Yields of Philippine treasuries rose across the curve on the day the hike came into effect. With UST yield lower, this created the BSP's desired effect of widening the gap temporarily.

That said, should the peso weaken from it, this would further stoke inflation. (Figure 1, lower chart)

Worse, this could cause outflows (capital flight), reduce the economy's access to foreign currency loans, or raise the price of FX liquidity. That's the effective link between supply shocks and expectations.

Again, the attribution bias—it is the fault of the Fed!

Why use monetary policies when the Philippines supposedly has sufficient Gross International Reserves (GIR) to manage the FX market?

As previously discussed, our humble guess is that substantial portions of the GIR consist of "borrowed reserves."

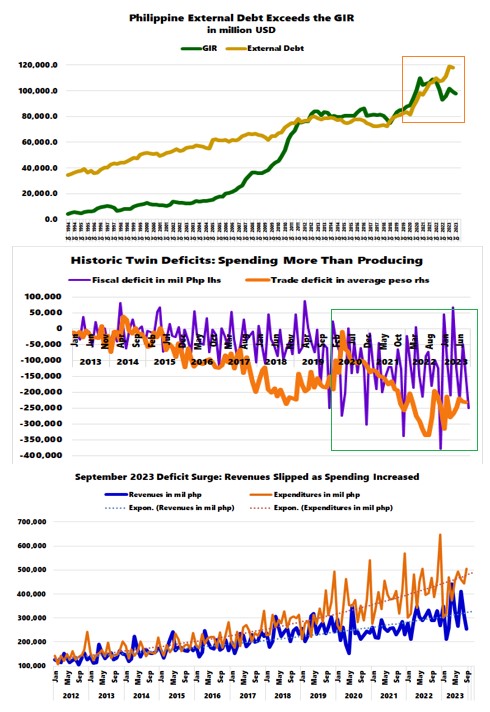

Figure 2

Not only that. However, because external debt has been rising faster than the GIR, in this case, the BSP can't afford a weaker peso. (Figure 2, topmost window)

The Php 57 level could be the Maginot line.

II. BSP’s Off-Cycle Hike: It’s Primarily Protecting Deficit Spending, 9-Month Deficit Neared the 2022 Levels

But there is more.

Why the surge in external borrowing?

In gist: The leaders of the Philippines believe in the Keynesian precept that one can borrow and spend their way to prosperity.

The twin (fiscal and trade) deficits, which have drifted close to their record levels, reveal that the Philippines (both public and private sectors) have been overspending. (Figure 2, middle graph)

With insufficient domestic organic FX revenues (exports, tourism, FDIs, etc.) and savings, it has to fill this void through external borrowing.

The more significant but implicit goal of defending the Philippine peso is to protect the deficit spending.

The public believes that the government’s emergency measures should become the norm, which validates Milton Friedman's axiom: "Nothing is so permanent as a temporary program."

Remember, authorities promised to do something to recover from the 2nd Quarter GDP bombshell.

GMANewsOnline, August 13: The Marcos administration’s chief economic manager, Finance Secretary Benjamin Diokno has expressed confidence that the government’s full-year economic growth target remains attainable despite the slowdown seen in the second quarter… To offset the underspending seen in the first half, Diokno said the government is preparing a spending catch up plan…“An aggressive catch-up plan for infrastructure projects (roads, bridges, airports, seaports, power, water, irrigation, telecommunications facilities, digitalization, school buildings, housing and others), quicker response by GOCCs, and strong and deliberate spending by resource-surplus local governments are essential parts of the solution to the relatively weak second quarter growth performance of the Philippine economy,” the Finance chief said. Similarly, National Economic and Development Authority (NEDA) Secretary Arsenio Balisacan said the government “will accelerate the execution of government programs and projects, including the delivery of public services, under the 2023 national budget.”

This fiscal stabilizer tool saw action in Q3.

GMANewsOnline, October 25:The Philippine government saw its fiscal balance yield a wider shortfall in September as state collections declined while expenditures expanded. Data released by the Bureau of the Treasury on Wednesday showed the national government’s budget deficit stood at P250.9 billion last month, higher by 39.6% from P179.8 billion in the same period in 2022. “The fiscal outturn for the period was underpinned by an 8.06% year-over-year acceleration in expenditures coupled with an 11.57% decrease in government receipts,” the Treasury said.

The fallout from the Q2 GDP eye-opener may have started to filter into revenues. In turn, public spending picked up tempo, resulting in the year's biggest monthly deficit last September. (Figure 2, lowest pane)

Figure 3

And because political spending (Php 3.82 trillion) exceeded collections (Php 2.84 trillion) in the nine months of 2023, the fiscal deficit swelled to Php 983 billion or just 2.8% away from 2022's Php 1.013 trillion—the second highest. (Figure 3, topmost and second to the highest charts)

Up by 9.5%, central government outlays represented the primary pillar of the 9-month spending activities. (Figure 3, second to the lowest graph)

Yet, the biggest growth emerged from Interest Payments, which rose by 15.04% and snared a 12% share of the total—the highest since 2009. (Figure 3, lowest diagram)

Higher rates have started to haunt the vogue obsession with political spending.

Rising interest payments and amortizations require automatic increases in allocations, which means public spending will go higher.

In 1H, Deficit-to-GDP remained at a lofty 4.8%. Unless the GDP picks up materially (ironically, driven by these expenditures), this ratio could expand. The increasing dependence on fiscal measures to boost the GDP translates to "fiscal dominance."

To emphasize: the pandemic response will serve as a blueprint for any economic slowdown or recession. The bailout culture or free lunch politics has become endemic.

Figure 4

In any case, as noted above, authorities have increasingly relied on FX borrowings to fill the public spending gap since 2021. (Figure 4, topmost chart)

And unsurprisingly, the USDPHP has risen along with nominal peso spending. And because the USDPHP signifies a symptom of domestic inflation, the CPI has risen along with it. (Figure 4, second to the highest and second to the lowest graphs)

And since the CPI is a primary driver of interest rates, rising rates reflect the crowding effect from public spending through inflation (spending more than producing). (Figure 4, lowest window)

III. The Inflationary Potentials from the Capping the USDPHP to Pave Way for Fiscal Dominance

And because of the crowding out, the economy will increasingly rely on fiscal dominance.

Figure 5

Declining Universal-commercial bank lending growth (as of August) has led to the devitalization of public revenue performance, which should lower the private sector's contribution to the GDP. (Figure 5, topmost chart)

In this case, funding the recharged deficit spending will likely require the BSP to jumpstart its monetization of public debt (QE). September's bounce manifests the decline in the BSP's liabilities to the central government (net claims on central government—NCoCG) rather than from QE. (Figure 5, middle window)

Banks will likely remain the chief providers of liquidity through its de facto monetization of public debt via NCoCG. (Figure 5, lowest graph)

For one thing, for the BSP, maintaining money supply growth has been its implicit principal goal: the BSP practices "Inflation Targeting" as the foundation of its monetary policies.

Figure 6

Nonetheless, compared to the US, which M2 has been contracting, it seems clear that this variance should pressure the peso. The Philippine money supply M3 growth momentum has been picking up (7.4% August). (Figure 6, top and middle windows)

As it is, M3 in peso has tracked the direction of public spending in peso, too. (Figure 6, lowest chart)

Figure 7

Aside from financing the twin deficits, the other crucial reason for the expansion in FX borrowings has been to increase the BSP's FX assets, which has served as a de facto US dollar standard anchor.

The BSP maintained a tight range (85-87%) for the share of FX assets for more than a decade. It served as the foundation for the domestic money supply operations. With the record injections in 2020, which boosted domestic securities at the expense of FX assets, this served as an Achilles Heel to the peso. (Figure 7, upper chart)

IV. Central Banks are "Dead Wrong:" The USD-Php Could Break the Php 57 level and Power a Rapid Advance

With this in mind, the BSP's emergency rate hike can be seen not only as a defense of the peso but to maintain the public boondoggles financed by FX borrowings.

However, given the structural weakness of the peso from the twin deficits and the FX vacuum in the BSP's balance sheets, this policy move will only have unintended consequences, which their quant models have not foreseen.

In politics, priorities are almost always channeled toward immediate concerns, disregarding their varying effects over time (time inconsistency).

And we agree with JP Morgan’s Jaime Dimon that central banks have been dead wrong.

CNBC, October 24: JPMorgan Chase CEO Jamie Dimon on Tuesday warned about the dangers of locking in an outlook about the economy, particularly considering the poor recent track record of central banks like the Federal Reserve…“I want to point out the central banks 18 months ago were 100% dead wrong,” he added. “I would be quite cautious about what might happen next year.” The comments reference back to the Fed outlook in early 2022 and for much of the previous year, when central bank officials insisted that the inflation surge would be “transitory.”

But to add, central banks have been "dead wrong" in inflating the global everything bubble via easy money (unprecedented QE and negative rates), which, more importantly, financed the welfare and the warfare state (resulting in the current wars). The global historic debt levels serve as a further testament to these unparalleled policy errors/experiments.

As such, in our humble opinion, staying long the USD Php would be a bet against developing uncertainties or insurance against boom-bust cycles and socio-economic turmoil. (not a recommendation)

A breakout of the USD Php from the Php 57 level would likely power it to test the latest all-time high of Php 59. (Figure 7, lower graph)

Besides, "a trend is your friend," as the aphorism goes, the USD PHP has been on an uptrend since the 1970s.

Yes, a bull market.