Inflation is a tax. Money for the government. A tax that people don’t see as a tax. That’s the best kind, for politicians—Lionel Shriver

With a 2nd Policy Rate Pause, a Victory Lap for the BSP? Philippine Treasury Markets and the PSEi 30 Slumps

After the second interest rate pause, the outgoing BSP Chief seemingly declared "triumph" over inflation. But Philippine financial markets expressed dissent.

I. The BSP’s Victory Lap over Inflation: "Ending Its Most Aggressive Tightening Cycle In Years"

Predicting that it contained inflation, the BSP's Monetary Board kept its policy unchanged for a second straight time.

GMA News, June 22: Following its policy meeting, BSP Governor Felipe Medalla said the Monetary Board kept the key rate for the overnight deposit facility at 5.75%, the overnight borrowing facility at 6.25%, and the overnight lending facility at 6.75%. This comes as the central bank now expects inflation to average 5.4% this year, slower than the 5.5% it projected during its meeting in May, citing the slower increases in prices of food and energy-related items in the past month.

Businessworld, June 23: PHILIPPINE CENTRAL BANK Governor Felipe M. Medalla said on Friday monetary policymakers had done enough to tame inflation, in his clearest signal yet that the Bangko Sentral ng Pilipinas (BSP) was ending its most aggressive tightening cycle in years. Mr. Medalla said the central bank’s future policy decisions will largely be driven by inflation data, which current forecasts show is on track to settle back within the bank’s 2%-4% target by the fourth quarter. (bold added)

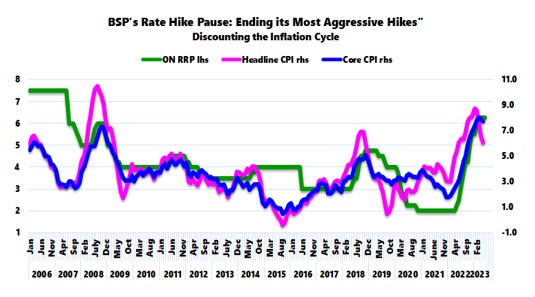

Figure 1

The establishment seems to have forgotten or discounted the "stickiness" of the Core CPI in its forecasts. Figure 1

Though the outgoing BSP chief seems confident to declare that they have surmounted the inflation dilemma, "ending its most aggressive tightening cycle in years," he contradicted this with a contingent, "largely be driven by inflation data."

Because data is history, and addressing inflation extrapolates to the future, such mismatch points to the risks of policy errors. In a word, BSP policies are reactionary.

Since the authorities denied from the get-go the emergence of the inflation crisis and blamed it instead on supply and private sector "hoarding," the BSP—in certainty—will be remiss in their prognosis of the inflation malady.

The fact that the BSP seems to deliberately ignore the imbalances forged from record liquidity injections, bank credit expansion, and BSP and bank-financed deficit spending translates to the concealment of the primary roots of inflation. This represents a policy of plausible deniability or "deny knowledge of or responsibility for actions committed by or on behalf of members of their organizational hierarchy."

For instance, as evidence, there is a tight correlation between the gyrations of the CPI and fiscal spending as well as the BSP’s net claims on the National Government (QE). (Figure 2)

Aside from these factors that help embellish the GDP, political authorities attain their objectives via increased taxes, expansive regulations, and mandates through a bigger government.

One can only maintain this privilege by whitewashing the role of the BSP and the Central Government as the source of inflation.

II. Response to the BSP’s "Rate Pause": Peso Rebounds Slightly, Treasury Yields Surge!

So did the markets agree with the BSP "pause?"

The most interesting is the response of the traders of the Treasury markets.

Figure 3

This week, BVAL rates rose, particularly in the belly—partly reversing the steep inversions—to flatten the curve. (Figure 3, upper chart)

Since June 9, the higher yield and the flattening dynamic have become more conspicuous. (Figure 3, lower chart)

If such a dynamic holds or even escalates, treasury traders could have started pricing in a comeback of inflation!

Yet, we see a close correlation between the flows and ebbs of the USD-Peso, CPI, and 10-bond yields. If so, a rebound in the USD-Php should not be a surprise. (Figure 4, upper graph)

Besides, authorities raised the issue of replacing Libor rates, which serve as a basis for the local Phiref.

Businessworld, June 22: In the Philippines, the LIBOR is still used for some fixed-income securities available in the market, as well as for interest rate and cross-currency swaps. The Philippine Interbank Reference Rate (PHIREF), which is used for interest rate swaps, cross-currency swaps and some peso corporate loans, is also computed using dollar LIBOR. (bold added)

Yet, rising Phiref or local interbank FX swap rates point to increasing USD liquidity strains in the banking system, therefore, a higher USD-Php. (Figure 4, lower chart)

It should also be noted that supply-side issues have also re-emerged.

The media reported the increasing rice prices and poor fish catch in May.

III. PSEi 30 Dismissed the Rate Pause; an Ominous Technical Chart; Record Systemic Leveraging

And it shouldn't be a surprise that with the re-escalation of rates, declining Philippine equities prices reinforced its bear market conditions.

The PSEi 30, down by 1.76% this week, closed at 6,393.55—a similar low it reached in March 2023 before the bounce.

Peso volume remains lackluster, while market breadth has been awful. While the principal equity barometer could bounce off to create an interim 'double bottom,' its long-term prospects seem portentous.

Figure 5

For chartists, haunting the PSEi 30 is a bleak 5-year head and shoulders pattern and a one-year rounding top, reinforcing this somber outlook.

Aside from cash and FX holdings becoming discernible competitors of bonds and equities, current conditions represent a headwind to the economy and the financial markets.

In closing, it is unclear if the BSP is aware of the impact of the unprecedented scale of financial leveraging in the face of the "most aggressive tightening cycle in years."

The sum of public debt and universal bank loans is at an All-Time High!

Higher rates extrapolate to higher borrowing, refinancing, and repayment costs. And it also translates to amplified liquidity requirements to keep this incredible scale of leverage afloat.

The Bulls will need Lady Luck on their side badly.