The semantic revolution which is one of the characteristic features of our day has obscured and confused this fact. The term inflation is used with a new connotation. What people today call inflation is not inflation, i.e., the increase in the quantity of money and money substitutes, but the general rise in commodity prices and wage rates which is the inevitable consequence of inflation. This semantic innovation is by no means harmless. Ludwig von Mises

In this issue

The Philippines May Core CPI Deviated from the Headline CPI, BSP’s RRR Cuts as First Sign of Credit Easing

I. "Imported" Disinflation?

II. Core CPI Deviates from the Headline CPI; Deflation in Transport CPI!

III. The Restructuring of Bank Lending (Towards Consumers); Economic Imbalances from the Credit Boom

IV. The Spike in Salary Loans Have Reversed, NPLs Surge!

V. Core CPI Fueled by Credit Card Boom, Induces a Drawdown in Savings

VI. Slowdown in Public Spending, Lower Headline CPI

VII. BSP’s RRR Cuts as First Sign of Credit Easing (Bank Rescue)

The Philippines May Core CPI Deviated from the Headline CPI, BSP’s RRR Cuts as First Sign of Credit Easing

The Philippine core CPI seems to have deviated from the slowdown in the headline CPI last May. Strong consumer credit growth fueled it. The BSP launched its first credit easing policy via RRR cuts.

Businessworld, June 7, 2023: PHILIPPINE inflation cooled for a fourth straight month in May to the lowest in a year as food and transport prices eased, the local statistics agency said on Tuesday, giving the central bank room to keep key rates steady. The consumer price index slowed to 6.1% from 6.6% in April, though it was faster than 5.4% a year earlier, matching the median estimate in a BusinessWorld poll last week. Still, it was the 14th straight month that inflation breached the central bank’s 2-4% goal…Inflation has averaged 7.5% this year, higher than the revised 5.5% forecast by the central bank. Core inflation, which excludes volatile food and fuel prices, slowed to 7.7% last month from 7.9% a month earlier. It has averaged 7.8% this year.

I. "Imported" Disinflation?

The Philippine CPI retreated to 6.1% in May, a level last reached in June 2022 or almost a year ago.

Then, the newly inducted President initially "disagreed" with the PSA statistics. Later, he attributed the mounting domestic inflation predicament as an "everywhere" phenomenon and thus was "imported."

With the CPI falling back to the same level a year ago, the President recently noted, "they were on the right track."

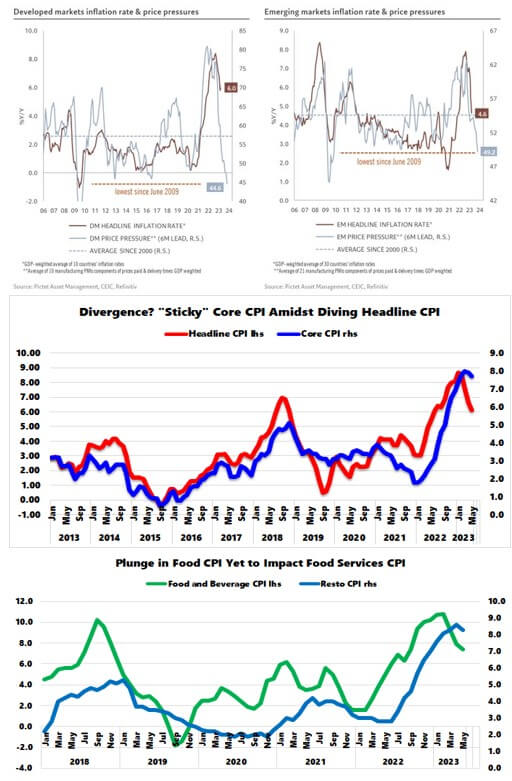

To borrow their reasoning, since inflation has been dropping almost "everywhere," could lower prices have also been "imported?" (Figure 1, topmost pane)

Or could this attribution bias (blaming others for failures, ascribing success to one's abilities) be about propping up popular approval?

II. Core CPI Deviates from the Headline CPI; Deflation in Transport CPI!

Yet, there seems to be a difference between now and the previous inflation episodes. While the headline CPI has nose-dived, the core CPI (ex-food and energy) has remained "sticky" or has diverged or lagged the headline.

The headline CPI sank by 260 basis points (bps) from the January 2023 zenith of 8.7%. On the other hand, the core CPI has only given up 30 bps from its March 2023 pinnacle of 8%.

In the past episodes, the core CPI either fell alongside or slipped ahead of the headline CPI. (Figure 1, middle window)

One possible explanation is implicit price controls via SRPs imposed by authorities on select basic commodities.

Of course, the inflation data doesn't capture the other methods by which commerce deals with inflation, such as the black market, "shrinkflation" or reduced quantity, value deflation or lower quality, and "sneakflation" or fees charged on ancillary items.

The other reason is that authorities took on focused or targeted measures. They allowed increased imports (more supply) of select commodities to lower prices.

A third explanation is the calculation of the CPI basket or its distribution of segments. In the non-food category, the restaurant and accommodation services carry the highest weight of 9.62%. In May, the sector's CPI had one of the hottest prints at 8.3%. (Figure 1, lowest chart)

The irony is diving food CPI (7.4% in May) has yet to affect the food services CPI. Another paradox is that food services CPI belongs to the non-food category!

And yet, even more ironies.

Figure 2

One of the most crucial factors for the fall in the headline CPI was the "deflation" in the Transport services CPI. Yes, believe it or not, it means prices actually dropped! Because of the 18.3% dive in the "Operation of Personal Transport Equipment," the sector posted a .5% decline in their May CPI. The 12.4% increase in "Passenger Transport Services" offset part of this deflation. (Figure 2, topmost chart)

Premised on many concocted assumptions, statistical models project a world beyond reality.

Here is the thing.

The mainstream fixates on the headline, specifically the food segment, even when it accounts for a minority share of the CPI. Food has a 39.91% share, plus fuel, which carries 6.74%, for a total share of 46.65%.

The core CPI, hence, signifies 53.35%, a majority, of consumer spending.

Why the focus on food? Because food prices affect a large section of the voting population. So in the realm of politics, authorities must be seen as addressing the concern of the masses.

III. The Restructuring of Bank Lending (Towards Consumers); Economic Imbalances from the Credit Boom

Aside from regulatory (price controls) and administrative (increase imports) measures, inflation's most important factor is its funding.

Sure, supply-side factors contribute to inflation. But price instability also reinforces supply dislocations. Sectors that benefit from liquidity injections and bank credit expansion not only come at the expense of the economy but induce resource misallocations, which lead to demand-supply imbalances.

We previously used listed food service chains as examples.

External factors, like fuel prices, while taking a substantial role in shaping the transport CPI, are secondary to the domestic forces. Again, as evidence, in 2020, the Transport CPI surged faster than the West Texas Intermediate (WTI) oil price. Further, WTI oil prices rolled over in May 2022, while the transport CPI crested two months later.

Why the disparity?

There are many forces. Here is one.

Pandemic policies and their aftermath—which reconfigured many sectors within the transport industry—induced shortages and disruptions. For example, the introduction of EDSA Carousel phased out former bus routes in EDSA, the Public Utility Vehicle Modernization Program replaced old jeepneys, the slow political response to the supply limits on Transport Network Vehicle Services (TNVS) and more.

In the face of the economic reopening, dislocations from these policies created bottlenecks. And this doesn't include the massive loss of capital from the economic shutdown. Moreover, during the pre-pandemic days, investors piled on the misallocations financed by a ballooning credit bubble. Inflation, economic paralysis, and credit bubbles not only combined to consume capital but also nurtured supply dislocations.

That aside, economic maladjustments were partly due to the restructuring of bank lending flows.

Little understood by the public is that banks have been shifting their lending thrust or direction towards consumers. (Figure 2, middle window)

That is to say, while consumers have more money to spend in the interim (because of bank loans), production has been insufficient to justify it. Or, "too much money chasing too few goods"—inflation!

Again, that consumers accounted for less than 10% of the overall bank loan portfolio may be true; in reality, credit penetration rates cover about half of adults (45% in 2021) mainly through informal means, according to the BSP's 2021 Financial Inclusion report.

As a side note, including real estate loans, consumers accounted for a record 20% of the Total Loan Portfolio (TLP) in Q1 2023.

Guess what are the primary sources for informal lending? And which dominates? Is it excess savings, remittance flows, or re-lending of clients from the formal sector (credit recycling)?

Nonetheless, let us examine the banking flows.

Consumer loans increased by Php 19.374 billion (MoM), the third highest after manufacturing Php 27.641 billion, and real estate Php 22.96 billion in April.

The Year-on-Year picture magnifies this gap.

Universal and Commercial consumer lending grew by Php 196.408 billion, which accounted for a 27% share of the net peso growth in April. In far second and third place were the electricity and trade sectors, with net increases of Php 131.98 billion and Php 116.9 billion.

While consumer lending, in pesos, was at an all-time high, its % share of total bank lending has been nearing its highest level since January 2020 at 10.1%

Is it then a surprise that the shift in bank loans favoring the consumers, which originated in 2015, has coincided with the uptrend in the CPI? (Figure 2, lowest diagram)

In the meantime, because of insufficient production, the economy relies on imports to fill that gap—resulting in higher trade deficits—which authorities have to counterbalance with external borrowing! External borrowing to offset the effects of domestic borrowing! Nice huh? [But this is a story for another day]

IV. The Spike in Salary Loans Have Reversed, NPLs Surge!

Figure 3

Bank consumer loans are not one-size-fits-all data, though.

In the present chapter, to confront the loss of purchasing power, people increased their use of credit or leverage.

That said, while the middle and higher-income groups tapped credit cards, the lower-income segment has used salary loans.

It doesn't surprise us that April's pullback in salary loans has also been congruent with the dive in the CPI. Or, the austerity embraced by the low-income group translated to reduced food purchases/consumption. (Figure 3 topmost window)

Importantly, have the lower-level groups exhausted their personal balance sheet space?

Signs are they have. Despite the relief measures, non-performing salary loans in the banking system have surged relative to the Total Loan Portfolio (TLP) and the share of Total NPL.

It would seem that salary loans are the bank's weakest consumer link. (Figure 3, middle chart)

And as the economy slows and job losses increase, so should NPLs.

V. Core CPI Fueled by Credit Card Boom, Induces a Drawdown in Savings

Again, it is no surprise that the ascent of bank credit card loans has jibed with the headline and core CPI too. (Figure 3, lowest chart)

Figure 4

And some segments of the core CPI, such as personal care & miscellaneous goods and household furnishing, have also dovetailed with the growth rate of credit cards. (Figure 4, topmost chart)

Again, thanks to the subsidies (interest rate cap), it has been a downtrend for credit card NPLs. (Figure 4, middle window)

But once liquidity tightens, we can expect a sharp reversal—slower lending and higher NPLs.

Interestingly, the raging inflation has created a shift in savings. Despite the bank credit expansion, savings have barely improved.

The YoY change in M2 savings deposits continues to fall (-.6%) in April, the fourth month of deflation. This drawdown exhibits the use of savings to augment the loss of purchasing power by the public. But part of these has shifted to time deposits to lock into higher rates. (Figure 4, lowest chart)

Disruptions from monetary interventions diffuse to cover almost all aspects of the economy with a time lag.

VI. Slowdown in Public Spending, Lower Headline CPI

Figure 5

Finally, public spending represents another major demand factor in inflation.

The recent slowdown in public spending, which has partly served as a roadblock to the bank credit expansion, has also corresponded with the lower CPI. (Figure 5, topmost window)

Because deficits have narrowed, the BSP has reduced its QE via net claims on the central government (NCoCG). (Figure 5, middle pane)

Nevertheless, banks continue to infuse liquidity to the government through NCoCG, which has, at its expense, shown liquidity strains. (Figure 5, lowest chart)

Figure 6

And these have been vented via the CPI and the (weaker) USD-Php. (Figure 6, topmost chart)

VII. BSP’s RRR Cuts as First Sign of Credit Easing (Bank Rescue)

Nonetheless, excess liquidity has still been circulating in the system, as signified by the inflation rate below the GDP.

But it is being gradually siphoned off by the government.

That said, it should not surprise us that to mitigate the worsening liquidity strains, the BSP declared a substantial cut on the (Reserve Requirement Ratio) RRR of banks this week.

Let us not forget that debt has been the foundation of the GDP. Debt finances demand, as shown above. And debt also funds supply (the race to build supply).

But financing costs should continue to rise, not just thru elevated rates but because of its higher stock level.

Though denying rate cuts amidst a falling CPI, history and path-dependent policies tell us that more BSP easing should be around the corner. (Figure 6, middle chart)

The historic RRR cuts—to the lowest level—represent the shot across the bow on tight money. (Figure 6, lowest chart) But the BSP denies it. (We shall deal with this in another post)

In any event, the mainstream has been addicted to free lunches from the BSP's liquidity treat.

So, because it's hard to wean from such dependence, especially the public spending teat, they'd "reflate" sooner than later. And this would fire up the third wave of inflation.

It is happening.

No comments:

Post a Comment