Perhaps more than anything else, failure to recognize the precariousness and fickleness of confidence—especially in cases in which large short-term debts need to be rolled over continuously—is the key factor that gives rise to the this-time-is-different syndrome. Highly indebted governments, banks, or corporations can seem to be merrily rolling along for an extended period, when bang!, confidence collapses, lenders disappear, and a crisis hits—Carmen Reinhart and Kenneth Rogoff

In this Issue

Goldilocks Meets the Three

Bad Bears: BSP’s Sixth Rate Cut and the Late-Cycle Reckoning

I. The BSP’s Sixth Cut and

the Goldilocks-Sweet Spot Illusion

II. Data-Driven or

Dogma-Driven? The Myth of Low-Rate Growth

III. The Pandemic Rescue

Template Returns, The MSME Credit Gap

IV. Fintech’s Limits, Financial

Concentration: Banking Cartel by Design

V. Treasury Market

Plumbing: Who Really Benefits?

VI. Crowding Out: Corporate

Issuers in Retreat

VII. The Free Lunch

Illusion: Debt and Servicing Costs

VIII. Banks as the Heart

of the Economy: Palpitations in the Plumbing

IX. Q2 2025 Bank Profit

Plummets on Credit Loss Provisions

X. Conclusion: Goldilocks Faces the Three Bad Bears

Goldilocks Meets the Three Bad Bears: BSP’s Sixth Rate Cut and the Late-Cycle Reckoning

The Bangko Sentral ng Pilipinas’ latest rate cut is a "Goldilocks" illusion masking a late-cycle reckoning driven by crowding out, surging leverage, and mounting stress in the financial system

I. The BSP’s Sixth Cut and the Goldilocks-Sweet Spot Illusion

Reinforcing its "easing cycle," the Bangko Sentral ng Pilipinas (BSP) cut policy rates last week—the sixth reduction since August 2024. Officials claimed they had reached a “sweet spot” or “Goldilocks level”—a rate neither inflationary nor restrictive to growth, as the Inquirer reported.

We’ve used “sweet spot” before, but not as a compliment. In our framing, it signals ultra-loose monetary policy—part of a broader “Marcos-nomics stimulus” package that fuses fiscal, monetary, and FX regimes into a GDP-boosting mirage. A rescue narrative sold as reform.

II. Data-Driven or Dogma-Driven? The Myth of Low-Rate Growth

The idea that “low rates equal growth” has calcified into public gospel.

But if that logic holds, why stop at 5%? Why not abolish interest rates altogether—and for good measure, tax 100% of interest income? By that theory, we’d borrow and spend our way to economic utopia. In short: Such (reductio ad absurdum) logic reduces policy to absurdity: prohibit savings, unleash debt, and expect utopia.

Figure 1

The BSP insists its decisions are data-driven. But have they been? Since the 1998 Asian Crisis, rate cuts have been the default posture.

And since the 2007–2009 Global Financial Crisis, each successive cut has coincided with slowing headline GDP—through the pandemic recession and beyond. The decline was marginal at first, barely noticed. But post-pandemic, the illusion cracked. (Figure 1 upper pane)

A historic rescue package—Php2.3 trillion in injections, rate cuts, RRR reductions, a USD-PHP soft peg, and sweeping relief measures—combined with unprecedented deficit spending, triggered a temporary growth spike. This extraordinary intervention, combined with global reopening, briefly masked structural weaknesses.

But since 2021, GDP has resumed its downward drift, with the deceleration becoming conspicuous through Q2 2025. Inflation forced the BSP to hike rates, only to restart its easing cycle in 2024.

So where is the evidence that low rates boost the economy?

III. The Pandemic Rescue Template Returns, The MSME Credit Gap

Today’s “sweet spot” eerily mirrors the pandemic-era rescue template—minus the direct injections and relief measures. For now.

Meanwhile, over half the population still self-identifies as borderline or poor (self-rated poverty surveys—SWS and OCTA).

GDP, as a measure, fails to capture this disconnect—possibly built on flawed inputs, questionable categorization and assumptions, as well as politically convenient calculations.

Meanwhile, the BSP’s easy money regime and regulatory bias have allowed banks to monopolize the financial system, now accounting for 83% of total financial assets as of Q2 2025. (Figure 1, lower graph)

Yet MSMEs—the backbone of employment at 67% (as of 2023, DTI)—remain sidelined.

Ironically, Republic Act No. 9501 mandates banks to lend 10% of their portfolio to MSMEs (8% to micro and small, 2% to medium enterprises).

Figure 2

But compliance has collapsed—from 8.5% in 2010 to just 4.63% in Q1 2025. (Figure 2, topmost image)

Banks, unable to price risk appropriately, prefer paying penalties over lending to the sector. The result: the credit boom inflating GDP primarily benefits 0.37% of firms—the large enterprises that employ only a third of workers.

While RA 9501 mandates banks to allocate 10% of their loan portfolio to MSMEs, BSP regulations restrict risk-based pricing—directly through caps on consumer and financing loans (BSP Circular 1133) and indirectly in MSME lending through microfinance rules (Circulars 272, 364, 409, and related issuances).

Again, unable to fully price in higher default risks, banks often find it cheaper to pay penalties than to comply.

IV. Fintech’s Limits, Financial Concentration: Banking Cartel by Design

At the same time, banks are aggressively expanding into consumer credit, while the unbanked majority continues to rely on the informal sector at usurious or punitive rates.

Fintech e-wallets have gained traction, but they remain mostly transactional platforms. Banks, by contrast, are custodial institutions. Even if convergence is inevitable, bridging the informal credit gap will remain elusive unless rates reflect real distribution and collection risks.

This convergence may democratize leverage—but banks still dominate credit usage, reinforcing a top-heavy system.

Deepening concentration, paired with price restrictions, resembles a cartel. A BSP-led cartel.

And the first beneficiaries of this low-rate regime? Large enterprises and monied consumers.

V. Treasury Market Plumbing: Who Really Benefits?

And like any cartel, it relies not only on market power but also on control of the pipes—the very plumbing of the financial system, now evident in the Treasury market

The Bangko Sentral ng Pilipinas has dressed up its latest rate cut as part of a “Goldilocks easing cycle,” but the bond market tells a different story.

Even before the policy shift, the Philippine BVAL Treasury yield curve had been flattening month after month, with long rates falling faster than the front end. (Figure 2, middle and lower charts)

That is not a picture of renewed growth but of markets bracing for a slowdown and disinflation.

The rate cut simply ratified what the curve had

preemptively declared: that the economy was softening, and liquidity needed to

be recalibrated.

Figure 3

From the Treasury market’s perspective, the real beneficiaries weren’t households or corporates—they were institutional actors navigating a crowded, distorted market.

Trading volumes at the Philippine Treasury market raced to all-time highs in August, just before and during the cut! (Figure 3, topmost diagram)

This wasn’t retail exuberance—it was plumbing.

BSP’s direct and indirect liquidity injections, coupled with foreign inflows chasing carry (data from ADB Online) amid global easing and macro hedges created a bid-heavy environment. The rate cut amplified this dynamic, lubricating government borrowing while sidelining private credit. (Figure 3, middle visual)

VI. Crowding Out: Corporate Issuers in Retreat

Meanwhile, the collateral damage is clear: corporate bond issuance has been trending downward, regardless of interest rate levels—both in nominal terms and as a share of local currency debt. (Figure 3, lowest window)

This is evidence of the crowding-out syndrome, which suggests that BSP easing isn’t reviving private investment—it’s merely accommodating fiscal expansion.

In the cui bono calculus, the winners of rate cuts are clear: the state, the banks, and foreign macro hedgers.

The losers? Domestic firms, left behind in a market—where easing no longer means access.

VII. The Free Lunch

Illusion: Debt and Servicing Costs

Figure 4

The deeper reason behind the BSP’s ongoing financial plumbing lies in social democracy’s favorite illusion: the free lunch politics.

Pandemic-era deficit spending has pushed public debt to historic highs (Php 17.27 trillion in June), and with it, the burden of debt servicing. (Figure 4, topmost chart)

July’s figures—due next week—may breach Php 17.4 trillion.

Even with slower amortizations temporarily easing the burden in 2025, interest payments for the first seven months have already set a record.

Crowding out isn’t just theoretical.

It’s visible in the real economy—where MSMEs and half the population (per self-poverty surveys) are squeezed—and in the capital markets, where even the largest firms are feeling the pinch.

The entropy in financial performance among PSE-listed firms, especially the PSEi 30, underscores that the spillover has reached even the politically privileged class. (see previous discussion—references)

Monthly returns of the PSEi 30 similarly reflect the waning impact of the BSP’s cumulative easing measures since 2009. (Figure 4, middle image)

In a world of scarcity, there is no such thing as a permanent free lunch.

VIII. Banks as the Heart of the Economy: Palpitations in the Plumbing

If the government is the brain of the political economy, banks are its heart. And the pulse is showing increasing signs of palpitations.

Bank NCoCG surged 7.5% YoY to an all-time high Php 5.591

trillion in Q2 2025, pushing Held-to-Maturity (HTM) assets up 1.8% YoY to a milestone

Php 4.075 trillion. (Figure 4, lowest graph)

Figure 5

OFCs saw an even sharper jump—14.7% in Q1 to a record Php 2.7 trillion! (Figure 5, topmost diagram)

According to the BSP, OFCs are composed of non-money market investment funds, other financial intermediaries (excluding insurance corporations and pension funds), financial auxiliaries, captive financial institutions and money lenders, insurance corporations, and pension funds.

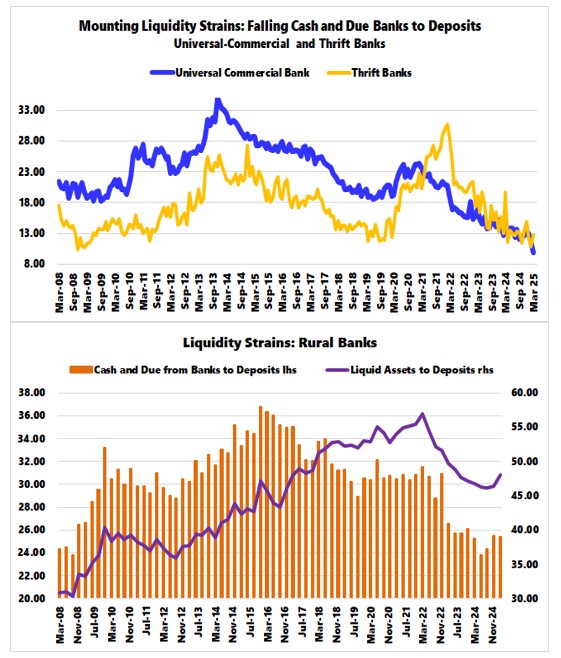

Yet despite these massive reallocations—and even with banks drawing a staggering Php 189 billion from their freed-up reserves (Claims on Other Depository Corporations) after March’s RRR cut—liquidity remains tight. (Also discussed last August, see references) (Figure 5, middle chart)

Cash reserves continue to decline. Though cash-to-deposit ratios bounced in June from May’s all-time low, the trend remains downward—accelerating even as RRR rates fall to 5%. (Figure 5, lowest image)

Liquid assets-to-deposit ratios have slumped to levels last seen in May 2020, effectively nullifying the supposed benefits of the BSP’s Php 2.3 trillion pandemic-era injections.

This strain is now reflected in bank stocks and the financial index—dragging down the PSE and the PSEi 30.

Goldilocks, eh?

After the rate cut, the BSP immediately floated the possibility of a third RRR reduction—“probably not that soon.” Highly doubtful. Odds are it lands in Q4 2025 or Q1 2026.

But even if the BSP dismantles the Reserve Requirement entirely, unless it confronts the root cause—the Keynesian dogma that credit-financed spending is a growth elixir—the downtrend will persist.

At zero RRR, the central bank will run out of excuses. And the risk of bank runs will amplify.

IX. Q2 2025 Bank Profit Plummets on Credit Loss Provisions

Figure 6

The toll on banks is already visible—profits are unraveling. From +10.96% in Q1 to -1.96% in Q2. (Figure 6, upper visual)

The culprit?

Losses on financial assets—driven by surging provisions for credit losses, which ballooned 89.7% to Php 43.78 billion in Q2. That’s pandemic-recession territory—December 2020. (Figure 6, lower graph)

X. Conclusion: Goldilocks Faces the Three Bad Bears

The cat is out of the bag.

The “stimulative effect” is a political smokescreen—designed to rescue banks and the elite network tethered to them. It’s also a justification for continued deficit spending and the rising debt service that comes with it.

But “sweet spots” don’t last. They decay—subject to the law of diminishing returns.

Paradoxically, under the Goldilocks fairy tale, there were three bears. In our case: three ‘bad’ bears:

- Crowding out and malinvestments

- Surging systemic leverage

- Benchmark-ism to sanitize worsening fundamentals

Even the Bank for International Settlements has quietly replaced Philippine real estate pricing bellwethers with BSP’s version—one that paints booming prices over record vacancies.

Nonetheless, the bears are already in the house. The porridge is cold. And the bedtime story is over. What remains is the reckoning—and the question of who’s prepared to face it without the comfort of fairy tales

All signs point to a late-stage business cycle in motion.

___

references

Prudent Investor Newsletters, Q2–1H Debt-Fueled PSEi 30 Performance Disconnects from GDP—What Could Go Wrong, August 24, 2025 Substack

Prudent Investor Newsletters, Philippine

Banks: June’s Financial Losses and Liquidity Strains Expose Late-Cycle

Fragility, August 17, 2025 Substack