(edited from Newsletter edition)

``The real difference is that China’s communist government has succeeded in globalising a much larger share of its population than India’s democratic government has managed to do.” Kenneth Rogoff, Harvard economist

During the past week, a headline article in a business broadsheet appeared where various domestic economic experts broached deep concern over the sharp appreciation of the Peso with some of them suggesting that our government keep the local currency at certain levels. In other words, some of our experts are advocating compelling the government to intervene and manipulate the local currency for what I believe as “perceived short term” benefits.

The kernel of our argument in my January 2 to 6th edition, (see Fear Not the Rising Peso) was based on the prospects of diminishing export competitiveness which we aptly debunked. A second issue was likewise raised by the article concerning the domestic economy’s dependence on remittances wherein a weaker dollar allegedly translates to weaker consumer spending by the beneficiaries of the foreign exchange brought into the country by our overseas workers.

Let me reiterate the fundamental premise of my contention, relative to export competitiveness, currencies as expressed by its price value or exchange rates have not been the sole and most important determinant of export competitiveness especially in a world where demand, supply and finances have gradually been integrating.

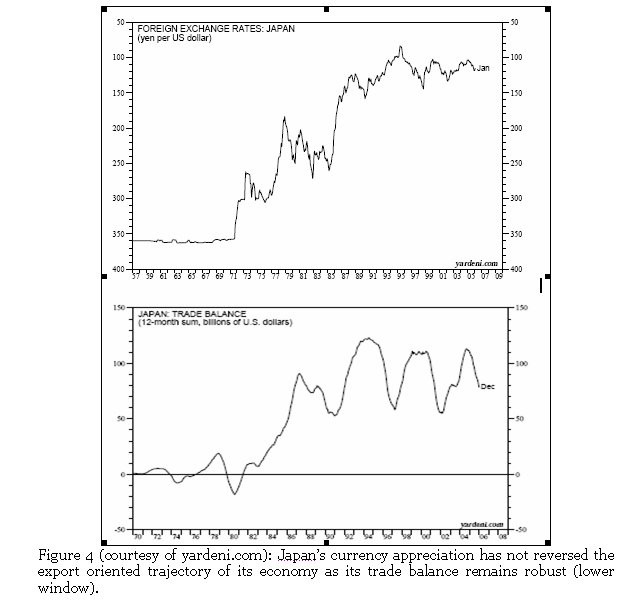

To wit, Japan’s currency have jumped over a period of time from 370 yen in 1970 to about 118 yen today, yet its trade balance have reached are treading near or at record highs as shown below.

On the same plane, we see a sharp reversal of Brazil’s currency, the real, since 2002, yet the currency’s strengthening has produced, instead of attenuating exports, surging trade surplus brought about by record exports even as the commodity based economy tries to climb up the value chain by adopting “internal reform measures”!

An opposite viewpoint could be seen with the US dollar index. As measured by its trade weighted share relative to its corresponding major trading partners, as seen in the above chart, the US dollar benchmark index has fallen from 2002 to 2004 nonetheless has failed to curb its record setting trade deficits and in fact continues to fall into the abyss, see figure 6!

In other words, while adjustments in currencies through fiat policies appears to be an easy way out to remedy trade imbalances, they have unintended consequences that may prove more detrimental or fatal than what is aimed to be rectified for political convenience.

To quote leading Austrian economist and free market advocate (emphasis mine) Ludwig von Mises, ``If one looks at devaluation not with the eyes of an apologist of government and union policies, but with the eyes of an economist, one must first of all stress the point that all its alleged blessings are temporary only. Moreover, they depend on the condition that only one country devalues while the other countries abstain from devaluing their own currencies. If the other countries devalue in the same proportion, no changes in foreign trade appear. If they devalue to a greater extent, all these transitory blessings, whatever they may be, favor them exclusively. A general acceptance of the principles of the flexible standard must therefore result in a race between the nations to outbid one another. At the end of this competition is the complete destruction of all nations' monetary systems.”

It seems that our experts have forgotten that the gist of today’s issues have been strongly interrelated with the Brobdignagian deficits in the

Second is the question of the valuation metrics. Despite the Peso’s fall from Php 26 to Php 56 to a US dollar from 1992 to 2005, the rate of change as measured in the Philippine export growth has even slumped (see January 2 to 6th edition, see Fear Not the Rising Peso)! We can draw up economic models for all to see yet question is will it work? But who would pay for a misdiagnosis effected by misdirected government policies? Why not let the market set its own valuation metrics?

Third, getting our products to the global economy by building the required infrastructure. To quote Harvard economist Kenneth Rogroff, ``Over the past five years,

Fourth, with the evolution of the trade dynamics borne out of technological changes, the trend of outsourcing has been inclined towards accessibility to a supply of highly qualified labor pool with an environment conducive to productive collaboration between corporations and universities. Let me quote the New York Times report of Steve Lohr (emphasis mine), ``The study contended that lower labor costs in emerging markets are not the major reason for hiring researchers overseas, though they are a consideration. Tax incentives do not matter much, it said. Instead, the report found that multinational corporations were global shoppers for talent. The companies want to nurture close links with leading universities in emerging markets to work with professors and to hire promising graduates.”

Fifth, if the aim is to get a big portion of our economy to be “globalized” then the country has to set conditions conducive to capital and investment flows. It has to give weight towards lowering the cost of doing business, increase labor productivity, adopt and maintain regulations, economic and monetary policies favorable to capital flows and market access, improve accessibility to the capital markets and reduce state intervention to economic affairs. Why then concentrate on the price factors instead of real concrete changes or reforms?

Sixth, is the risk of incurring foreign exchange losses; considering the financial difficulties of the present government, could we allow our public institutions to absorb more losses or incur further financial strains for gains that are likely to be ambiguous? How about the risk of diffusing inflation into the economic system? Have devaluations not been the cause of reduced savings to the people and reduced standards of living transmitted via price inflation?

Throughout the entire 2003 to the First quarter of 2004,

Finally, is the issue of consumer spending; while the negative side of our labor exports have been highlighted by the media to even demean the industry by labeling them as “maid exports”, why is it that our experts seem to mollycoddle on the “rhetorical” preservation of a fragile consumption-led remittance based growth model rather than advocate on an investment fueled one which could be induced by a rising currency?

To a reprise a quote from Dr Marc Faber (emphasis mine), ``a strong currency has never been a problem in the long run. It forces corporations to become extremely efficient, to innovate and to invent new methods of production. Weak currencies on the other hand are an incentive to compete based on short term favourable exchange rate movements – in nature very much alike protectionist economic policies.”

Resistance to change would be a natural reaction that could be expected from the man on the streets....but normally, not from our experts.

No comments:

Post a Comment