``Successful investing doesn't require above-average intelligence because it is not an intellectual challenge; it is an emotional one and, I believe, it is a challenge most of you are capable of meeting head on and winning. If there's anything 'clever' about what I do, it is recognizing what works and ignoring what doesn't.”-Mark Shipman: The Next Big Investment Boom

Figure 4: US Dollar Index Loss; Phisix Gains

As explained last week, the falling US dollar trade weighted index has had a “stimulative” aftereffect to emerging market assets. As such we have been seeing an accelerated increase in the prices values of world equity indices, as well as in commodities to emerging market equities.

In particular, I have noted that the Phisix experienced its cyclical reversal when the US Dollar index peaked in 2003 backed by the Fed’s flooding of the global marketplace with superfluous liquidity to arrest any prospects of deflation. The Phisix climbed at the back of intense foreign buying then until early 2005 as foreign money played the US dollar diversification theme.

For most of 2005, as the US dollar recovered on the premise of interest rate/yield differentials while the Philippine market practically stood still or traded rangebound. As shown in Figure 4, the mid April collapse of the US dollar index has been inversely associated with a positive reaction from the Phisix once again bolstered by foreign portfolio flows.

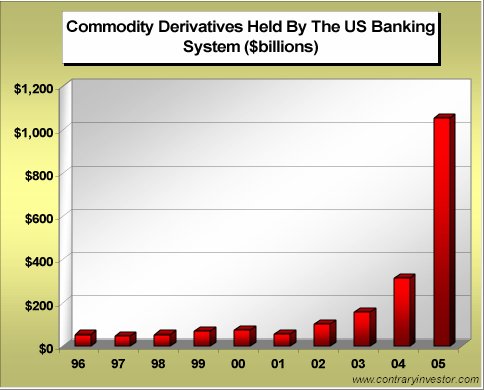

Figure 5: Phenomenal Growth of Commodity derivatives

As a measure to the exponential growth of world surplus liquidity contraryinvestor.com shows us of the bulging commodities trade underpinned by exploding derivatives held by US banks!

While global monetary authorities have the power to control the liquidity valves, as to where it flows is practically beyond their reach. Here the authors of contraryinvestors.com suggest that to profit from present liquidity flows simply means to “follow the money” (emphasis mine),

``...whether the Fed is willing to admit this or not, it has become the servant to the hedge fund managers, the prop desk traders, the structured finance masters of the universe, etc. Under this set of circumstances, our best near term investment returns lie where these aforementioned allocators choose to position the Fed liquidity largesse at any point in time. And that's currently in the hard asset complex. Simple enough? Until these forces or dynamics change, we need to stay long energy, long equities benefiting from higher commodity prices, in short duration fixed income if at all, as well as long precious metals.

Nonetheless, the world financial markets appears to be too complacent, wearing rose colored glasses...and a word of caution from Dr. Marc Faber...``Right now, risk appetite is at an extreme and everybody is bullish about something. Investors are also extremely optimistic about the global economy. Hence the significant rise in commodity prices. However, given tighter international liquidity and weakness in U.S. housing, and the potential for equity markets to undergo a nasty correction in the next three to six months, the global economy could — for a change, after having surprised on the upside for the last three years — disappoint. If such a scenario were to play out,

In short, be wary of a short term jolt. Keep your mental stops on.

No comments:

Post a Comment