``No government wants a hard currency which preserves purchasing power. They want a deceptively soft currency which inflates away debt and secures a competitive advantage for exports.”-David Fuller, Fullermoney.com

Leveraged positions entrenched in the global financial markets present themselves as heightened volatility risks considering the argument to resolve current imbalances. However, we should not forget that it is from taking on more risks where above average returns can be generated.

Question is, considering the current risk environment, to what investment theme/s should one consider as to generate positive returns relative to the risks?

Figure 3: Stockcharts...Breakouts the US Dollar Index (black line) and US 10 Year Yields (candlestick)

I noted that the US dollar have so far benefited from the increased volatility seen in the global markets. Some have taken this in the context of rushing into the proverbial “safehaven” following the recent market rout. However, the global market signals a different tune. While US equities appear to be holding, the bond markets have been steadily weakening, hardly a manifestation of an onrush to dollar based assets (see figure 3).

Instead, in my view, these could be more of a short covering undertaken by the heavily levered bearish US dollar camp prior to the spike in volatility.

As a matter of leverage, those who massively shorted the US dollar were similarly intensively long gold, commodities and emerging market assets, as well as junk bonds. When the liquidity squeeze came about, every of these assets got hit.

Question is, has this been the end of the run for these markets?

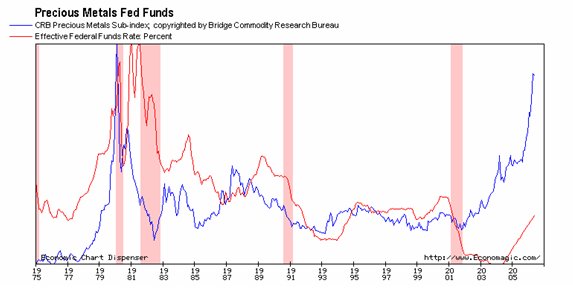

In the past, rising interest rates have not hampered the rise in gold prices as shown in Figure 4, when REAL interest rates remained negative.

Figure 4 Rising Metal Prices (blue line) and FED Fund Rate (red line)

The US economy is said to be behind the curve, meaning that despite the series of increases in interest rates, Fed data does not represent real or actual inflation. With present interest rates still hovering at negative or that unofficial inflation rates are still higher than nominal interest rates, such conditions are still said to be accommodative. According to Adam Hamilton of ZealLLc.com, ``When real rates of return fall to near zero or below, capital flees credit instruments that begin to actually destroy real wealth and some seeks refuge in the ultimate safe asset, gold.”

In the 70’s despite rising interest rates gold leapt from $35 to over $850 at the time interest rates had been accelerating due to high inflation, aggravated by closed economies, wage spiral and highly protected and regulated markets. US treasury yields then galloped to over 15%! Until real interest rates became starkly positive “approaching 8%” according to Mr. Hamilton, before gold stumbled to its decade long bear market.

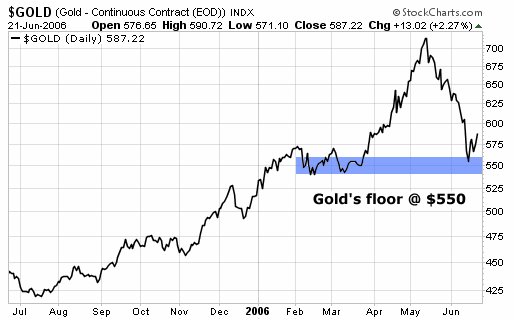

Figure 5 Daily Wealth: Gold’s floor?

Recently gold like all other assets which climbed on speculative leverage fell like a stone on the recent markdown brought about by the liquidity squeeze or increased risk aversion. As shown in Figure 5, the psychological threshold for gold appears to be at the $550 level. Today, gold appears to be staging a rally from its recent lows.

What makes me bullish about gold is first, from a net long position it appears that the shorts have taken over (if there is any leverage today it is the shorts-making a short squeeze very likely).

Second, technically gold has been quite oversold bouncing off from $550. This means that the psychological threshold which served as a base prior to its take off remains a significant and strong support level (until of course broken). This also suggests that gold then is coming off from a low (if such base holds).

Third, the uptrend despite the recent correction has been unviolated. Fourth, given the currency markets long wait before delivering the verdict for the US dollar to a breakout, in my view, such reluctance suggests that the US dollar is less likely the safehaven sought in the present volatility.

US dollar bears point to US imbalances as possible catalysts for a selloff, while US dollar bulls allude to a potential political, financial and economic crisis in China for its strength (rush to safehaven). My view is that when paper money whose strength derives from faith comes into question, the likelihood is a shift to hard assets, which makes gold a likely candidate.

Those who argue that gold’s fate has been tied inversely to the US dollar seems to forget that last year or in 2005 despite the strength of the US dollar, as measured by the trade weighted index, was up 12.86%, while gold soared even by more 17.92%! A correlation is a correlation until it isn’t. Yet none of the world’s greatest investment guru’s I know predicted on such possible correlation to thrive, as gold was predominantly viewed as the nemesis to the US dollar (wrong- to fiat currencies in general). Last week, both the US dollar index (+.81%) and gold (+1.08%) rose in tandem. When it comes to fear and lingering uncertainty, both gold, considering the thin market, and US dollar may rise!

Fifth, no I won’t be arguing about central banks shifting to gold which is rather speculative, in fact I prefer gold into private hands. If gold does rally as I expect it to, then the likelihood that we could see a rally in emerging market stocks, barring any unforeseen shocks...despite possible weakness in the US stocks. The incipient divergence may start to unfold.

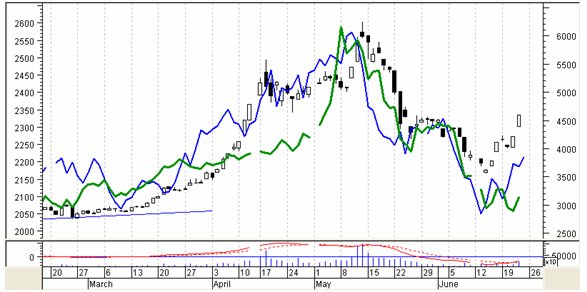

Figure 6: Stockcharts: rallying Gold (candle) MS Emerging Free Markets (line)

Figure 6 shows the tight correlation between emerging markets performance as signified by the Morgan Stanley Emerging Free Index and gold, (which could likewise translate into a rally in the Phisix!). I know, I know....data have shown of net outflows during the past weeks....but could a rallying gold inspire a reversal to inflows anew?

I have talked about the potentials of the local mining index at great length ad nauseam. Despite the recent selling pressure over the broadmarket as manifested in the Phisix, the mining index have mimicked the price movement of gold lagged by only TWO days.

Figure 7: Phil Mining Index (candle) Phisix (green) and CBOE GOX (Blue)

Since my metastock chart has no gold chart for us to be able to overlap, I have in place taken the CBOE “GOX” Gold Mining (blue line) index of the US as representative. As you can see in Figure 7, the Philippine Mining index alongside the GOX has surreptitiously scaled higher in spite of the recent selling pressures in the Phisix.

If the correlation between gold and emerging markets will continue to hold true, then I am to project that the Phisix to progress alongside its peers despite being the traditional laggard.

Some are asking as to what extent of their portfolio should they allocate for their mining plays. It actually depends on your risk appetite. In my case, considering the massive growth potentials of the industry relative to total market cap or to GNP, I give them a majority.

No comments:

Post a Comment