``The ladder of success is best climbed by stepping on the rungs of opportunity."- Ayn Rand

If there is any one factor that holds sway to the global financial markets of late, it is the speculations about the US Fed’s next moves. Last week, as Chairman Bernanke appeared on the US Congress for his Monetary Policy report, and the equity markets suddenly exploded to the upside on the view that Bernanke hinted for a pause. Global equity markets followed suit, US and global bonds rallied while the US dollar declined.

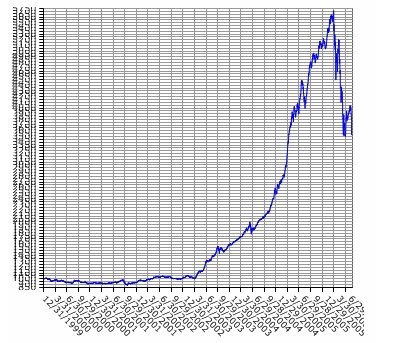

Figure 2 stockchart.com: Phisix (candlestick) and S & P 500 (line)

As shown in Figure 2, over the past three months, or since May, the Philippine Composite Index has largely shadowed the movements of the S & P 500 index of the US. Unlike my original expectations that the Phisix, which had previously ran the same course with that of Gold, would ply the same route or pattern, it now appears that investors have pinned the activities of the domestic market in line with the outlook in the US, which in my view, is not entirely promising.

The US Federal Reserve raised its overnight interbank lending rates for the 17th time last June to normalize its money policies, load up on its monetary ammo against possible emergence of deflation, defend the US dollar (my view) and moderate the growth clip of its economy. Since the global financial system has been addicted to profuse liquidity injections which led to inflationary pressures worldwide, the prospects of a pause signifies of its continuity, hence the resonant jubilation at first instance.

Yet, the paradox here is that it comes in the face of an economic downturn, which makes the initial euphoria in the US markets unwarranted. Analyst Paul van Eeden warned (emphasis mine), ``On Wednesday the stock market in the US rallied because Ben Bernanke indicated that he might not push for higher interest rates. Two weeks ago the market rallied because of weak retail sales numbers. This market is dangerous: investors are desperately searching for good news.

``When weak retail sales figures and the Fed Chairman's comments that he sees the economy slowing are interpreted as good news for stocks, then you know it is time to get out of the market.”

As you know, I have been in the camp of those who think that the US Fed would embark on a gamut of rates cuts once signs of a downturn snowball. I mentioned that political expediency (election season, pressures from the public), inveterate fear of deflation, aside from ideological leanings by the Fed Chief, past actions undertaken by the Fed (see Figure 3) and the huge leverage in its system which translates to more money “created out of thin air” required to settle the chronically exploding liabilities as possible reasons why the Fed would likely accommodate more inflation risks and focus on sustaining asset-driven growth (see June 26 to June 30 Fed Dilemma: Too Much Pressure To Continue Hikes).

Figure 3: Ritholtz Research & Analytics: Liquidity Driven Banking Policy

Although over the long term, I think that accrued policy mistakes (out of the fixation towards short-term remedies) and rising default risks are likely to drive interest rates higher.

Another cause of concern is the continuing weaknesses conspicuous in the Arabian markets. The liquidity driven Arabian markets stumbled in December of last year and could have foreshadowed the inflection point of world equity markets last May (see Figure 4).

Figure 4: Ameinfo.com: SC Arab Index

Since the onset of the millennium, stocks have grown manifold and had been supported by abundant petro revenues, ``After growing at the average rate of 25.7 percent in 2005 to $597 billion, this year's nominal GDP for the six Gulf states could exceed $700 billion.” notes Henry Azzam founder and CEO of Amwal Investments.

After peaking last December, the SC Arab index has given back over 40% of its gains. It could be that the parabolic rise caused its market benchmarks to stumble under its own weight or that while liquidity continues to be strong; the explosive rise of its stocks was simply unsustainable or lacked the amount of liquidity growth to sustain its pace. It could also mean that Arab stocks have been responding to the liquidity withdrawal measures adopted by global central banks as shown in Figure 5.

Figure 5: Gavekal: Falling Velocity and Global Markets

According to the very perceptive team of Gavekal Research, ``Unsurprisingly, given the latest volatility on equity markets, the overall appetite for risk has fallen dramatically...Since velocity (the private sector’s propensity to multiply the liquidity provided by central banks) has been the primary source for liquidity and the most important driving force behind the rally of the riskier asset classes, this is a very important development. Indeed, with both M and V in negative territory, markets will now face serious headwinds.”

My concern is if Arab stocks buttressed by robust oil revenues continue founder, it could herald renewed softening in global equity markets as suggested by Gavekal over the interim. Until perhaps the Fed goes into an actual stop and global central banks plays follow the leader, then will we probably see a resurgence of global equities.

For the moment, the Phisix’s close correlation with the US markets represents inauspicious development. Until we see a lucid divergence (see June 12 to 16 Awaiting Asia’s Markets to Diverge from the US) of the Phisix or of the region’s activities relative to the US markets, then it would be recommended that one plays defensive and selectively trade or accumulate on opportunities.

No comments:

Post a Comment