I’d like to also point out that the Philippine Stock Exchange (PSE) recently issued a word of caution to the public on what appears to be growing speculative activities seen in the broad market which I find as quite bizarre or if not ludicrous. According to the PSE, ``Based on the recent two (2) months of trade data initially reviewed, there are nineteen (19) listed companies that have increased its share price ranging from 30% up to 860%, breaching trading bands under the PSE Rules. Total traded volume and value for these stocks were 7B shares and Php2B, respectively, and amount to 10% of the total value of PSEi for the same period. Approximately, 60% of active Trading Participants traded at least one (1) of the stocks in review and 24% traded three (3) or more. These stocks also consistently reached 50% a number of times within the same review period and some for two (2) to three (3) consecutive days. All these activities happen amidst consistent general declaration of the issuers to have no known basis for the steady climb of its share prices.”

While I admire the PSE on its “good faith” for its attempt to curb what appears to be a snowballing of punts or the swelling of speculative activities, it seems that the PSE has overlooked the fact that financial markets in general have intrinsic or natural inclinations to gyrate based on short-term speculations. The PSE should take heed of the words of the prominent industrialist J. Paul Getty, founder of Getty Oil (emphasis mine), ``For as long as I can remember, veteran businessmen and investors – I among them – have been warning about the dangers of irrational stock speculation and hammering away at the theme that stock certificates are deeds of ownership and not betting slips. The professional investor has no choice but to sit by quietly while the mob has its day, until the enthusiasm or panic of the speculators and non-professionals has been spent. He is not impatient, nor is he even in a very great hurry, for he is an investor, not a gambler or a speculator. There are no safeguards that can protect the emotional investor from himself.”

These warnings, instead of generating added public interest towards the market, may prompt for even more aversion on the unwarranted implications that the domestic market is vulnerable to either “gambling” or manipulation. This essentially negates their present efforts (e.g. nationwide roadshows) to boost the demand side in their thrust to advance the cause of enhancing the present state of domestic stock market.

What, I think, needs to be addressed instead, more than just simply issuing inane warnings, is the strict monitoring or surveillance of possible manipulative activities undertaken by cabals or groups intending to hype or corner certain issues. Warnings like these are nothing but bad publicity, yet it actually misses the forest for the trees.

For instance, the PSE glosses over the main drivers of these activities: surplus liquidity! The tidal wave of excessive liquidity throughout the world today has palpably filtered into the local markets through the transmission mechanism of the Philippine currency’s price appreciation. As we have noted previously, a strong peso and declining yields have most likely underpinned these “search for higher returns” phenomenon now manifested via speculative punts. As long as these underlying incentives remain, the trend towards broadbased speculations would likely continue.

Let me divert for a while, in an article, I recalled that the PSE president commented that about only 1% of the Philippine population are invested in the domestic stock market today. 1% of a population of 84 million translates to only about 840,000 individuals! That speaks of how unprogressive and underdeveloped our stock market is. For some to comment that these heightened speculative activities signify a “top” in the market operates on the premises of a lackluster growth of domestic market participants, aside from the presumption that funds circulating within its spheres are limited, which in my view, is highly flawed.

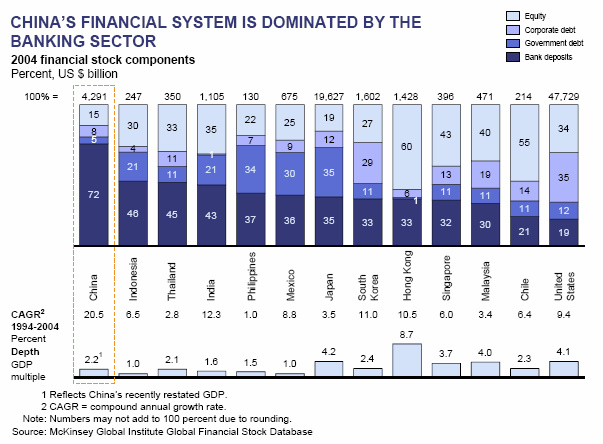

Figure 2: McKinsey Quarterly: Asian Capital Markets

Figure 2 from McKinsey Quarterly is a comparative chart of capital markets of Asia and other select countries around the world. While I extracted this from McKinsey Quarterly’s article about China’s financial markets, the informative expanse of the structural makeup of the region’s capital markets prompted me to include this noteworthy chart in this week’s outlook. It gives us a clue why the Philippines remain at the posterior in terms of economic development.

Except for Japan whose equity markets have been shellacked by a bubble bust down by about 80% from peak to trough, aside from its massive pump priming activities undertaken during its 14 years of economic doldrums which ballooned its debt to about 160% of its GDP, most progressive countries could be observed as having less (or declining) reliance on the traditional sources of funding as banks and governments, while equity markets have contributed significantly to their progress. In the words of market guru George Soros, ``The stock market is one of the most important repositories of collateral”. Yes, we could also see that the corporate debt market could also be one area of growth.

This leads us back to the speculative activities in the market. I have noted of the rising trend in the number of issues traded, where I would theorize that this trend have incorporated new participants and new money into the market, which has provided a flanking support to the largely foreign driven Phisix today.

The local investor base is coming from an extremely low side in terms of penetration level as percentage to the population, ergo if the stronger peso would be able to induce more participation from the domestic investors or even from overseas workers or migrants, let us assume from the present 1% to 5%, you can just imagine the sheer magnitude of support the Phisix would have at its present advance cycle.

That is why I am bullish and would speculate on issue/s that are related to the equity markets itself aside from other possible growth areas in the field of non-traditional finance. Call me a speculator too, in the John Steinbeck (Nobel Prize winner for literature) fashion (emphasis mine) ``I don’t know how speculation got such a bad name, since I know of no forward leap which was not fathered by speculation.”

No comments:

Post a Comment