Yuan’s Dollar Unpegging Opens Portals for Philippine Economic Advancement

A kaleidoscope of earthshaking global events has failed to take away the limelight from the unwarranted fixation of Filipinos on domestic politics. The terror bombings in Egypt, whose causalities have climbed to 88 fatalities as of this writing and the second series of bombings in London and most importantly, the seismic ‘Yuan revaluation’ or the depegging of the Chinese currency from the US dollar for the first time in more than a decade which is now the du jour topic of the global financial markets.

While the Yuan’s peg has been adjusted by only 2.1% from 8.3 to 8.11 to a US dollar, the move towards a “managed exchange rate regime” alters the framework of its peg from the US dollar to a “basket of currencies” which almost similar to the Singapore dollar model. Second, the currency is now allowed to float within a trading band of +/- .3 percent, with the closing prices determined at the end of the trading day.

What is so significant about the Yuan? According to Morgan Stanley Chief Economist Stephen Roach ``

In other words, in the context of global trade dynamics, the symbiotic relationship of

It is true that while the revaluation is miniscule relative to the expected adjustments (anywhere from 15 to 30%), the PBOC is anticipated to adopt ‘baby steps’ in its transition to the new exchange regime, possibly to avoid the risks of having massive disruptions or dislocations in the financial markets that may ripple to the global economy. Further, it is my view that the gradual steps are part of the Chinese central bankers’ learning or experience curve as quasi-independent policy makers.

It is also possible that the recent moves to adjust its currency could be a political statement in response to the souring relationship with

What’s in it for the financial markets? For one, the diversification away from the US dollar and the pegging to a basket of currencies are definitely bearish indicators for the US dollar and US treasuries.

| | | 2004 |

| | Country | in $ Million |

| 1 | | 169,626.20 |

| 2 | | 167,886.40 |

| 3 | | 112,678.40 |

| 4 | | 90,068.20 |

| 5 | | 78,323.80 |

| 6 | | 54,124.30 |

| 7 | | 26,683.90 |

| 8 | | 26,261.10 |

| 9 | | 21,488.60 |

| 10 | | 21,232.00 |

As the Yuan appreciates the cost of imports from

For

Second, after applying administration policies to unsuccessfully slowdown growth to lower the risks of overheating, the revaluation could have been also used as an instrument to temper the fast clip growth momentum as well as to reduce inflation.

Further, the tensions arising from its inability to sterilize excess money in buying US dollars in its monetary system may have the heightened risks of excess credit creation as manifested by the emergence of ‘assets bubbles’ and mounting inflation. The revaluation basically gives

Third,

The other related notable capital outflow policies are the raising of the limits on the amount of money that students and tourists can bring abroad, as well as the current process of loosening restrictions and repatriation of money for foreign owned companies in

Lastly, given the present economic realities such as the surplus capacities brought about by excess business and government investments, rising costs in the coastal areas, transportation bottlenecks, shortage of oil and electricity, China’s present thrusts, according to Simon Hunt of Simon Hunt Strategic Services as excerpted by John Maudlin seems to revolve around ‘focusing on business profitability’, ‘return on capital investment’, ‘value added’ ventures (new technology, more expenditures on R&D and etc.), and expanding inland or rural sectors ``where transport systems have improved, where land costs are a fraction of that in the coastal cities and where wages are one-third or less.” These disadvantages open the doors for opportunities among the region’s low cost producers and other emerging market economies.

Naturally, an appreciating Yuan would translate to more expensive exports for

For manufacturing companies in

For a region that holds about 60% of the world’s population supported by 70% of the global currency reserves, it is of no doubt why our paragon benevolent dictator Mr. Lee Kuan Yew, Singapore’s former Prime Minister in his latest article ‘Rising Asia’ in Forbes forecasts that ``The inevitable surprises will occur, but both China and India are on course for a revival of their glorious civilizations. By 2050 the world's economic center of gravity will move from the

Meanwhile, the US is unlikely to recover the hollowed out manufacturing capacities it has lost to the outsourcing/offshoring phenomenon given that its relative price structure is still way above China and the emerging market economies even considering a 30% revaluation of the Chinese currency.

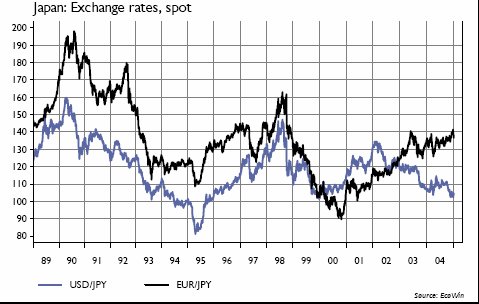

Japan Yen Spot Rates 1989-2004

To aptly quote Dr. Faber, ``Quite frankly I do not understand the thinking of central bankers. Either they think that a strong currency is a problem or they think that weak currency is a problem. The world would be better off if central bankers collectively resigned and let the market fix exchange rates. Then there would never be a problem, in my opinion. In addition, a strong currency has never been a problem in the long run. It forces corporations to become extremely efficient, to innovate and to invent new methods of production. Weak currencies on the other hand are an incentive to compete based on short term favourable exchange rate movements – in nature very much alike protectionist economic policies. I think the Yen could appreciate to one US$ equal 1 Yen and the Japanese would still have a trade surplus with the

Finally, the Yuan revaluation essentially opens the economic opportunity portals for emerging market economies as the