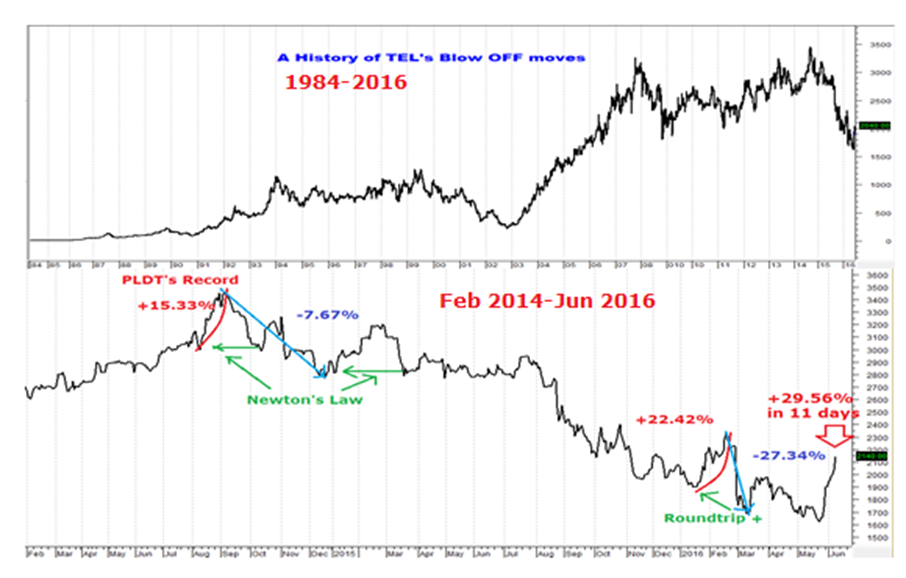

Last weekend, I noted that there were signs of seeming discoordination from the usual end session pumps by the index managers. Likewise, there had been incipient signs of hype and dumps. My point was the destabilizing "in your face" rallies looks to have reached a climax.

Today’s session was a masterful display of the reverse manipulation—a huge marking the close dump!

Today’s session reinforces signs of more forthcoming violent bidirectional price activities.

64% of the PSEi’s 2.41% loss came at the last minute!

These guys could have simply sold at the higher price during the regular time which could have save them some money. So why the dump? A sudden change of mind? To fix the PSEi lower? To setup for a pump tomorrow by buying these back at the opening bell?

Yet such a huge dump would only happen because the biggest market cap had been sold off.

And that’s exactly what had happened. Except for the mines, all of the mainstream indices had been “dumped” at the close. Such only indicates of a coordinated selling of the biggest market cap across the sectors. And so it was.

And the above window shows how the marking the lose dump was accomplished through most of the top 15 biggest market caps.

Such HUGE session end price changes!

Let me emphasize, the above represents the transition or the price changes from the market intervention phase to the runoff period.

The lower window shows of the day’s performance.

So the gist of the end of the day performance had basically been shaped only at the closing bell. Example, 95% of ALI’s 2.63% loss was shaped by the last second 2.5% dump! So four hours and 45 minutes of trading were all considered useless because the only thing that mattered was the end session transition phase.

The PSE should just chop daily trading sessions to just 16 minutes!

Considering how these have been done so frequently (but mostly on the upside) it shows that these guys have essentially no respect for the markets.

And if the markets don’t get their reverence, it reveals of the scale of price and foundational deformities which eventually would lead to its destabilizing unwind or violent adjustments

Today’s 2.41% dump virtually erased most of the three day pump. The PSEi is now up by only .3%. Curiously the headline index is back to 7,550.

And to consider such degree and frequency of price fixing happens ONLY in the Philippines!

Nevertheless as I noted last weekend

And as product of regulators, whom seem to have been asleep at the wheel, the ultimate consequence of such egregious manipulation has been to blow market activities out of proportion or drive them further away from reality.

At the end of the day, market forces will eventually rule: the obverse side of every mania (backed by manipulation) will be a bust.