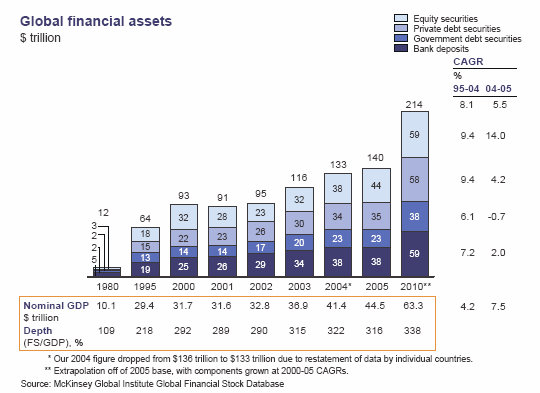

Figure 6: McKinsey Global Institute: 2005 Global Financial Assets

Figure 6: McKinsey Global Institute: 2005 Global Financial Assets

``Information is the currency of the Internet. As a medium, the Internet is brilliantly efficient at shifting information from the hands of those who have it into the hands of those who do not...The Internet has accomplished what even the most fervent consumer advocate usually cannot; it has vastly shrunk the gap between the experts and the public. The Internet has proven particularly fruitful for situations in which a face-to-face encounter with an expert might actually exacerbate the problem of asymmetrical information-situations in which an expert uses his informational advantage to make us feel stupid or rushed or cheap or ignoble.”-Steven Levitt and Stephen Dubner in Freakonomics

Prior to the Christmas break, I was asked if Unit Investment Trusts (UIT) would be a good way to go, for the coming year. To my understanding, UITs operate like mutual funds in the sense that it holds a portfolio of securities. But unlike mutual funds they have been designed for a specific length of time and structured as a fixed portfolio. I was particularly asked, which among the bank’s locally offered portfolio namely, the Peso denominated fixed income, equity or combination of (balance fund), I would recommend, considering the bank’s bullish outlook for the coming year.

To the surprise of the client, my response was to buy US dollars (relative to the Peso) or US dollar short term fixed income instruments and Precious Metals or its proxy (mines) instead.

It is not that I seek to purposely become a contrarian, but my interest considering today’s ambiguous investing climate, is to preserve capital or minimize losses and optimize profits, yet much of today’s optimism comes in the light of a global downshifting of economic growth or a heightened risk environment.

It’s all about Incentives

During the holiday, I came about a very insightful book of which I am in halfway, by Steven Levitt and Stephen Dubner, called “Freakonomics” which essentially deals with how people respond to incentives; to both negative and positive stimulus, something like getting penalized for committing mistakes or receiving awards for a job well done.

Similar to the Austrian School of Economics “Praxeology” which basically deals with the study of human conduct, Mr. Levitt and Dubner wrote (emphasis mine), ``An incentive is simply a means of urging people to do more of a good thing and less of a bad thing. But most incentives don’t come about organically. Someone-an economist or a politician or a parent-has to invent them.”

For instance, in the environment where a country’s currency is rising, mainstream economists would demand for government intervention in support of the export industry, or politicians in response to a public’s outrage would act to impose restrictions or regulations such as the recent “Anti-billboard law”, or a parent would ground their child based on current misbehavior.

And in many instances, as Freakonomics team cites, an individual or the public or society responds to such incentives in manners which have not been anticipated, wherein, as the Freakonomics team says “the conventional wisdom is often wrong”.

Let me cite possible analogies in the local arena; while Economics 101 tell us that rising currencies are essentially bad for exports, why are there “substantially” numerous if not greatly significant cases of Asian, European and Latin American countries with rising currencies YET accompanied by years of rapidly GROWING exports?

Or the Freakonomics team quotes risk communication expert Peter Sandman in New York Times (emphasis mine),``The basic reality is the risks that scare people and the risks that kill people are very different...When hazard is high and outrage is low, people underreact, and when hazard is low and outrage is high, they overreact.” An example would be the dread of death from terrorism than from heart attack.

In the Philippine setting, could the recent Anti-Billboard law as a consequence of a once-in-10 year event, i.e. Typhoon Milenyo’s direct hit to

Since there are three basic forms incentives, moral (how the people would like the world to function), social and economic (“how it actually does work”-Freakonomics), I would relate to the latter with respect to this field of endeavor.

In such light, the economic incentives for brokers, bankers, fund managers and investors are divergent. Brokers earn by commissions, thereby our incentive is to encourage market participants to trade more. Bankers, on the other hand, earn by fees, whereby to entice the public for more placements opportunities by offering more products, while fund managers earn by a combination of fees and profit-sharing scheme, where the purported incentive is to earn from more placements and investing profitably (return based).

While the investing public seeks to grow their money through the incentives of “rate of returns”, it is incumbent upon them to understand the incentives of the intermediary they deal or transact with. Simply because the investing public’s incentives more often than not varies and could, in fact, be in conflict with their intermediary’s interest.

So it would be natural for bankers or fund managers or brokers to promote their product line or services regardless of the return outlook because it is their “economic incentive” to do so.

The Wisdom of Conventional Thinking

Now relative to the “wisdom of conventional thinking”, today’s investor sentiments emanating from the recent buoyancy in global equity markets could be depicted through this newspaper heading...

Figure 1: SCMP: December 30 Headline: “20,000” Roaring Through

For money managers, these are known as the “Magazine Cover or Newspaper Headline” indicators, a contrarian signal. Since the “incentive” of the press is to “sell its media to the public”, it usually does so by conveying recent developments backed by a STRONG consensus view. In other words, they vend information which caters to mostly what the public wants to hear about.

This reminds me vividly of the yearend 2004 where several magazines as the Economist declared the “Death” of the US dollar following two successive years of rout. In 2005, the US dollar simply proved the consensus wrong by rebounding mightily across the board.

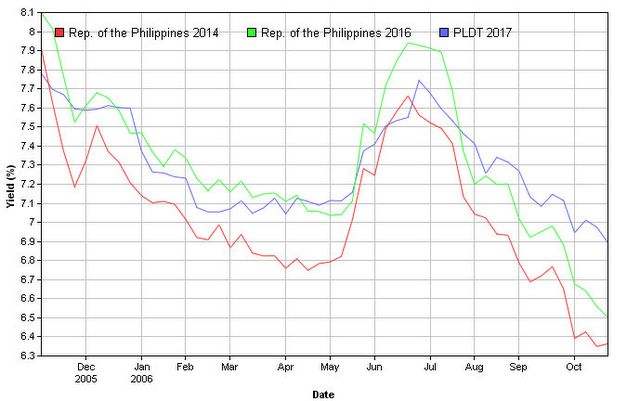

Figure 3: Asianbondsonline.com: Declining Yield Spreads of on Major USD Philippine issues

Yes, while it is true that weakness in the

The Peso gained 7.69% in 2006 to Php 49.03 per US dollar supported at the margins by these massive portfolio investments into the Phisix, the Philippine debt instruments in both local and dollar denominated issues as shown in Figure 3 and other asset classes. Of course, remittances have been a factor, yet as we argued before, it is the unseen working at the margins that have shifted in favor of the Peso.

As evidence to this, remarkably, the spread of the 10-year Peso Philippine denominated Treasuries and the 10 year US dollar denominated Philippine Treasuries has narrowed to only 34.9 basis points as Friday (Jan 05), from 278.4 basis points at the end of 2005 (Dec 29th).

The thinning of the spreads astonishingly reflects on the enormous money flows into Philippine assets mostly on the grounds of a global low risk premia and low volatility aside from the moving out of the risk spectrum in the stretch for yields mentality.

Of course, local analysts and experts will construe these as mostly reform based since they hardly comprehend the dynamics of the macro cycle which the local media would unsparingly carry up. To quote again Mr. Levitt and Mr. Dubner, ``Journalists need experts as badly as experts need journalists. Every day there are newspaper pages and television newscasts to be filled, an expert who can deliver a jarring piece of wisdom is always welcome. Working together, journalists and experts are the architects of much of conventional wisdom.”

Increased Portfolio Risks Plus Unfavorable Cost-Return Analysis

Figure 4: IMF: Sub-Saharan

Since I believe that today’s directional path of money flows are inexorably moored towards the fate of the US dollar [US dollar index -9.01% in 2006], we might as well consider the recent actions which may be as well be indicative of the directions of the Phisix and related Philippine assets.

I have argued in November 27 to December 1 (see Falling US Dollar Fuels Rising Oil Prices) outlook that aside from “demand-and-supply” factors the prices of oil or other commodities could be determined by the gyrations of the currencies where they are predominantly traded in, i.e. US dollar. For instance as oil prices recently swooned, media outlets took the quick-and-easy version of a warmer weather attributed to its actions. Nevertheless, oil’s decline came about as the US dollar massively rallied.

Which brings us to the unseen, could the inverse relationship of commodities and the US dollar signal a demand contraction and a rise in risk aversion similar to the case last May?

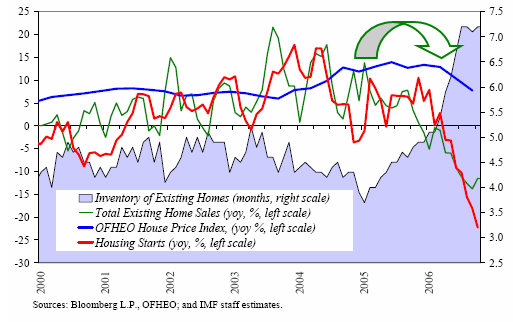

Figure 5: IMF

Warns the IMF (emphasis mine), ``The shift in recent years toward more risky mortgages may make segments of the mortgage credit markets more vulnerable to the deceleration in housing prices. Innovations in the origination of mortgages have allowed a widening range of borrowers to finance more expensive homes at a given income level. These include mortgages for subprime borrowers, mortgages with high degrees of leverage, and mortgages that feature sharply rising monthly payments, resulting in “payment shock” (Figure 10). More than half of mortgages originated in 2005 and 2006 are estimated to contain provisions that will eventually lead to a sharp rise in payments, even if the level of market interest rates does not change.

``Furthermore, as shorter-term interest rates have increased in recent years, rising payments on conventional adjustable rate mortgages will add to payment shock. Although the overall level of home equity remains high, a recent study suggested there may be significant pockets of home purchasers with low or negative equity; that is, mortgage debt in excess of the value of their homes. This may owe to several factors, including falling home prices in some regions, mortgages that initially allow for a buildup of debt over time, and the fact that some homeowners may have overpaid for their homes at the speculative height of the market, facilitated by overly liberal underwriting. Thus, homeowners with small or no equity cushions in their homes may find the payment shock difficult to manage.”

The good news is that so far the housing recession has been contained to within the industry premises. However, as the IMF warns, adjustments to subprime mortgages, which could have a significant impact and may translate to more tightening of belts by the US consumers, which has been the single most important engine of growth on the demand side for the global trade structure.

Lest be accused of the logical fallacy of “Cum Hoc, Ergo Propter Hoc” [With this, therefore because of this], we are curious to know if the inflection point seen above are correlated, since they broke down almost simultaneously? And if this could be reflective of the lagged effects of the above stated US housing recession? Or does this effectively represent a diffusion of the weakening of the

Writing prior to the recent rally of the US dollar Chief Economist Paul Kasriel of Northern Trust last December to give us a clue, ``This weakening in copper prices corroborates the slowdown in the pace of U.S. manufacturing activity – it appears as though manufacturing output peaked in August 2006 – and the recession in housing. The decline in the dollar price of copper is all the more indicative of faltering goods-producing activity in the

A benign decline of the

Thus likely, as shown in Figure 7, the inverse correlation between the US dollar and emerging market equities have been quite strong over the past year. To wit, as the US dollar rallies emerging market equity indices tend to decline, while emerging market bourses rally when the US dollar index is on a downshift.

Figure 8: IMF: Correlation of Asset Classes with S & P 500 and Broader Market Volatility

To quote the IMF, ``If these positive correlations were to persist, or even to rise, in a sell-off, the traditional diversification benefits of investing in a wide variety of asset classes might be less than investors expect. The possibility that the correlations may persist underscores that investors may eventually demand higher risk premiums.”

What this implies is that going forward considering the hefty advances of the Global Equity Indices (“priced for perfection”), as well as the Phisix, considering the record low volatility, tight credit spreads, extreme optimism (newspaper cover), the diminution of seasonal strength, the non-confirmation of Dow Theory (see December 4 to 8 Dow Theory: The Emergence of a Divergence?), technically overbought conditions, mean reverting cyclicality and tendencies of the financial markets, rising correlation among diverse asset classes, conflicting messages by the bond and equity markets, the recent massive decline of broad based commodities, a rallying US dollar, an inverted yield curve, rising potentials for “volatility” shocks (while the Euro is down lately, the Yen is up- further increases in the Yen could unnerve the widely utilized Carry Trade) and uncertainties towards the ripple effect of the present slowdown in the US suggests of Increased Portfolio Risks. Of course, aside from our oft mentioned “Fat Tail” or Sigma risks.

This coupled with the rising cost of our capital over potentials returns on our invested capital makes the investing in the local UITs a less palatable proposition today. Sometime in the middle of 2007 could be a good entry point.

``All man's troubles come from not knowing how to sit still in one room.” Blaise Pascal

While I remain bullish over the long term with the Phisix (10,000 Phisix...conservatively) as well as with the Peso and would not discount a potential mania to top out the present cycle, I am inclined to think that there could be a significant correction over the interim, possibly anywhere 10-25%; remember the Phisix is an illiquid market by global standards and illiquid markets translates to above par volatility (high beta), and that the Philippine markets could possibly stage a strong rebound during the latter half of the year.

All this will essentially depend on the developments in the US dollar [I know the Euro will surpass the US dollar as the most circulated currency] as a fundamental driver as well as, the US financial markets which has, in my view, been the focal point of cross-border capital flows, and the inspirational paradigm to the world equity markets during the last quarter of 2006.

I do not foresee present day decoupling by Asia vis-à-vis US (see November 20 to 24 Asia’s Soaring Markets: A Matter of Decoupling from the

The Phisix could possibly end the year on the negative or trade sideways where gains or losses would unlikely top 5%.

I have been right with gold having reached the $600-650 level (closed at $604.9) which I forecasted early this year see Jan 02 to 06 2006 (2005 Recap and Blemishes: 2006 Still For Mines and Oil) and forecasts the potential of gold to decouple soon with its industrial metal siblings. Gold’s latest decline has been attributed to diminishing “inflation” concerns and to a surging US dollar.

If the market savants such as the world’s Bond King Bill Gross are right to predict that the US Federal Reserve will cut rates from 5.25% to 4.25%, I can see gold topping the $700 at the close of 2007, alongside another key commodity, crude oil possibly in the $60 to $70 mark, this despite a worldwide slowdown on possibilities of greater than expected “peaking out” of maturing fields (for as long as the world does not enter into a depression-where all bets are off).

Meanwhile the US dollar index would possibly close lower for the year but at a much subdued loss than in 2006 possibly at 5% or less.

Because the PSE made substantial adjustments to the composition of the Phisix subsectors which took effect last January 2, 2006, I based the yearend returns on the first day from which the changes were adopted.

The mining sector which I predicted as the best performer for 2006 came in a very close second with gains of 65.2% to trail the Holdings at 66.67%. The other sectors came in the following order, Property 51.12%, Service 45.71%, All index 45.13% Banking 35.07% and CI 19.34%.

Unlike other mainstream analysts whose fungible views are dependent on the present activities of the market which they use to project into future, I remain steadfast in my projection that the juvenile mining sector has the potentials to draw even more investments, considering the “nationalization” efforts undertaken by several resource rich nations (Bolivia, Russia, Venezuela, Mongolia & etc..) which in essence reduces potential supplies on stream, and makes the country even more a compelling supply chain participant.

Of course, our projections are based on the sustenance of a “mining friendly” climate, that should be able to draw on foreign investments and generate more corporate stories and activities that would drive local investors into the mines.

And this should include the power and energy sector which has undergone years of intensive underinvestment, aside, from the much neglected agriculture based investment themes-arising from declining supplies of arable land due to growing desertification trends, a looming water crisis in various parts of the world, growing industrialization in emerging markets, demographic and urban migration trends as well as demand for agriculture products which used to be solely for food is now in competition as feedstock for alternative energy and most importantly, the growing consumption trends by rapidly developing emerging markets economy.

Furthermore, while many world markets have seen a boom in real estate, the

Another compelling investment theme would be the rapidly growing “sunshine” Business Process Outsourcing industry (BPOs), a beneficiary of today’s supply chaining trends in globalization. A global economic growth slowdown should benefit BPOs more as companies attempt to reduce costs and outsource more of their non-sensitive business processes. Also watch for companies that would benefit from various outsourcing/offshoring patterns, as well as beneficiaries from growing trends to integrate financial markets.

Finally, it is never good to discount that the Philippines sits on a wealth of potential high value tourism spots given its 7,100 islands, rich historical background and diverse culture. As

One of the fundamental risks in today’s world is the rising tide of protectionism. As in the case of

Mainstream economists whose analysis influence policymakers are wont to believe that rising currencies curb exports. While such is a textbook dogma, the reality is different. Rising currencies of many Asian countries for several years hasn’t curtailed exports, so as with many Latin American and European countries. What you have is a global phenomenon of rising currencies and rising volume of exports, the probable reasons of which I may write about soon. In short, policymakers have been barking at the wrong tree. Exchange rates are usually made by policymakers as scapegoats for their inefficiencies. This is the same premise adopted by US politicians in pressuring

It was an ASEAN contagion as a general response to

P.S. Following the dramatic bloodbath, the Thai Government has made a ludicrous U-Turn, according to CNN

"The Thai government performed an abrupt U-turn on Tuesday after the stock market suffered its worst fall in 16 years as foreign investors pulled the plug in response to drastic measures to rein in the baht.

"Hours after the central bank rebuffed a plea from a stunned stock market chief to withdraw them, Finance Minister Pridiyathorn Devakula announced equity investments would be excluded from the restrictions, starting Wednesday.

Well, that's what to expect from governments.

``Accuracy of observation is the equivalent of accuracy of thinking." Wallace Stevens, American Poet, (1879-1955)

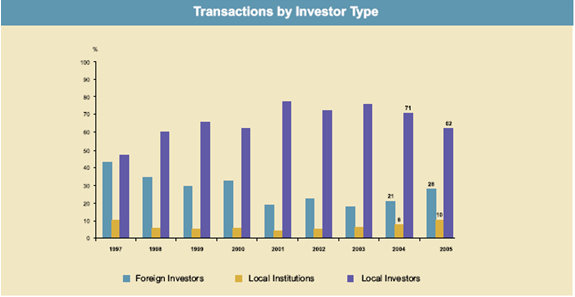

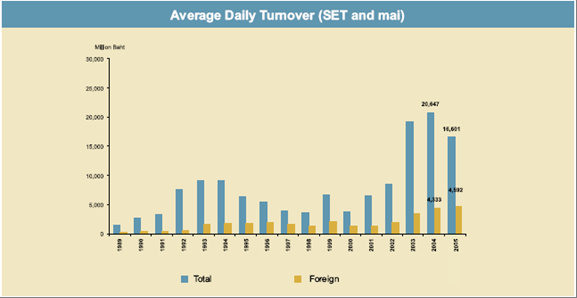

Here are some important facts of note:

1.

2.

3. The Average daily turnover of is a whopping USD 409 million in 2005 against a measly the

4. Local RETAIL Investors constitute the majority of investors; although on a declining trend relative to market share, but has likewise increased in terms of nominal volume since 2003.

5. On the other hand, Foreign Money constitutes a significant growing minority!

6. According to IMF data,

When economic analysis centering on comparisons about certain countries omit the financial market aspects, then it is not representative of a meaningful picture or analysis.

Why? Today’s global economy is much more dictated by the financial world than the actual exchange of widgets and services. Global Market Cap for the collective stock market is said to be at over USD 43 Trillion which is almost the same scale as today’s Global GDP.

Combined, the world capital markets broken down into sovereign bonds, corporate bonds, bank deposits and mortgage securities are at over an estimated 1.7 times the world economy!

Now relative to

Investors who continue to immerse themselves into the illusion that the local factors have been the key determinants of the domestic market will be left holding the proverbial “empty bag” or would be caught “swimming naked” when, to paraphrase Mr. Buffett, “the tide goes out”.

No markets are essentially single-variable/dimension determined over the long term, although in one instance or another, a variable may outweigh all others given their influence to the collective investors.

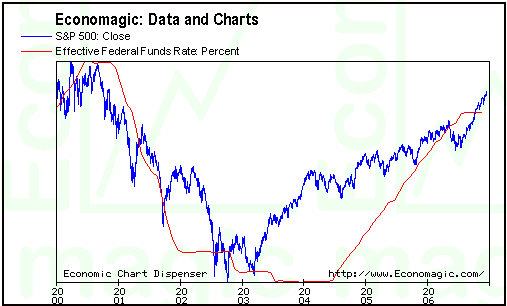

One of the most crucial factors that I’ve been repeatedly arguing for as major drivers to our financial markets or of the worlds’ is of global liquidity.

When the US Federal Reserve fretted upon the shadows of a Japan-like Deflation bugaboo, following the technology bust in 2000, they undertook an aggressive massive campaign to flood the world’s monetary system with surplus money and credit. The Fed took down its interest rates to its lowest levels in about half a century, as shown in Figure 7. This essentially prompted investors to take upon massive leverage worldwide in different trading forms, such as the widely known CARRY Trade.

Notice that all the indices mentioned above found their bullish stimulus almost synchronically in 2003. It likewise appears that almost all variants of asset classes [bonds, collectibles, stocks, commodities and real estate] around the world have responded to the US Fed’s easing.

Yes, the FED did take steps to increase its interbank lending rates 18 times to 5.25%, from its trough in June 2003, but essentially in nominal figures it remains lower compared to the past.

One should not forget that the present monetary system is based on the US dollar standard and that policies encompassing the US dollar have greatly weighed on the performances of various asset classes, if not among economies.

Yet, another supportive role of today’s fiat money based asset economies has been the increasing importance of new financial instruments, such as structured finance and the various strains of derivatives, aside from the technological innovations in the areas of information and communications which have transformed and enabled real-time money flow platforms that has essentially facilitated global money flows using the click of a mouse.

``Each believes easily what he fears and what he desires."-Jean de La Fontaine French Poet (1621-1695)

This week’s huge inflows of foreign money (a startling P 12.25 billion!) have been mostly due to the very successful PNOC Exploration listing (+34.375%), an issue whose foreign take up I had gravely underestimated. PNOC’s fundamentals have been very impressive at least, but given the performances of its peers (yes, here I was guilty of extrapolating the past for the future), and the likelihood of the prospects of an interim “top”, I have been wary of the possibility of mistiming. Besides, short term gains are for those with especially high risks appetite!

Further, there have been sporadic chatters about the risks of a huge IPO listing siphoning liquidity out of the market. As I have been arguing about liquidity driven markets, the PNOC experience, which raised about P 16.2 billion from its listing, simply proved that there had been simply too much money out there chasing for returns, both in the domestic and the international sphere, as the Phisix continued its upward trek in contrast to some expectations of a liquidity drain.

Anyway, since successful investing in the market is mostly about opportunities management, there are even more propitious opportunities in the offing given the present secular phase of today’s domestic market.

As an aside, last week I pointed out that while local investors who appear to be on a selling mode, foreign money continued to pile on local assets, where I argued the latter would influence the former. It appears that such observation came true as the number of traded issues and number of trades combined with the general market breadth improved considerably to manifest of improved sentiments from local investors.

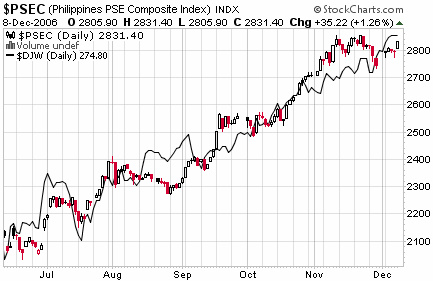

The Peso hasn’t been much of a factor to the Phisix until 2005, where as shown in Figure 8, peaks of the Phisix coincided with the peaks of the Peso or troughs of the USD/Peso.

The interim bearish factors for the Phisix today, which as shown above is highly dependent on foreign capital, are mostly due to exogenous risks as mentioned previously, the record low volatility and extremely complacent global investor sentiment and frothy market action, the technically overbought conditions, growing divergences of a Dow Industrials relative to the Transports, and record levels (1987 highs) of insider selling in the US markets.

Aside from of course, fundamental “fat tail” risks from a greater-than-expected global economic growth slowdown, rising tide of protectionism, an abrupt fall or a US dollar crisis, a nuclear war, global pandemic or perhaps a meltdown of global credit house of cards. For the meantime, any reversals could be more cyclically driven than structurally based.

Given the near closing of the season which has likewise underpinned today’s upbeat outlook here and abroad, I would be very cautious about positioning into the market, and surf the momentum instead.

Given too, the periodicity of the rally here and overseas, which is about nearly half a year already, as noted previously, we could be at the near end or at the maturity of the present cycle which heightens our risks profile while at the same time limiting our returns potentials.

Remember that no trend goes in a straight line and today’s bullish cycle could end sooner rather than later.

Yet of course, one cannot discount a speculative blow-off top as a culmination to the present cycle, yet as we surf the tide we need to tighten our stops, especially as the markets gets frothier.

``The precipitous drop in the dollar shows how investors around the globe are very concerned about American deficits and debt. When government policies in a fiat system are the sole measure of a currency’s worth, the currency markets act as a reliable barometer of how those policies are viewed around the world. Politicians often manage to fool voters and the media, but they rarely fool the financial markets over time. When investors lack faith in the U.S. dollar, they really lack faith in the economic policies of the

In a rather buoyant climate for world equities, upbeat sentiment levitated our Phisix, alongside most equity benchmarks, to a remarkable 1.54% advance over the week to regain most of its losses following the two consecutive weeks of retreat, as shown in figure 1.

Figure 1: stockcharts.com: Phisix and Dow Jones World Index

The shift to lower gears (red arrow), which is a representation of divergence from a sturdy uptrend of the Phisix, could have been a signal of the recent correction.

How can we say so?

``Political risk is no respecter of boundaries, and

I made my case in my previous edition, Should You Invest in the Phisix Today? (See Oct 23 to 27 edition), where I believe today’s bullish interim cycle is close to its maturity, subject to risks of correction from the market cycle’s mean reverting tendencies, aside from risks of arrant complacency and a murkier economic outlook for 2007.

So far global liquidity remains unblemished. ``While US commercial banks continue to provide lots of liquidity to the domestic economy, US mutual fund investors continue to do the same for both the US and overseas stock markets. These investors poured $592 billion into mutual funds over the past 36 months through October. They've done very well for themselves. The net asset value of US mutual funds increased $2,232 billion over the past three years to $5,670 billion. So, net capital gains totaled $1,641 billion over this period. Over the past 36 months, $333 billion, or 56%, of the inflows into US mutual funds poured into funds that invest overseas”, comments the ever Panglossian Dr. Ed Yardeni of Oak Associates Ltd.

Figure 6: BCA Research: Emerging Markets Preparing for a breakout

{kind=link}