``There are a terrible lot of lies going around the world, and the worst of it is half of them are true.” Winston Churchill

FORECASTING markets, particularly over the short-term, is an incorrigibly tricky pursuit. Variable gyrations and wildly random pendulum swings characterizes the market’s volatility whose directions over the short term are as good as a “throw of dice”. Curtly said, your guess is as good as mine. In the words of Benoit Mandlebrot, author of the Misbehavior of Markets, ``All is not hopeless. Markets are turbulent, deceptive, prone to bubbles, infested by false trends. It may well be that you cannot forecast prices. But evaluating risk is another matter entirely.”

And risk evaluation and assessment is what distinguishes us from the rest of the domestic playing field, simply because our paramount aim has been to preserve capital, aside from maximizing profit opportunities and containing losses.

Of course, we try to heed on Warren Buffett’s invaluable advice of reading and applying on Ben Graham or Phil Fisher’s principles in relation to the “macro” stuffs, and don’t engage in equations with “Greek” letters on them, especially on “technical grounds” as some others do.

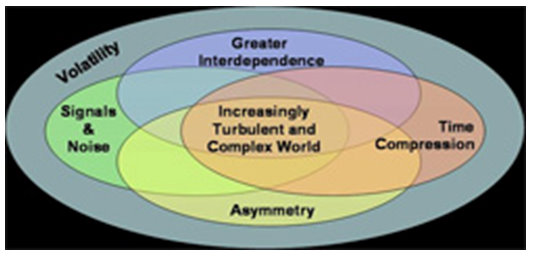

Figure 1: Guardian: World Economic Forum: Complex and Interconnected Global Risk Environment

I have interminably argued that today’s market landscape has dramatically shifted, such that the “Globalization” platform phenomenon backed by the “technological telecommunication and information revolution” has tremendously increased the interconnectedness or the correlations of our market’s movements with that of the world’s. In doing so, our domestic market have now been subjected to the ebbs and flows of global capital, sharing with it, as much of its benefits, the risks of an “increasingly complex and turbulent complex world” as shown in Figure 1.

Notes the World Economic Forum in their Global Risks 2007 (emphasis mine) ``In an increasingly complex and interconnected global environment, risks can no longer be contained within geographical or system boundaries. No one company, industry or state can successfully understand and mitigate global risks.”

All this goes to show that for as long as the world continues on its path towards the evolution of greater economic and financial interdependence, its markets, business environments, national and macro economies, aside from political, social and cultural dimensions are likely to evolve towards encompassing more developmental convergences, relative to risks and benefits.

With no less than the recent ASEAN meeting in held in our Cebu to corroborate on this perspective, according to China’s Xinhua/People’s Daily Online (emphasis mine), ``In the signed document, ASEAN leaders reiterated their conviction that "an ASEAN Charter will serve as a firm foundation in achieving one ASEAN Community by providing an enhanced institutional framework as well as conferring a legal personality to ASEAN."

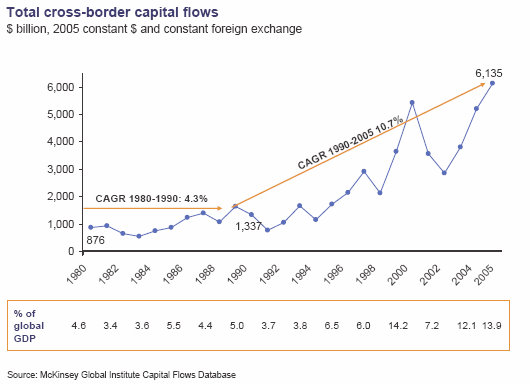

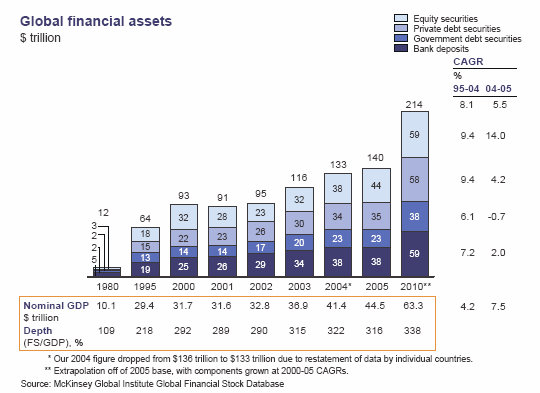

Figure 2: McKinsey Global Institute: Record Cross-border Capital Flows

In addition, as testament to a world of greater integration, global capital flows have reached record levels where the Compounded Average Growth Rate (CAGR) has steepened to an average of 10.7% per annum during the last 15 years compared to 4.3% during 1980 to 1990 period, as shown in Figure 2, where in such environs the emergence of the global investors class has evolved.

In its 3rd Annual Report, McKinsey Global Institute, noted that (emphasis mine), ``In 2005, worldwide cross-border capital flows, which include foreign purchases of equity and debt securities, cross-border lending, and foreign direct investment (FDI), increased to more than $6 trillion, the highest level ever. Since 1990, cross-border capital flows have grown 10.7 percent annually,10 outpacing growth in world GDP (3.5 percent), trade (5.8 percent), and financial stock (8.7 percent). Advances in technology and the deregulation of financial markets around the world have enabled this growth and given rise to a growing class of global investors. Although investors in most countries still show a marked preference for financial assets of their home country, roughly one in four debt securities and one in five equities today is owned by an investor outside the local issuing market—for instance, a US investor buying Thai equities, or a German investor buying US bonds. National financial markets are increasingly integrating into a single global market for capital.”

Plainly stated, much of the world’s developments matters for us today than the “wisdom of conventional thinking” would have it. To paraphrase New York Times’ columnist Thomas Friedman in his bestseller, the WORLD is indeed becoming FLAT.

For us, business or financial models or paradigms and market analysis would have to deal with the instrumentalities of present realities rather deluding ourselves of insularity.

To be get ahead of the curve, one has to learn how to adopt on the strategies or approaches underpinned by the present trends and risks, otherwise lose out to either obsolescence or competition.

Which brings us back to our risks analysis, the World Economic Forum (WEF) through their Global Risk Network identifies 23 global risks subdivided into the segments of economics, environment and geopolitics, The Guardian quotes the WEF warning (emphasis mine), ``Expert opinion suggests that levels of risk are rising in almost all of the 23 risks on which the Global Risk Network has been focused over the last year, but mechanisms in place to manage and mitigate risk at the level of businesses, government and global governance are inadequate."

The WEF enumerates the five major economic risks namely, an oil price shock, a plunge in the US dollar, a hard landing in China, budget crises caused by ageing populations and a crash in asset prices, which has been ``more acute than at this time last year”.

It also cited worsening instances of the four out of five environmental risks, particularly climate change, loss of fresh water supplies, tropical storms and inland flooding.

Aside from the incremental escalations in six geopolitical risk factors, specifically, international terrorism, WMD, war, failed states, instability in the Middle East and a retrenchment from globalisation. The WEF warns that if such factors tip into a degree of intractability, ``the environment for business and society could be changed beyond recognition."

True, today’s financial markets have been discounting much of these factors, in fact, the world equity markets appear to be exceedingly ebullient.

While some domestic technical “experts” have claimed in consonance to my view that today’s market has been quite overheated, following a semblance of retracement, the Phisix and the global markets rallied sharply at the end of the week which once again took queue from the actions in the US markets, despite the asymmetric or discordant signals from the broader financial markets (rallying US dollar and gold, declining bonds, copper and oil.) as shown in Figure 3.

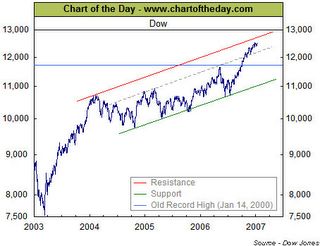

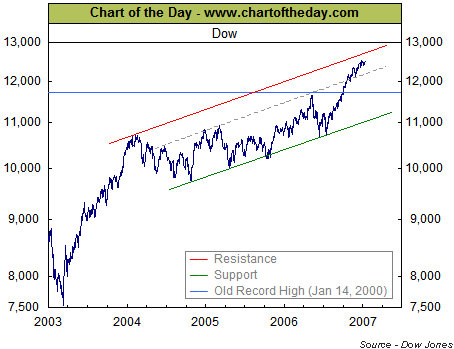

Figure 3: ChartoftheDay.com: Dow Jones at Critical Juncture

Here chartoftheday.com says that while the Dow is in critical juncture following the string of record high closes amidst its astonishing climb in a backdrop of a litany worries, it has to yet hurdle its three-year trading channel to steer clear of technical obstacles, which incidentally could also prove to be its decisive bump.

Figure 4: Stockcharts.com: Phisix, Dow Ex-Japan Asia Index and the Morgan Stanley Emerging Free

However, if you take a gander at figure 4, the Dow Jones 1800 Ex-Japan Index (black line superimposed), a benchmark consisting of 1,800 companies throughout Asia, the Morgan Stanley Emerging Free Indices (black line lower panel), a benchmark of the broad universe of emerging markets “developing economies” benchmarks and the Philippine Phisix, the movements including short-term fluctuations have been almost similar to the extent that the recent retracements or even the “timing” at the end of the week rally appears to have been “orchestrated”. No conspiracy theory here, just a depiction of the congruity by global markets.

And to consider the Philippine setting, today’s market activities have been envisaged by massive outperformances of companies with little fundamentals. Formerly dormant companies with little or no operations have been taking the centerstage accruing mouth-salivating gains that have been attributed to corporate stories of potential backdoor listings, Mergers & Acquisitions and/or plain vanilla “push” by certain interest groups.

The recent easy gains have ostensibly lured vulnerable retail investors, the last among the investing group to get involved, to undertake aggressive moves in the broader market.

Such conspicuous froth have been simply reflective of an outgrowth of an accelerating speculative mindset, where one could even hear arguments stating that “nothing in the local arena poses as significant threat to present conditions”.

.bmp)

.bmp)

.bmp)

.bmp)

.bmp)

.bmp)

{kind=link}