``And when voters get scared, politicians leap into action. Unfortunately, fast government action almost always results in irrational action.”-D.R. Barton is the editor and founder of Traders’ Tuesday, and editor of the E.S.P. Profit System.

One of the discordant messages or might I say “conundrum” painted by today’s market has been the surprising underperformance of gold. In the wake of the Fed’s decision to hold in abeyance its interest rate hikes, gold has plunged by about $50 over the past weeks under the rationale of “lower inflation concerns” or “mitigated geopolitical risks” or “dragged by oil”.

I find such arguments as absurd. The benchmark precious metal has basically thrived on uncertainties in every known dimension (be it politics, economic, financial, monetary etc..). While the war in Lebanon may have temporarily led to a multilateral brokered settlement, the overall political climate in the Middle East remains as tense and poses as potential powder keg.

Listening to the US former Secretary of State Henry Kissinger’s interview at the Bloomberg, I have to share his view that the ceasefire interposed by the UN may not last considering that the Hezbollah is unlikely to acquiesce on disarmament. Furthermore, the Hezbollah claimed victory as the first Arab group to have dragged the Israelis into a war of attrition of which compelled their archrival to a ceasefire unlike the outcomes in 1948, 1956, 1967, 1973 and 1982.

George Friedman of Stratfor gives an incisive comment (emphasis mine), ``The group did not conduct offensive operations; it was not able to conduct maneuver combat; it did not challenge the Israeli air force in the air. All it did was survive and, at the end of the war, retain its ability to threaten Israel with such casualties that Israel declined extended combat. Hezbollah did not defeat Israel on the battlefield. The group merely prevented Israel from defeating it. And that outcome marks a political and psychological triumph for Hezbollah and a massive defeat for Israel.”

Now with a psychological booster gleaned from the recent proxy war, backed by oil surplus oil funds, what stops the Hezbollah and/or its patrons (Syria and Iran) from expanding the theatre of war to attain their politically desired objectives or agenda?

Another fuzzy excuse is of the “slowdown” or “lower inflation” concerns; monetarist proponent and Noble laureate Milton Friedman once said that “inflation is always and everywhere a monetary phenomenon.” This means that inflation has less to do with state of economic growth since it is always and everywhere about money and credit. Morgan Stanley Andy Xie explains the present environment best, in my view:

``The basic reason for rising inflation is that global real policy rates are less than half of, and global inflation 50% above, average levels over the past decade. Real interest rates are not high enough to exert a headwind against inflation.

``The risk of accelerating inflation is even higher, considering that central banks have pumped enormous liquidity into the global economy over the past decade. Until recently, the inflationary effect of the liquidity was held back by deflationary shocks. Instead, the money inflated asset markets, which, in turn, boosted global demand.”

Where consumer demand may have been temporarily curtailed driven by a deceleration of the US real estate industry, the transmission mechanisms of the inflationary policies by global central banks could be channeled into other areas of interest by the speculative community. Hedge fund dabbling on the field of property catastrophe reinsurance or betting on weather outcomes is just one of such vivid manifestations.

Has the recent rise in global equity markets, despite the semblance of a tightened money environment, as manifested by the full inversion of the yield curve spectrum in the US, presuppose a future or forward easing by the US Fed? Are the actions in the financial markets today, compelling central bankers around the world to adopt a more investor or market friendly regime?

In addition, the argument that oil has dragged gold lower fallaciously presumes that inflation is driven by energy rather than excess liquidity stimulating inordinate demand for oil or oil as a major beneficiary from inflationary policies that has lowered the “price value” of the US dollar relative to oil.

Further, real interest rates will have to climb further to wring out “inflation” or excess liquidity out of the system similar to the actions of former US Fed chair Paul Volker in 1980; something of which “measured” pace of rate increases by global central banks are unlikely to accomplish.

In short, inflation is very much embedded and entrenched around the global financial and economic system and would most likely find its way in different outlets, unless global central banks act decisively. Moreover, as discussed previously, political expedience and credibility concerns are likely future drivers for sustained inflationary growth. So in essence, the financial markets appear to be “mispricing” or underrating the relationship of gold to a prospective slowdown, the oil-gold affinity and easing of geopolitical concerns.

One more thing; because inflation is essentially what Central bankers stand for, controlling inflation expectations is one of their major functions. And for a little spice, let me add my conspiracy theory.

While it is summer period in the in the US and Europe possibly much of the market participants could be off from work for a vacation which leads to relatively light volume of trades in the markets.

In the meantime, European central banks have been significantly behind schedule in offloading their gold holdings allotment under the 15 member European Gold Agreement (EGA) by about 169 tonnes which ends in September 26th, according to Resource Investor’s Charlotte Mathews, ``In the year to this September, the signatories were permitted to sell 500 tons of gold but by the end of July they had sold only 331 tons. They cannot carry over the allocation from one year to the next.”

It could be that central banks have taken advantage of the present “lean season” in the financial markets to carve out a “low inflation” scenario to “manage the public’s inflation expectations” by unloading the remaining balance of 169 tonnes. Of course, heavy selling on lean volume equates to lower prices, which is possibly what we are seeing today.

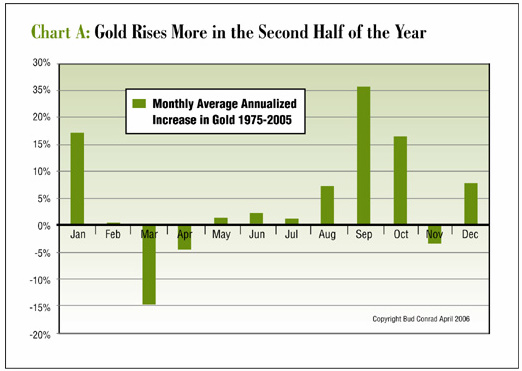

However, as a matter of seasonality gold appears to be entering its strongest period as shown in Figure 6.

Figure 6: CaseyResearch.com: gold Rises more in the Second Half of the Year

According to market savant Doug Casey, ``As you can see in Chart A, which summarizes gold's monthly price moves over the past 30 years, the yellow metal typically shows weakness from February to April, rallies in May, then heads down for summer. In August, gold typically begins to rebound and moves up pretty much for the rest of the year. Of course, this is an average pattern, not an invariable one. In 10 years out of the last 30, gold dropped in the fourth quarter. Even so, the long-term data suggests the average pattern is worth paying attention to.”

So what drives gold higher during the second half?

Seasonal jewelry purchases, according to CNN, ``September and October are key holiday periods in China - the mid-autumn festival -- and India -- the revival of the wedding season -- and precede Christmas purchasing in the OECD countries.” Aside from of course, Christmas shopping in the US of which gold is sold most during the fourth quarter or about half or 45% of the annual gold jewelry sales in 2005 according to Resource Investors.

Market maven Mr. Casey remind us of India’s share as a major consumer of the gold jewelry segment as substantial, he says ``In fact, in 2005 Indian gold jewelry sales rose by 25%, and now that country takes credit for about 23% of the world's consumer gold sales. The U.S., at #2, takes down just 12%.”

Figure 7 shows that during the past three years, gold has markedly used August for its springboard towards a yearend rally.

Figure 8: stockcharts.com: HUI Amex Gold bugs follows gold’s footsteps?As a matter of benchmark, I used the composite HUI Amex gold bugs index representative of unhedged gold mining stocks as possible clue to the movements of local mining shares counterpart. In figure 8, the HUI index has also followed the footsteps of gold during the past 3 years as to mounting a last quarter rally.

To recap, the present movements of gold appears to be founded on nebulous grounds; low inflation/demand slowdown, oil as a drag and mitigated geopolitical risk, as the inflation scenario remains deeply entrenched into the system and remains a politically expedient and “credibility” friendly alternative to politicians and their bureaucrats compared to the “deflationary option” while geopolitical environment remains critically volatile despite present news accounts.

It could be that European central banks have been trying to “manage” inflation expectations by possibly selling their balance due to end this September under the EGA agreement on a lean light volume market as brokers and financial market players could be in vacation.

One mitigating factor despite the recent selloff is the seasonal strength of gold going into the fourth quarter usually with August as springboard. Finally, real interest rates, the US Federal Reserve’s forward policies which could be expected to err on the side of inflation and a declining value of the US dollar will continue to cast a favorable light for higher gold prices.

Verbum sapienti satis est (A word to the wise is enough- Titus Maccius Plautus Roman comic dramatist)

No comments:

Post a Comment