``Money, again, has often been a cause of the delusion of the multitudes. Sober nations have all at once become desperate gamblers, and risked almost their existence upon the turn of a piece of paper.” Charles Mackay (1814-1889), British Poet, author of Extraordinary Popular Delusions and the Madness of Crowds

Illustrious economist Lord John Maynard Keynes once wrote, ``the markets can stay irrational longer than you can stay solvent.” When bad news is deemed as a premise to buy, and good news as an impetus to sell, isn’t that reckoned as irrational?

Just observe the world financial market’s dissonance; some segments appears to have factored in a looming temperance of the pace of global economic growth, and thus we have been witnessing a vigorous rally in global sovereign bonds as well as significant declines in prices of key commodities as oil and a majority of basic metals. As shown in Figure 1, Philippine treasuries have rallied strongly in tandem with its counterparts. This has been likewise reflected by the outstanding performance of the peso (which has been on a roll) as portfolio flows have recently supported the domestic financial markets.

Figure 1 Asianbondsonline: Philippine Treasury 2-year (green) and 10-year (red) Yields headed lower

Paradoxically, global equity benchmark indices have ascended briskly as if to discount the possible adverse effects of a prospective economic slowdown to corporate financial health. The basic presupposition is that a low inflation landscape would be conducive for higher price earnings multiples. As shown in Figure 2, the Dow Jones World Index and the Dow Jones Asian Index has so far staged a mighty comeback. If the present momentum holds, the clearing of the present obstacles (resistance levels) paves way for a retest of its recent highs!

Figure 2: Stockcharts.com: A Resurgent Dow Jones World Stock Index (red-black) and Dow Jones Asia Pacific Index (black)

But what of earnings growth? In my July 24 to 28 outlook (see Liquidity Driven Rally Amidst A US Slowdown?), I noted that the widely followed independent Canadian research outfit BCA Research expects global earnings to be revised downwards as the US growth engine cools. To extrapolate; as the earnings growth cycle peaks and most likely downshifts on a backstop of moderating pace of global economic growth, the price earnings ratio would essentially bloat. Higher prices then would exaggerate p/e ratios under this environment. But does anyone care about P/E ratios today? Or have P/E valuations been germane to present market conditions?

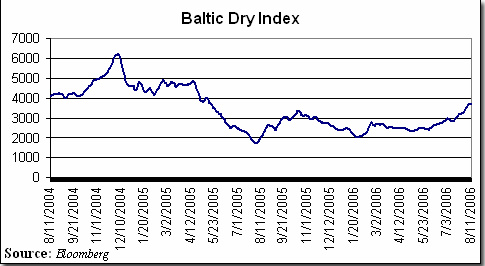

Figure 3: US Global Investors: Baltic Dry Index on a 52 week high!

Or could it be that equity markets are right, and that deceleration worries have been arrantly or even at least partially misplaced, as the bulls would have it. Can the prevailing boom conditions in the global economy cushion or offset the present headwinds from the US economy?

While most commodities have been on a decline, oddly, shipments to China have once again lathered up as shown in Figure 3. According to US Global Investors, ``The Baltic Freight index once again made another 52 week high to 3,681. Dry bulk tankers used to ship iron ore and other commodities to China are in demand and are receiving higher day-rates.”

The Baltic Dry Index is ``an assessment of the price of moving the major raw materials by sea" or to quote Daniel Gross of Slate Magazine represents `` a good leading indicator for economic growth and production. After all, it doesn't deal with container ships carrying finished goods. It deals with the precursors to production: bulk carriers carrying building materials, cement, grain, coal, and iron. Unlike stock and bond markets, the BDI "is totally devoid of speculative content," says Howard Simons, an economist and columnist at TheStreet.com. People don't book freighters unless they have cargo to move.”

Aside from seasonal factors (BDI index tends to go up during the last semester of each year), could the 52-week high BDI suggests of an upturn in commodity prices bolstered by a “surprising” turnaround in the global economic setting presently bogged down by “slowdown” expectations?

Or have global markets been anticipating more liquidity injections from the US Federal Reserve and global central banks? The recent decline in US inflation indicators as represented by Producer and Consumer Price Indices appears to have bolstered the case for a continued stance towards maintaining present interest rate levels by US authorities, and that a more pronounced retrenchment may even lead to a more accommodative monetary environment (slashing of rates).

Figure 4: Bond Market Association: Surging Credit Instruments (mortgage related securities, US treasury issuance, Money Market Instruments-Commercial Papers and Large Time Deposits and Asset Backed Securities): What tightening?

Figure 4 shows that even as Central Banks such as the US Federal Reserve go over the rigmarole of raising the cost of lending at a graduated clip, non-monetary aggregate measures of liquidity in the US have been exploding to the firmament, such as Mortgage Related Securities, Asset Backed Securities and Commercial Paper issuance. In the words of Dr. Kurt Richebächer excerpted from the Daily Reckoning, ``There never was any monetary tightness (emphasis mine). Instead, there has for years been a sharply accelerating credit expansion that has grotesquely run out of relation to economic activity. We see an economy and financial system that have pathologically become addicted to a permanent credit and debt deluge.”

Talking about addiction, the prospects of more booze for the continuity of the asset backed shindig have most likely kept short-term oriented investors in celebration. As Lord Keynes once wrote, 'Men, like dogs, are only too easily conditioned and always expect, that, when the bell rings, they will have the same experience as last time.”

Anent to surplus liquidity, the quest for higher yields and diversification into uncorrelated markets have driven hedge funds into investing or betting in...believe it or not...weather outcomes! According to the New York Times, ``Reinsurance companies, staggering from their 2005 losses, need more capital, and hedge funds, in search of high returns, have a lot of it.” Yes, excessive money and credit has led money managers and financers to tap, aside from conventional markets into the remotest geographical corner of the world, to unorthodox or seminal markets as property catastrophe reinsurance. Hedge funds and private equity capital have contributed to $7.3 billion of the $23 billion recently raised to recapitalize the reinsurance business. Talk about inflationary manifestations.

Finally, the short-term noise or the present market incongruities could also be attributed to quirks such as the expiration of options, as shown in Figure 5.

Figure 5: Mish Shedlock’s The Survival Report: Option Expiration rallies

According to WhiskeyandGunpowder’s Mish Shedlock, ``This week's rally has everything to do with inflicting maximum pain on options holders, and almost nothing to do with economic reality. For instance, one week ago, the QQQQs were flirting with a breakdown below $36, but with close to 700,000 $36 put options set to expire at the close of today, there was no way the market was going to let those options close in the money. In fact, there are over 1.2 million put options spread between strikes $35-38 for the QQQQs, all of which will expire worthless with a close above $38 this week. On the flip side, there are significant numbers of call options at strike $38 and $39, and not much at lower strikes relative to the numbers of put options. The bottom line? A QQQQ close near $38 this week will have the largest number of puts and calls expire worthless, which is a spot of maximum pain to options holders that the market often seeks to find at the end of expiration week.”

Perplexing ambiguity indeed. However, my view remains that over the interim, global Central banks will maintain their “market friendly” stance, while over the long term interest rates are bound to move higher on the continued adoption of inflationary policies and an attendant rise in inflation expectations.

No comments:

Post a Comment