``Value is not embedded in the material properties of any good or service. Neither does a thing acquire value merely because labor was employed to create it. Value is not dictated by the production process or social conditioning. An economic good is valued because an individual mind values it. It is a product of the human mind.”-Jeffrey Tucker, Fortune Cookie Economics, Editor Mises.org

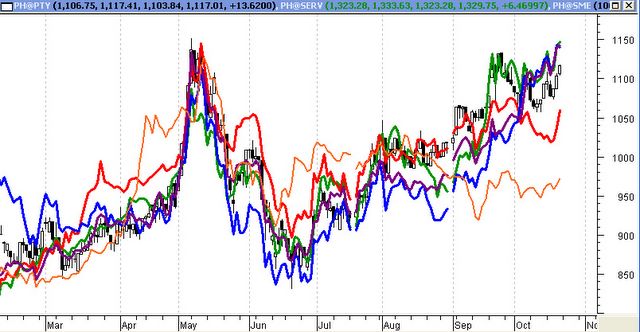

Figure 4: Rising Tide Lifts All Sectors?

Figure 4 shows, that aside from the rising general breadth of the market as the Phisix advances, sectoral indices (Property-candle; Banking- Red, Holdings-Violet, Services-Green, Commercials-Blue and the Mines and oils- Orange) have likewise been in close chime to the upside....except for the mines and oils (which outperformed earlier on the year).

The global selldown in the metals and energy prices have been used as a yardstick for “lower inflation” and has been a significant contributing factor to the weakness in the mines and oil sector of late. Aside, the outstanding gains, during the 1st semester by today’s lagging sector, have emasculated somewhat the overwhelming bullish sentiment built then. This could have possibly influenced its latest underperformance. But signs are such underperformance wouldn’t last...

Figure 5: Growth Stock Wire/Stockcharts.com: Unblemished seasonal Record for Oil stocks since 2002

Jeff Clark of Growth Stock Wire pinpoints consistent October bottoms since 2002 for the Oil stocks sector abroad as shown in Figure 5. With today’s rampaging equity markets, there is such possibility that global economies could surprise to the upside for the last quarter this year despite the much touted real estate slowdown.

It is important to note that the rotational activities in the asset sector indicate a shift in the inflationary manifestations which remains copious in the system despite the actions of the US Federal Reserve and the world central banks (remember, Rajan’s 80% non bank value added in the financial system). This could suggest for a subsequent rise in energy prices too and a corresponding rebound in metal prices, led by gold (looks consolidating as with global mines and poised for a second wind). As an aside, the pronounced cut in productions by OPEC could be a factor too (but I doubt so, considering their previous tendencies to cheat on quotas).

I also think that the eve of US elections could presage for a rebound in benchmark commodities, thereby, percolating into the domestic arena too.

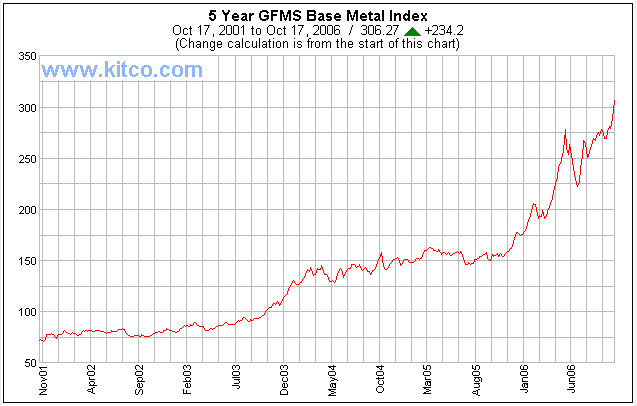

Figure 5: Kitco: GFMS Base Metal Index: What Weakness?

It’s difficult to suggest for a demand induced weakness, as I had been earlier expecting or suspecting, if as measured by commodities, we see base metals on a blistering streak, Figure 5. As you can see, inflation manifestations reveal itself in different avenues unequally.

Consequently, improving OVERALL sentiment in the local market plus a turnaround in the prices of oil/energy (hopefully) should boost prices of local mines/oil to run at par with the rest of the market possibly until the yearend, in condition that external markets remain favorable.

However, we must be reminded that there are risks out there as described earlier, mostly exogenous in nature that are real enough to heighten volatility and destabilize world markets including ours and could risk expunging present gains. We are living in very interesting times.

No comments:

Post a Comment