US trade deficit for August leapt to a record $69.9 billion. This trade deficit borne out of the global vendor financing scheme trade structure has been a very important source of worldwide liquidity, as Asia, OPEC and other Oil and/or Resource exporters continues to subsidize US consumers via recycling their foreign exchange surpluses into US assets mainly into US treasuries.

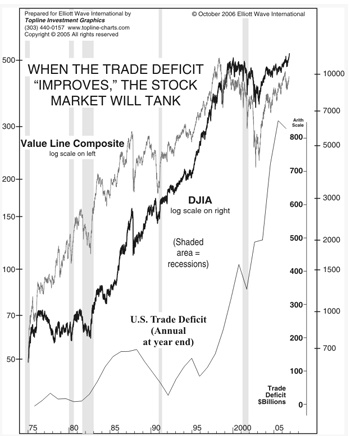

Figure 7: Elliot Wave Independent: Trade Deficit Beneficial to Markets

While we continue to decry these imbalances as unsustainable and as possible spark to a future financial or economic conflagration, US equity markets appears so far to have been funded by it (see Figure 7).

Allan Hall of Elliott Wave Independent commented, ``In fact, The Elliott Wave Theorist pointed out long ago that the trade deficit was rising with the bull market. Back in 1988, EWT used just the first half of this chart to state, “Based strictly on the chart, people should be rooting for perpetually soaring deficits!”

They predict that since liquidity has been generated by these deficits a contraction or reversal of these deficits will lead to a reversal and possibly cause the stockmarket to decline.

Now that a slowdown is clearly at works in the US economy but whose degree remains argued by the various schools of thought (the soft, hard and no landing camps), these deficits are expected to have peaked out or reached inflection point, as imports are likely to decrease while exports may continue to remain strong due to relative strengths of the ex-US global economy.

Figure 8 Gavekal Research: US Current Account Deficits and Financial Crisis

Like Alan Hall of EWT, Gavekal Research posits a similar view but on a different scale, the keen-eyed analysts says that ``a reduction in the U.S. current account deficit is equivalent to a liquidity squeeze”. And such liquidity squeeze in the past has been associated with financial crisis in some parts of the world such as Japan’s depression, Tequila Crisis, Asian Crisis and Argentina Crisis (see Figure 8).

The difference between the two camps: the Gavekal team presages a similar crisis to erupt in some other parts of the world and expects global money flow back to safe haven markets hence, remains bullish with the US dollar and US and OECD markets (low volatility due to emergence of platform companies) and expects a deflationary BOOM as an outgrowth, while, the EWT camp sees a decline in US and global equities, or deflationary BUST as a result of the unwinding of the credit bubble.

My view: the source of all these imbalances (inequality) has been anchored on the inflationary Dollar standard system. I think the ripple effect following its unwinding would be centrifugal in nature.

As noted earlier, the market consensus has been piling onto US treasuries as a one way bet on the purview that the US economy would slow significantly. Be careful on what you wish for.

No comments:

Post a Comment