Balance-sheet wealth is sustainable only when it comes from earned success, not government fiat. Wealth creation comes from strong, sustainable growth that turns a proper mix of labor, capital and know-how into productivity, productivity into labor income, income into savings, savings into capital, capital into investment, and investment into asset appreciation.- Former Federal Reserve Governor Kevin Warsh and Billionaire Investor Stanley Druckenmiller

[note my windows live writer won't work so I am doing this the traditional way]

In this issue

Phisix: Understanding the Dynamics Behind ‘Pump and Dump’

-The Pump: Everyone is a Genius

-The Difference between Promoting Bubbles and Pump and Dump

-The Central Bank Pump: “Now voting is finished”

-Pump in Motion: Ballooning Disconnect Between US Stocks and the Economy

-Japan’s Buybacks: Symptoms of a Dysfunctional Markets and Economy

-Europe’s Draghi Put Pump

-Middle East: Incipient Signs of an Erstwhile Pump to a Dump?

-SMC’s DEBT IN DEBT OUT; Symptoms of the Deformation of the Philippine Economy

Phisix: Understanding the Dynamics Behind ‘Pump and Dump’

The Pump: Everyone is a Genius

What’s the connection between celebrity magazines and stock market circles?

Well, gossip. Celebrity magazines frequently deals with coming movies or shows for certain celebrities, status of romantic relationships, scandals, fashions, paparazzi candid sensational portraits of celebrities taken from unexpected locations and more.

How about stock market circles? Most of the postings or publications from participants usually revolve around digital newspaper links on the economy or particular security issues, quotes by industry authorities or by politicians, speculations on the actions of tycoons, corporate leaders, or even leading brokers, ex-post explanations or rationalizations (mostly post hoc) of price actions, crystal ball reading from charts, and or even literature or commentaries from specialist of the industry and more. The common theme: “who is doing what” drives stock market pricing.

And since the direction of conversation has been from a populist perspective, there appear to be little tolerance on any opposing perspective.

With retail participants as the dominant constituency, stock market circles mostly serve as a channel to provide confirmation to the biases or sentiments of members which galvanizes the groupthink interactions.

What many think as searches for information has really about looking for confirmation of ones beliefs!

There is basically one way to make money in stocks in the Philippines. This is from a bullmarket. That’s why embedded incentive has been to view stock market activities as a one way trade, up up up and away.

There legally exist “short” facilities but such has been hobbled by choking regulatory requirements which renders this facility with little usefulness. This means that the “short” facility most exist only for symbolism.

So the essence for the success or survival of each platform, which depends on the number of participants, would be to sell optimism and hope; again a one sided trade.

Aside from confirmation bias, another factor which characterizes stock market circles has been social desirability bias. Aside from discussions about successful trades (very few discussion about losses), many perceive that the myriad citations of financial ratios or statistics or economic variables or sophisticated technical reading of charts in the conversational thread elevates one’s intellectual status.

[As a side note, even experts and talking heads have been frequently afflicted by these. I recently came upon a material from a domestic financial institution explaining how the domestic property sector will continue to flourish. They do this by overwhelming the reader with a deluge of statistics (or economic history) which they simplistically project into the future. This will convince the economically uninformed reader and provide a confirmation of popular opinion to those looking for one. But there is one critical and fundamental flaw: the absence of identifying where demand will come from, except to assume that this exists. This also means that since demand has been unknown, then automatically this precludes the explanation of how continuing increases in property prices which has been funded by credit can be discerned as salutary and sustainable.]

Bullmarkets reinforces groupthink. This is because markets go up even for the wrong attributed reasons applied by participants. Being proven right cements one’s belief regardless of the cogency of methodology used. This represents the bull market’s “everyone is a genius” dynamic.

I had my share of this kind of experience during the bullmarket days of the mid-1990s. Unfortunately the outcome proved to be excruciating: financial losses PLUS traumatic mental anguish. That’s why I renounced the stock market then. Well that was until my mentor convinced me back. And this is the reason for my conservative approach in dealing with the tradeoff between risk and rewards in stock market investing. And this is why I help spread my experience by writing about it, even if it means going against the consensus.

Yet since groupthink reduces personal accountability and responsibility, most retail participants are easily swayed by sheer peer pressure. So even in bullmarkets some fall into sharp price volatility traps which some attribute to so called immoral “pump and dump” operations.

The Difference between Promoting Bubbles and Pump and Dump

If dishonest money begets dishonest accounting, it also begets dishonesty and corruption in every aspect of life – from the boardrooms of the big bankers down to the lowest economic agent. – Dylan Grice, Edelweiss Journal

I find accusations of “pump and dump” a curiosity in moral and in economic context.

First “Pump and dump” as defined by Investopedia.com[1] (bold mine): A scheme that attempts to boost the price of a stock through recommendations based on false, misleading or greatly exaggerated statements. The perpetrators of this scheme, who already have an established position in the company's stock, sell their positions after the hype has led to a higher share price.

Phisix member issues presently carries valuations of PERs of 30, 40, 50, 60 that are already above pre-Asian crisis highs as well as PBVs at 4,5,6,7,8. These are facts. And these have not been about small “growth” stocks, but of blue chips or the biggest market caps firms whom have been dominant in their respective industries.

Given their size or heft, the rate of “growth” from these firms will have natural limits due to a number of factors such as competition, the law of compounding, size relative to the overall economy, inflation and more as previously discussed[2].

In short, the rate of growth of the biggest market caps will mostly reflect on the growth rate the of economy overtime, where any outgrowth will be subject to mean reversions.

The recent decline of 1Q 2014 statistical GDP growth to 5.7% underscores a statistical force called the mean reversion dynamic[3] even applied to economic growth rates

So when has these “rich” levels of valuations premised on unsustainable growth rates been considered normal? Also what are the risks accompanying such extreme levels of valuations? Or has risks been entirely eliminated?

Are these valuations not based on false, misleading or even great exaggerations?

Apparently for the mainstream these concerns fall into a sound of silence.

Yet common sense tells us that if the rate of nominal stock market returns grows MORE than earnings growth, then stock market activities will account for multiple expansions than about healthy returns.

Say for instance, publicly listed company X grows at a rate of 10% annually, but stock prices expands by 30% over the same period. The table above reveals that ceteris paribus or assuming the constancy of these numbers, the annualized Price Earnings Ratio PER growth of 18.2% will mean that by year or period 4 Company X’s PER will almost double to 19.51 from the original 10! This comes in the light of a 185% return in the stock prices as against only 46.4% increase in eps!

Do you see now the dynamics behind these outrageous stock market valuation levels? Or do you see how—PERs of 30, 40, 50, 60 that are above pre-Asian crisis highs and PBVs at 4,5,6,7,8—have been arrived at, where stock market returns has discernibly outpaced earnings growth?

Has the essence of earnings multiple expansions been about earnings growth? Obviously the answer is a BIG NO!

What this exhibits instead has been that “growth” has been used as pretext (or a rally cry) to justify wanton and reckless speculations based on popular fantasies.

Negative real rates have made conditions conducive for the susceptible public to believe that PERs of 30, 40, 50, 60—that are already above pre-Asian crisis highs—will even be HIGHER!!!

This is a clear demonstration that for the mainstream, valuations and risks do NOT really matter at all. This one way trade mentality which represents the consensus thinking has been promoted by media, their favorite bubble ‘expert’ apologists, and interest groups who benefits from the BSP’s inflationism that has been naively ingested by the gullible public.

This has been part of the orchestrated publicity campaign to promote a political agenda, i.e. easy access to cheap credit[4].

And evidently too the 30-60 PERs reveals of the stunning degree of accrued distortions from the widening chasm between nominal earnings growth vis-à-vis stock prices returns for such incredulous levels to be achieved.

NO bubble huh?

Yet what drives a general overvaluation of asset prices?

Under a fixed money supply, price increases in one area would result to price reductions in other areas. So while some individuals may influence prices of one or two assets or commodities, they can’t influence prices overall. And given the limits of resources, any manipulation will tend to be short term.

But what we are seeing today has been a generalized mispricing of both financial assets and economic goods. So who is responsible for the spreading of price increases from asset prices (stocks, bonds, properties) to the real economy[5]?

The key proponent of inflationism J. M Keynes gives us a clue[6]: “Lenin is said to have declared that the best way to destroy the capitalist system was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some.” (bold added)

By the above substance: Is debauching the currency—in order “to confiscate, secretly and unobserved, an important part of the wealth of their citizens” by blowing bubbles that ultimately destroys the capitalist system—the work of the sinner or the saint? IS the promotion of bubbles (money from thin air credit expansion) which is a form of “debauching the currency” the work of the sinner or the saint?

Who are the “enriched some” who benefits from the bank credit expansion of debauching of the currency as seen by the massive 30+% growth in money supply[7] at the costs of impoverishing the many?

Has these inflationist actions not generated a “pump” (false, misleading or great exaggerations) in asset markets where the next actions will be a “dump”?

How do you call vested interest groups, politicians and bureaucrats who promote “buy” of severely overpriced securities that has concealed huge risks…sinners or saints?

Have these rampant credit expansion not signified as the invisible redistribution process via the transfer of risks and resources (or the secret and unseen confiscation of resources) from the vulnerable public to these interest groups or the enrichment of some? Yet are these activities not the principal agent problem (conflict of interest) or seemingly professional misconduct?

What ethically differentiates between promoting bubbles and a “pump and dump” operation?

Yet has the public been aware that these two are connected? If the cost of unscrupulous behavior have been substantially lowered (which means such actions have even been rewarded), then the natural consequence would be to see these activities multiply.

Said differently, if monetary policies have been promoting widespread gambling in the marketplace as manifested by grotesque mispricing via valuations excesses and by the sharp jump in churning activities that has spread to the second and third tier issues, as exhibited by near record trade churning (no of trades, left) covering a record broad market activities (traded issues, right) despite the Phisix still below May 2013 highs at 7,400 (green rectangles), then why won’t specific “pump and dumps operations” become more frequent or even a norm?

Even real world Ponzi schemes thrive or flourish in such an environment[8].

One major nefarious repercussion from the stealth policies that facilitate the plunder of the clueless public through money manipulation or debasement has been immoral behavior.

As the great journalist Henry Hazlitt warned in his book What You Should Know About Inflation[9], (bold mine)

Inflation makes it possible for some people to get rich by speculation and windfall instead of by hard work. It rewards gambling and penalizes thrift. It conceals and encourages waste and inefficiency in production. It finally tends to demoralize the whole community. It promotes speculation, gambling, squandering, luxury, envy, resentment, discontent, corruption, crime and increasing drift toward more intervention which may end in dictatorship.

Then why merely look only at the symptom (pump and dump) but not the disease (inflationism)? Why mistake forest for trees?

The Central Bank Pump: “Now voting is finished”

This observation from Sir Michael Hintze, founder of CQS, one of Europe’s largest hedge funds as quoted by the Financial Times[10] resonates on the state of the current financial markets: (bold mine)

The problem is that we’re not there [in a low volatility environment] because markets have decided this, but because central banks have told us . . . There is no room for dissenting voices. My fear is that when everyone is in the same place is when a change in sentiment causes the maximum disruption.” Sir Michael adds: “The beauty of capital markets is that they are voting systems, people vote every day with their wallets. Now voting is finished. We’re being told what to do by central bankers – and you lose money if you don’t follow their lead.”

This striking remark reveals several provoking insights.

One, this has been a candid admission of the intense pressure in the operating environment of money managers. [Yes this includes me].

Two, while cognizant of the risks, this hedge fund admits to reluctantly having to chase on yields because they have been “forced” by central bank policies: “Now voting is finished”.

Three, because of the unbalanced nature of risk-reward provided by the current environment, investor money placement with hedge funds have been faced with unnecessary risks. Money managers have to either front run the central banks or just crowd into central bank administered trades. Staying on the sidelines will not benefit fee based money managers. So money managers have been taking more risks than required.

Fourth, this statement “central banks have told us . . . There is no room for dissenting voices” means that market prices have been set—not by normal market forces—but by politics. In short, there hardly has been a natural or market based “price discovery” because market signals have been severely distorted.

This is very important because this also shows that aside from financial markets, a vast segment of economic activities have also been influenced or affected by the monetary policy induced manipulation of price signals. This means that economic conditions operating under the current policy setting will be vastly different than one from conditions where either market forces or economic reality pushes back on central bank (and government) actions or when the same authorities reverses on the current policy dynamics.

This applies whether in the US or the Philippines. For the latter, the runaway property inflation[11] has been emblematic of the real economic dislocations which has buttressed and abetted the severe distortions in the financial asset valuations. As one would note, everything is interconnected; one sector’s action is another sector’s reaction and vice versa. It would be foolhardy to view the world in isolation.

This also implies that in the context of ‘specifics’ or defined opportunities, trend watchers should be aware of this conditionality. This is because given the grave distortions in the pricing system; chances of economic and financial miscalculation may be substantial. And miscalculation translates to losses.

To simplistically assume that tomorrow’s conditions will be the same as today can be analogized as walking on a minefield.

To repeat, economic or business conditions today may be immensely different tomorrow.

Remember price signals communicate and guides economic coordination. To ignore the indispensable role of price signals is to be confused of how economic reality works under a market economy. Distortions in pricing signals are indicative of ephemeral unsustainable conditions.

Fifth, this has also been a disturbing revelation of the fragility of financial market conditions. The hedge fund manager knows that due to the vast contortion of prices, markets are confronted with a substantial risk of “maximum disruption”. They recognize that the “Don’t fight the Fed” trade has its limits.

Rising inflation rates and unwieldy growth in debt are just examples of the natural barriers to any inflationary boom.

Wall Streets of the world has been ramping up on very risky forms of debt that have been diverted into risk assets. (charts above are from the Institute of International Finances). These serve as epicenters to risks of ‘maximum disruption’.

Lastly this represents further signs of central bank “pump” which implies that financial markets has been disfigured into a grand casino.

Pump in Motion: Ballooning Disconnect Between US Stocks and the Economy

The recent events showing the vast divergence between the US statistical economy and the US stock markets, which has been drifting at record levels, are examples of the evolving maladjustments derived from policy interventions.

1Q 2014 statistical growth has been revised TWICE originally from .1% to -1% last week came to print with a huge -2.96% decline. So this has not only been an issue of an unseen event by the mainstream, importantly the contraction has been readjusted to post bigger losses, yet stocks remain streaking skyward. Also 2.96 isn’t just a number, it represents the 17th largest decline in US history.

Why the seeming disconnect?

The ongoing mania in the US stock markets has not only been fueled by retail investors piling into markets financed by margin debt, but importantly also debt financed buybacks and dividend issuance.

Buyback is a form accounting (financial) engineering. Buybacks amplify earnings by reducing the number of shares in the denominator of the Earnings Per Share (EPS) ratio. So even if earnings growth has been unimpressive, buybacks would provide the cosmetic embellishment; the lipstick on the pig. Thus buybacks provide the juice for higher stock market prices.

As I pointed out here[12], during the 1Q, NINETY THREE 93% of companies from the S&P spent their earnings on buybacks and dividends.

Companies have hardly been redeploying earnings to expand productive undertakings, so the continuing lackluster growth. Instead companies have been borrowing to massage their EPS, via accounting magic, so as probably to bloat stock options[13] and management bonuses aside from seducing retail participants into a frenetic buying spree.

This means that aside from the mainstream alibi of weather related slowdown on 1Q GDP, this exposes on why the US economy has been languishing. Recovery in Private Non-residential fixed investments/GDP from the troughs of the 2008 lows remains halfway mark from the 2007 highs.

The diversion of funds from capital expenditures into financial engineering and rank speculation has brought about this parallel universe or divergence between real economic activity and financial markets.

Even former US Federal Reserve governor Kevin Warsh and billionaire hedge fund investor Stanley Druckenmiller in a recent OpEd at the Wall Street Journal[14] notices the same predicament: (bold added)

Higher asset prices are not translating into meaningful increases in capital expenditures, and the weak growth in business investment is proving to be an opportunity-killer for workers. Those with jobs have some job security. But they are less willing to run the risk of finding a better opportunity, or negotiating for higher wages.

Those without jobs, especially in the younger cohorts without a post-high school education, do not attach to the workforce, thus never gaining the entry-level skills and discipline to build a career. The malaise in the labor markets—and muted business investment—help explain why productivity measures are a full percentage point below historical norms.

Financial markets or particularly stock markets have essentially become propaganda loudspeakers or misinformation dissemination machine for policymakers to convey to the public, probably as part of their indoctrination campaign, to paint their desired picture of economic conditions. By massaging stock market markets, they attempt to impress upon the public that rising “stock markets equal economic growth”.

Unfortunately, the problem is that the real economy hasn’t been collaborative or cooperative.

Yet how sustainable has this policy induced “Now voting is finished” Fed-sponsored trade?

The mainstream, whom didn’t see the significant 1Q contraction coming, dismisses the 1Q figures as weather related anomaly. The question is what if this hasn’t been an aberration? What if economic growth data in the 2Q sustains a decline? This would technically represent a recession.

Following the sharp slump, if the past were to rhyme then the odds doesn’t favor a recovery. Notes David Stockman a former US politician, presently a businessman and publisher of the Contra Corner[15]: There have been 265 quarterly GDP prints since 1947; only 18 of these posted a number below the -2.9% recorded for Q1; and in only one of these 18 deeply down quarters was the US economy not in recession.

I am not keen on pattern searching even if it is based on statistics. Yet the most probable explanation for the 17/18 or 94.4% odds for a continuation of an economic contraction has likely been momentum. Big declines tend to have carryover effects.

So while it may be true that there may some weather related shocks that may have influenced the 1Q downturn, the intensity (-2.96%) of decline suggest that this has been more than just climate based aberrations.

Yet despite rapid denials by Keynesian Kool Aid drinkers, Mr. Stockman adds that current economic figures hardly have been materially supportive of a recovery citing lackluster PCE growth, housing starts below Q1, tepid Q-on-Q exports growth or even hardly any sizeable pick up in government sector consumption and investment.

So how would record overvalued US stocks and other financial markets react to a possibility of recession? How will the cumulative liabilities acquired to pump up record stocks based on buybacks be paid when earnings are likely to decline too? Will the FED reverse their “tapering”? And more than this, US financial markets are at record low volatility while stock markets, like the Philippines, has completely departed from fundamentals or in a parallel universe, thus the multiple expansion.

And based on corporate announcements[16], buybacks appear to be poised for a decline in the 2Q 2014. Yet if buybacks have indeed been “played a prominent role in the market's record-breaking rally” according to Wall Street Journal’s Money Beat[17], then the consensus could be in for a nasty surprise.

Japan’s Buybacks: Symptoms of a Dysfunctional Markets and Economy

Buybacks hasn’t just an issue of the US.

Prior to this week’s slump, Japanese stocks have been furiously rallying backed by a rising tide that has lifted many boats mainly on buybacks. A Bloomberg article describes the surge in buybacks by Japanese firms as the “fastest rate ever”, founded on “the combination of record cash, cheap shares and a government-led drive to buoy return on equity”[18].

This PM Shinzo Abe led drive to “buoy return on equity” has also been prompting the yield starved markets to “front run” on the equity markets in heavy expectations that Japan’s US$1.3 trillion Government Pension Investment Fund (GPIF)[19] would drastically modify asset allocation that would favor equity markets. Since last year, Japan’s PM has been pressing the world’s biggest pension fund to buy stocks.

What has been fundamentally and terribly wrong with all these?

If stock markets are supposed to represent discounted stream of future cash flows in favor of investors, then all these finagling of earnings have only been obfuscating real fundamentals. Simply stated, stocks haven’t been valued based on real fundamentals but by financial engineering. So aside from the failure of price discovery, this reveals of a fundamental breakdown of the pricing system—again which has become a tool for political agenda. This means that even if stocks do go up, they have unsoundly been pillared from political interventions.

As a side note: What will GPIF’s contribution to the stock market mean? Nothing fundamental but a temporary boost from a reshuffling of assets. But coming at what cost? At the hands of the average Japanese pensioners. Yet the GPIF seems to have signaled a pushback: “Investment reform will take place exclusively for the benefit of those covered by the pension system”[20]. Yet temporary boom can also mean a bust.

What has going on in Japan’s stock markets have only been symptoms of a bigger picture: the same Abenomics engineered economy. It’s a wonder how the Japanese economy can function normally when the government destabilizes money and consequently the pricing system, and equally undermines the economic calculation or the business climate with massive interventions such as 60% increase in sales tax from 5-8% (yes the government plans to double this by the end of the year to 10%[21]), and never ending fiscal stimulus which again will extrapolate to higher taxes.

The mainstream has all been desperately scrambling to look for “green shoots” via statistics. They fail to realize that by obstructing the business and household outlook via manifold and widespread price manipulations, this will only lead to not to real growth but to greater uncertainty which translates to high volatility and bigger risks for a Black Swan event.

Yet no amount of pumped up statistics will displace the importance of record cash ¥232 trillion, or about $2.3 trillion being held by Japanese companies[22]. This shows that despite rising stocks Japanese firms view the current environment with even high uncertainty, and some has instead resorted to buybacks.

So what does the policy “buoy return on equity” mean? It means benefiting a small number of equity holders coming at the expense of the resident Yen holders.

Soaring inflation has increased Japan’s Misery Index which has reportedly hit the aging population hard: “The price of everything we eat on a daily basis is going up,” Tatsunami, 70, a retired kimono dresser, said while shopping in Tokyo’s Sugamo area. “I’m making do by halving the amount of meat I serve and adding more vegetables.” Tatsunami’s concerns stem from the price of food soaring at the fastest pace in 23 years after April’s sales-tax increase. Rising prices helped push the nation’s misery index to the highest level since 1981, while wages adjusted for inflation fell the most in more than four years[24].

So Japanese senior citizens will not only be faced with falling purchasing power, but also a risk of the loss of pension if the GPIF abides by PM Abe’s urgings.

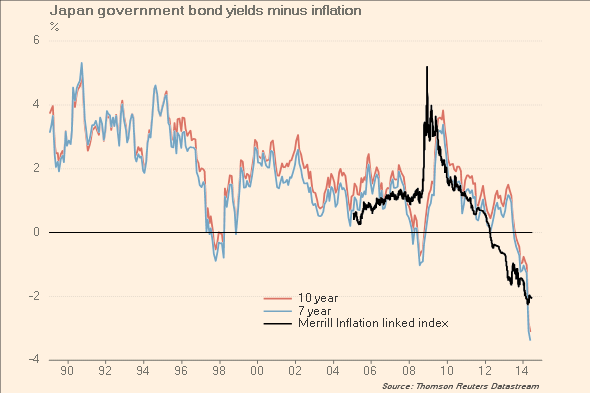

Oh, all these massaging of the markets have led to an astounding divergence. Yields of Japanese Government Bonds (JGB) continue to sink as price inflation spiked. This comes as the BoJ has practically vanquished liquidity in the JGB markets[25]. In other words the BoJ manipulates the JGB markets in order to keep interest low to sustain the humongous debt levels and by banishing the ‘shorts’ (or the windowmaker trade). This simultaneously builds on financial instability as JGBs, which are supposedly risk free assets and core holdings of financial institutions, becomes illiquid and inaccessible.

Promoting bubbles is an activity of a sinner or saint?

Europe’s Draghi Put Pump

A short note on Europe’s stock markets.

This is a fantastic example of the central bank “Now voting is finished” trade or a seeming falsification of the earnings drive stocks trade.

Forward earnings of Europe iShares EMU MSCI has not only been in a steady decline since 2011, but estimates by the mainstream have been repeatedly been downscaled as shown by those red lines in the left window chart from Yardeni.com.

Ironically despite both downscaling of earnings estimates and forward earnings, since ECB’s Mario Draghi’s “Do Whatver it Takes to save the Euro” in July 2012, the iShares EMU MSCI ETF bottomed, kept climbing, recently set a 7 year high and fast approaches the 2007 highs. (right window from iShares)

You can now throw out all what you know about textbook stockmarket investing.

How have these been financed? I’ll quote the Financial Times (bold mine)[26]: European companies that raise finance are taking on levels of debt not seen since the financial crisis as they adjust to the prospect of low interest rates for the foreseeable future. The ratio of debt to company earnings, or “leverage multiples”, for all European transactions were 5.1 times earnings in the first quarter of 2014, above the 10-year average (4.8 times) for the first time since 2008.

Again the question: how sustainable is a debt financed equity multiple expansion?

Middle East: Incipient Signs of an Erstwhile Pump to a Dump?

Finally speaking of boom bust cycles, high flying frontier markets appear to be signaling another round of destabilization.

United Arab Emirates’ stock market index as measured by the Dubai Financial Market (DFM) has suffered a quasi crash last week. The DFM index was down 8% on the week ending June 27th this adds up to a bear market where UAE’s index has endured a 21.8% loss as of Friday (chart from Arab Stock Market Analysis). Ironically the DFI remains 21.3% UP year to date. This means the quasi-crash only erased about half of the early gains.

Stated reason for this week’s decline as per Bloomberg[27]: 1) “The U.A.E.’s central bank said June 8 there are signs the property market is overheating” 2) rumors of “top-level dismissals at Arabtec Holding Co. (ARTC), the United Arab Emirates’ largest-listed builder” and 3) margin calls or losses “amid speculation leveraged traders liquidated positions”

Hmmmm. Blueprint for overheating bubble economies?

I would add to this to possibility of growing concerns over the region’s stability and or even possibly, fund raising activities for political purposes (opposing parties in Iraq-Syria crisis)[28].

All it takes is for a trigger (related or not) to unleash forces that exposes on artificial boom conditions.

SMC’s DEBT IN DEBT OUT; Symptoms of the Deformation of the Philippine Economy

Of course central bank puts or “pumps” impact corporate operations even in the Philippine setting. This will mark a follow-up commentary from last week’s truncated discourse on SMC[29].

Technically speaking, or based on accounting, SMC has indeed been profitable. This is what has been projected; therefore this is what has been publicly seen.

BUT what has not been seen is that SMC’s business model has been MORE than just about accounting entries. This marks a difference between substance and form.

The PRINCIPAL reason SMC has been technically profitable has been because of the debt carry subsidies provided by the BSP (as well as the US Federal Reserve) through zero bound rates or negative real rates. SMC has significant exposure on foreign debt too.

Without the central bank’s invisible subsidies, San Miguel’s DEBT IN DEBT OUT model would NOT have reached current levels as interest rates would have been significantly higher. This also means that under ‘normal’ circumstances, SMC’s current operations will hardly cope up with the cost of servicing debt or be able to indulge in extensive expansions financed by gearing.

What I also have tried to previously show is that SMC’s business model of asset trading financed by debt has produced growth rates of debt far GREATER than profits.

When debt grows significantly faster than profits, eventually the company will suffer from a debt overload. This shows why SMC’s model looks very much like a Hyman Minsky’s Ponzi financing dynamics. That's also why I pointed out that SMC’s net profits in 2013, outside the Meralco sale, or recurring pre-tax profits in 2013, have been substantially lower relative to 2012 (-48%) and 2011 (-36.7%) even as debt grew by 20% last year!

Yet 2013 hasn't been an anomaly for SMC’s deepening reliance on debt. Instead this has been an ongoing trend since 2009 when the company overhauled her business model[30] which curiously and coincidentally came along with the BSP’s monumental aggregate demand based policy shift[31]. No conspiracy theory here.

Ponzi financing is really about the inadequacy by an entity to service existing liabilities out of the regular or conventional business operations. It is a symptom of an ongoing deterioration in the existing business model as expressed through corporate financing. So companies operating under these circumstances use increasing degree of leverage complimented by arbitraging of assets to make up for the shortcomings in the financing of business operations. This represents THE substance.

However, without a real improvement in business conditions, Ponzi financing only buys time (from a black swan event or an implosion) that builds upon the entity’s operational fragility.

A truly profitable company would use debt as a compliment to operations rather than to become heavily, if not entirely, dependent on it. Thus when SMC incurs sustained substantial increases in her debt stocks, which mainly springs from DEBT IN and DEBT OUT rollover financing operations, that has reached a stunning Php 1 trillion annualized in 2013, then these are manifestations that whatever profits that have been generated have been merely accounting profits. The latter is the form.

Said differently, entities that suffer from consistent deficiency in internal cash generation would lead to a deepening dependency on debt financing. This has been the case of SMC. Yet such are hardly signs of real profitability or salutary financial conditions. Instead, artificially derived accounting profits would function more like accounting artifice induced embellishment.

In addition, there is also the quality of the revenue side to consider which becomes basis for a company’s cash flows. In the case of SMC, much of the revenues of its subsidiaries Petron, PAL, SMB, Packaging, Infrastructure and Energy, have likewise been anchored from today’s BSP’s interest rate subsidies.

This means that when the money environment ‘normalizes’, possibly either in response to global monetary political economic trends or domestic market conditions and or from domestic policy actions, a slowdown in global growth or in the domestic economy will bring to fore SMC’s most vulnerable spots, particularly from the business side via slowing sales (demand) combined with the expenditure side via the intractable levels of debt stock, the asset side via the corrosion of asset valuation and the liability side via the amplification of risks predicated on heavy gearing.

Also SMC’s asset trading profits has been dependent on sustained asset price increases.

Via negative real rates, the BSP has been providing price arbitrage opportunities to big companies with access to credit in the formal banking and finance sector from which SMC has capitalized considerably.

Negative real rates environment has provided financial leverage to SMC to acquire assets for price arbitraging with extremely low debt carry service costs. As previously noted, SMC’s cost of debt at Php 30.97 billion in 2013 grew by a measly 3.9% from 2012’s Php 29.8 billion even as debt ballooned by 20% or Php 75.2 billion.

SMC’s Meralco trade serves as a splendid example of the BSP’s silver platter or gift via a leveraged or debt financed “buy high, sell high”. In short, the BSP rewarded accounting profits to SMC, albeit indirectly. These are profits (or even trade opportunities) that may NOT have been realized and or even existed under “normal” monetary conditions.

Such accounting profits could be reckoned as unendurable primarily because these are politically subsidized. Said differently, in order to maintain the firm’s operational viability, SMC have become heavily reliant on unsustainable political support from the continued tweaking of the economic environment through the BSP’s aggregated demand management policies

SMC’s debt conditions alone reveal of their sensitivity to variable risks in particular interest rate, inflation, currency and credit. Yet recent increases in consumer price inflation in the backdrop of a ballooning debt will amplify on these risks.

At the end of the day, SMC’s incumbent business model deeply depends on TWO factors 1) a NON-inflationary environment from central bank subsidy of Financial Repression via NEGATIVE real rates (ZIRP) that supports sustained asset price increases or the Keynesian utopia of ‘quasi permanent boom’ and or 2) continued open access to cheap debt financing.

The problem is that the first seems in the process of a reversal. The second or cheap debt financing seems about to hit a natural speed limit.

Yet SMC’s predicament should hardly be seen in the context of only specific risk (standalone or isolated) or common factor risk (subgroups, e.g. industry specific) but one of systematic risk (market risk or financial stability risk).

Bottom line: SMC’s financial frangibility represents a symptom of the evolving deformation of the Philippine financial and economic system, specifically in the formal economy.

And like in politics, accounting identities can be made to function in a spectrum of smoke and mirrors.

.png)

.png)

.png)

.png)

.png)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}