For domestic Earth Hour fans, your dreams just came true: Earth hour is for now a reality -via rotational brownouts in Metro Manila!

2-3 hour brownouts plagued the Philippine metropolis over the week.

Of course the news has cited many "seen" factors, such as high energy costs, "extremely high prices at the wholesale electricity spot market", the weather "With El Niño still around, hydropower facilities in Luzon were likewise not performing to capacity", and the dearth of operating capacity, "Data from NGCP, the agency tasked with transporting power from generation plants to power distributors, showed that several generation facilities were either still out of commission or producing way below capacity."

Others blame it on monopoly distributor Meralco, one analyst argues that powers generators should be held responsible.

Anything else but the government.

Earlier, some conspiracy theorists associated brownouts with surreptitious plans to "sabotage" the elections in order to declare a 'failure', thereby extend the rule of the incumbent.

YET what is not reported or the "unseen" is that the Philippine energy sector is one of the tightest regulated (and most politicized) industry, which means hardly any activities are outside the ambit of regulatory scrutiny or "oversight".

Can Meralco raise rates without the approval of ERC (Energy Regulatory Commission)? Can power plants be constructed liberally without the Department of Energy's approval? The obvious answers to these questions: No.

Yet for all the power and authority vested in the presumed "expertise" of regulators, this has to happen.

What I am saying is that in contrast to all other factors cited by talking heads and the media, brownouts are simply representative of regulatory or government failure.

Proof?

Take subsidies.

The Philippine energy sector has operated on various subsidies from which the ERC has reportedly recently waived except for lifeline subsidies for the "poor".

Yet politics is always seen as operating outside the realm of economics.

Economic 101 tells us that low prices will spur greater demand. And rising demand will create pressures on supply. In free markets, these imbalances will be vented through market price signals, from where adjustments in supply will be made in order to meet demand.

But energy prices here are not determined by market prices but by prices set by the government, particularly by the ERB (via PBR for Meralco) [see earlier discussion Bubble Thoughts Over Meralco’s Bubble].

This indicates that energy prices reflects on the bureaucratic assessments, which not only deals with the market (we don't know how they define the market), its compromises with energy producers, but for its political needs too.

Moreover, subsidies made to the "poor" or the unproductive sectors create additional demand (due to subsidized prices) which are paid for by the productive sectors.

Hence, the productive sectors are paying for higher cost of energy, from which adds to the cost of doing business, which thereby reduces the rates of domestic investment.

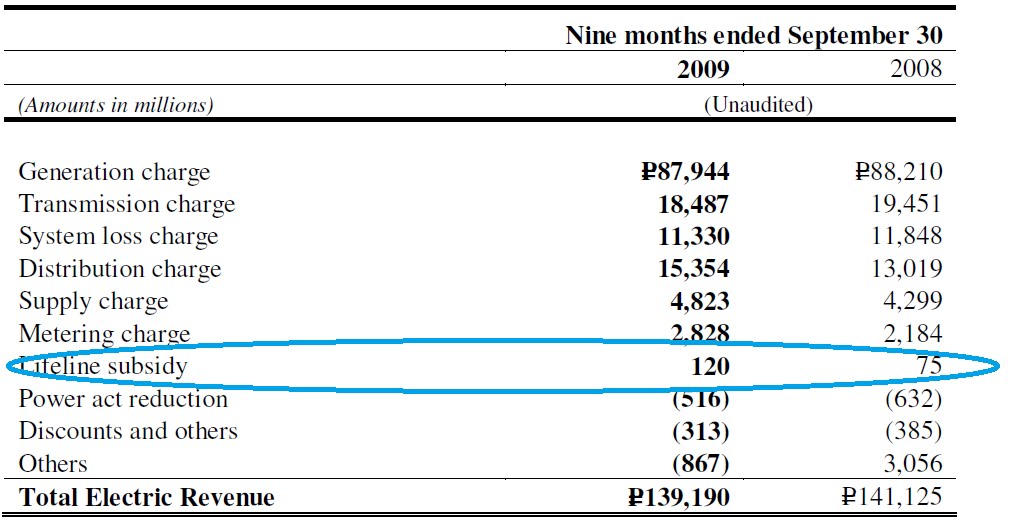

Here is Meralco's 3rd quarter financial statement.

Here is Meralco's 3rd quarter financial statement.

The table simply shows that the income from lifeline subsidies jumped by a hefty 60% through September 2009 relative to the same period in 2008.

This is simply the laws of economics at work.

This also implies that the productive sector (investors, entrepreneurs and working class) along with the rest of society is suffering from the brownouts based on the policy to subsidize energy rates on the poor.

It's essentially a manifold blackeye for the productive sectors:

-paying for a higher cost to subsidize the poor (where the latter takes advantage of) or deadweight loss,

-production and work disruption from energy outages,

-lesser income from diminished output

-reduced economic growth from high cost of doing business and work disruptions and

-personal inconvenience!

And there's the rub. Good intentions are blighted by economic reality.

And guess what? We seem to be seeing more of a rerun of 1994. The next President is likely to preside or oversee a deluge of investments that would cater to present shortages.

And these would seem as the ripe opportunities for the Return of Investments (ROI) for the political class that rightly invested on this elections.

And this is why we have predicted there will be little material change with a new government.

It's all about human nature, in terms public choice theory.

Finally there are other factors to deal with, local regulation, environment and most importantly taxes (VAT and royalty). But we will deal with these later.

2-3 hour brownouts plagued the Philippine metropolis over the week.

Of course the news has cited many "seen" factors, such as high energy costs, "extremely high prices at the wholesale electricity spot market", the weather "With El Niño still around, hydropower facilities in Luzon were likewise not performing to capacity", and the dearth of operating capacity, "Data from NGCP, the agency tasked with transporting power from generation plants to power distributors, showed that several generation facilities were either still out of commission or producing way below capacity."

Others blame it on monopoly distributor Meralco, one analyst argues that powers generators should be held responsible.

Anything else but the government.

Earlier, some conspiracy theorists associated brownouts with surreptitious plans to "sabotage" the elections in order to declare a 'failure', thereby extend the rule of the incumbent.

YET what is not reported or the "unseen" is that the Philippine energy sector is one of the tightest regulated (and most politicized) industry, which means hardly any activities are outside the ambit of regulatory scrutiny or "oversight".

Can Meralco raise rates without the approval of ERC (Energy Regulatory Commission)? Can power plants be constructed liberally without the Department of Energy's approval? The obvious answers to these questions: No.

Yet for all the power and authority vested in the presumed "expertise" of regulators, this has to happen.

What I am saying is that in contrast to all other factors cited by talking heads and the media, brownouts are simply representative of regulatory or government failure.

Proof?

Take subsidies.

The Philippine energy sector has operated on various subsidies from which the ERC has reportedly recently waived except for lifeline subsidies for the "poor".

Yet politics is always seen as operating outside the realm of economics.

Economic 101 tells us that low prices will spur greater demand. And rising demand will create pressures on supply. In free markets, these imbalances will be vented through market price signals, from where adjustments in supply will be made in order to meet demand.

But energy prices here are not determined by market prices but by prices set by the government, particularly by the ERB (via PBR for Meralco) [see earlier discussion Bubble Thoughts Over Meralco’s Bubble].

This indicates that energy prices reflects on the bureaucratic assessments, which not only deals with the market (we don't know how they define the market), its compromises with energy producers, but for its political needs too.

Moreover, subsidies made to the "poor" or the unproductive sectors create additional demand (due to subsidized prices) which are paid for by the productive sectors.

Hence, the productive sectors are paying for higher cost of energy, from which adds to the cost of doing business, which thereby reduces the rates of domestic investment.

Here is Meralco's 3rd quarter financial statement.

Here is Meralco's 3rd quarter financial statement.The table simply shows that the income from lifeline subsidies jumped by a hefty 60% through September 2009 relative to the same period in 2008.

This is simply the laws of economics at work.

This also implies that the productive sector (investors, entrepreneurs and working class) along with the rest of society is suffering from the brownouts based on the policy to subsidize energy rates on the poor.

It's essentially a manifold blackeye for the productive sectors:

-paying for a higher cost to subsidize the poor (where the latter takes advantage of) or deadweight loss,

-production and work disruption from energy outages,

-lesser income from diminished output

-reduced economic growth from high cost of doing business and work disruptions and

-personal inconvenience!

And there's the rub. Good intentions are blighted by economic reality.

And guess what? We seem to be seeing more of a rerun of 1994. The next President is likely to preside or oversee a deluge of investments that would cater to present shortages.

And these would seem as the ripe opportunities for the Return of Investments (ROI) for the political class that rightly invested on this elections.

And this is why we have predicted there will be little material change with a new government.

It's all about human nature, in terms public choice theory.

Finally there are other factors to deal with, local regulation, environment and most importantly taxes (VAT and royalty). But we will deal with these later.