``But the boom cannot continue indefinitely. There are two alternatives. Either the banks continue the credit expansion without restriction and thus cause constantly mounting price increases and an ever-growing orgy of speculation, which, as in all other cases of unlimited inflation, ends in a ‘crack-up boom’ and in a collapse of the money and credit system. Or the banks stop before this point is reached, voluntarily renounce further credit expansion and thus bring about the crisis." Ludwig von Mises in Interventionism: An Economic Analysis (p. 40)

Recently a link from last year’s TV interview of an eminent Cassandra, Mr. Gerald Celente, was posted at a social community network. Mr. Celente prophesized, not only of the “greatest” depression for the US, but of an environment marked by “revolution, food riots and tax rebellions”. Such development would bring about America’s “ceasing to be a developed nation” or essentially would translate to the country’s defacement as the world’s premier economic and financial power by 2012.

The accompanying the link had a note from the link author who questioned about how such an interview was “allowed” to be aired and what was this “doomsday” scenario all about.

We have long known about such extreme views (which should include James Kunstler-another Cassandra who believes of the real risks of a world at war arising from the unsustainable energy infrastructure from which the world currently operates and survives on), but has refrained from discussing it because of our “optimistic” predilections. Nonetheless, on the account of the “ripeness” of the occasion, this article will attempt to elaborate on the risks of such concerns.

Cognitive Biases and Censorship

As Julius Caesar remarked, ``People readily believe what they want to believe."

Obviously the late great Caesar alluded to people’s proclivity to act in social norms. And as social norms, popular views are often dressed up as lies which are repeated so often and digested as the reality or the truth, especially when buttressed or promulgated by figures considered as “authorities” in their fields or from the bureaucracy. Yet, most people only look at the superficial and intuitive side of any issues without belaboring on the tacit intents proposed by the advocates or of its unseen consequences.

Bluntly put, people are basically faddish and tend to look for grounds to confirm or substantiate their beliefs or are predisposed to absorb only the quality of information which they believe suits their palate. In behavioral finance, this is known as the CONFIRMATION bias or “the tendency to search for or interpret information in a way that confirms one's preconceptions” (wikipedia.org).

Applied to social trends, the acceptance of mainstream views (or seeking “comfort of the crowds”) or conformity represents as the more psychologically rewarding route than in defiance of them (regardless of the validity of the observations or theories).

For instance, the mainstream has repeatedly mocked, jeered or scorned at those who warned of the illusions of the wealth derived from unsustainable debt driven boom. Contrarians were deemed or labeled as “killjoys” or “partypoopers”. Eventually as the boom turned into a bust, losses turned into reality, and the “IN” thing or “THE” social trend is now to be a pessimist.

The contrarians, who were previously the “outcasts”, have been exonerated and have now commanded sufficient clout of an audience enough to be embraced by mainstream media. In short, since media’s role is to sell what is mostly in popular demand, the Celente interview represents as pessimism becoming an entrenched social trend.

And that’s why gloomy videos have found their way into social networks. And that’s why too, we should expect more of these until perhaps we have reached the stage of “revulsion” or “capitulation” for one to reckon the US as in a “bottoming” phase.

Remember, throngs of “finance and banking” professionals or organizations (such as banking institutions, insurance and hedge funds) have not been eluded from such basic human frailties of “crowd” following or falling prey to “confirmation bias”. As the present bust or crisis clearly shows, technical expertise or even quant algorithmic models can’t substitute for the process ability driven emotional intelligence which is more a required attribute in the analysis of the market’s risk-reward tradeoff. As we have discussed in many occasions, most of them have even fallen prey to Ponzi schemes as the Bernard Madoff or the Robert Allan Stanford case.

I won’t suggest anyone to disregard extreme views especially if the Cassandra sports a good track record in projecting major trends and this includes Mr. Gerald Celente.

Yet, a remarkable past may not necessarily extrapolate to another successful forecast. Since any mortal can only wield so much of limited information in a highly complex world, like anyone else, his views aren’t infallible. The point is to understand the merits of his argument than simply to dismiss it out of the Pollyannaism or blind optimism or from the outrageous belief of a messianic salvation from the present leadership or fanatical subscription to the economic school of orthodoxy.

Worst of all, is the implication for the socialistic bent of “censorship” by those intolerant of diametric or contradictory perspectives. One should ask: would it be better for us to adhere to fantasies masquerading as truth and eventually suffer? Or would reading an expository “falsifiable” mind be a better alternative as to recognize potential risks and prepare for them?

The Fundamental Problem: UNSUSTAINABLE DEBT

So what seems to ail the US economy so much as to risk turning its political economy into an emerging market?

This from Bloomberg, ``Bill Gross, co-chief investment officer of Pacific Investment Management Co., said the Federal Reserve’s purchases of Treasuries and mortgage securities won’t be enough to awaken the economy.

``We need more than that,” Gross said today in a Bloomberg Television interview from Pimco’s headquarters in Newport Beach, California. The Fed’s balance sheet “will probably have to grow to about $5 trillion or $6 trillion,” he said.”

The Fed’s balance sheet is roughly around $2 trillion with an additional $1 trillion more for the QE as it gets implemented. This brings the Fed’s balance sheet around $3 trillion. Mr. Gross has asked to double the size.

Now this from Jeremy Grantham an erstwhile ferocious stock market bear whom has turned into a raging bull recently said, ``To be successful we need to halve the level of debt. Somewhere between $10 trillion and $15 trillion will have to disappear."

So how do we do that? ``Grantham sees three ways, according to the Wall Street Journal, “to restore the balance between private debt levels and asset values.” That is by “1) Drastically write down debt, 2) let the passage of time wear down debt levels, 3) “inflate the heck out of our debt” and reduce its real value.” (bold highlight mine)

In short, the fundamental problem comes with the government policy induced overdose of debt intake as shown in Figure 1.

Figure 1: American Institute for Economic Research: Total Debt by the US

Figure 1: American Institute for Economic Research: Total Debt by the US

AS you can see, the debt ratios for the US economy mostly held by the private sector have exploded beyond the nation’s paying capacity, according to the AIER, ``The debt-to-dollar ratio currently tops $3.50, more than double the ratio of 50 years ago.”

Given the unsustainable debt structure from which the US and the world economy has been built, the recent collapse in the financial markets (estimated at $50 trillion-ADB) and the subsequent meltdown in global trade, and investments (or deglobalization) has managed to reduce parts of such massive scale of imbalances.

But the adjustment process has a long way to go.

The US Federal Reserve’s Agency Problem

However instead of allowing for an orderly rebalancing of the US economy by permitting institutions that took upon the unnecessary burden of the speculative excess to fail or undergo bankruptcy proceedings, the US government has been pushing to revive the past Ponzi financing model by substituting the losses from these institutions with taxpayer money…to no avail so far.

And the Federal government’s heavy handed interventions in many significant parts of the economy and the prevention of price discovery has contributed to the prolonged nature of recovery and has added uncertainties in the marketplace, by distorting market price signals and altering the incentives for market participants which has been skewed towards prospective actions of the government.

The recent fracas of over the bonuses is a case in point.

Take this article from the New York Times,

``As public outrage swells over the rapidly growing cost of bailing out financial institutions, the Obama administration and lawmakers are attaching more and more strings to rescue funds.

``The conditions are necessary to prevent Wall Street executives from paying lavish bonuses and buying corporate jets, some experts say, but others say the conditions go beyond protecting taxpayers and border on social engineering.

``Some bankers say the conditions have become so onerous that they want to return the bailout money.”

In other words, some banks have resisted availing of government bailouts because of the burdensome conditions imposed on them, which is not helping the situation at all. As we said earlier the incentives in trying to normalize bank operations are being contorted by minute by minute changes in government intervention. Investors look for stability in policy.

And how much of these government intervention has been affecting the banking industry? The same New York Time article admits…

``At the height of the savings and loan crisis in the 1980s and 1990s, Congress and regulators adopted new rules known as “prompt corrective action” that required the government to quickly close weak financial institutions if they could not raise money to absorb mounting losses.

``The rules were a response to a consensus that keeping weak institutions open longer, under an earlier practice known as forbearance, damaged healthy banks competing with the government-subsidized ones and ultimately destabilized the banking system. By shutting weakened institutions before their losses grew, prompt corrective action was also seen as less costly to taxpayers and the deposit insurance fund.

``Administration officials say that some of the banks at issue today are simply too large to be seized by the government, making comparisons to the savings and loan crisis less meaningful.”

But this is exactly what has been happening today, damaged banks have been competing with government subsidized ones at the expense of the industry and the economy. And much worst, those subsidized are banks have been TOO LARGE to be seized by government, which is why the accrued losses have led to a creeping nationalization. See figure 2…

Figure 2: BCA Research: Top 20 Banks

Figure 2: BCA Research: Top 20 Banks

According to the BCA Research, ``The Chairman of the FDIC, Sheila Bair, contends that U.S. banks are well capitalized. However, she must be referring to the multitude of small banks, rather than large banks (i.e. there are many small banks that are well capitalized). The top 20 financial institutions have a thin capital cushion of only 3.4% (defined as tangible capital/total assets). In other words, it would require a writedown of total assets of only 3%-4% to wipe out all tangible capital for the largest banks. The FDIC data on the broader banking universe confirms that the capital cushion of large banks is much less than their smaller counterparts. Moreover, toxic assets are concentrated in large financial institutions.”

As you can see the risk profile of the top 20 banks have largely been because of the Level 3 assets which simply means ``Assets whose fair value cannot be determined by using observable measures, such as market prices or models.” (investopedia.com)

And what are the possible Level 3 assets? Perhaps figure 3 may provide the explanation…

Figure 3: OCC: 3rd quarter Report: The Average Credit Exposure to Risk Based Capital

Figure 3: OCC: 3rd quarter Report: The Average Credit Exposure to Risk Based Capital

The average credit exposure to risk based capital in percentage is 317.4% for the 5 largest banks as of the third quarter of 2008! The pecking order of the riskiest banks: HSBC (664.2%), JP Morgan (400.2%), Citibank (259.5%), Bank of America (177.6%) and Wachovia (85.2%).

Moreover, consider that 96.9% of the total derivatives of the US commercial banking system is held by the just these 5 institutions according to the Comptroller of the Currency Administrator of National Banks!

In other words, of the 8,451 banks and savings institutions insured by the FDIC, or of the 7,203 commercial banks operating in US (Plunkett Research), 5 banks have essentially held hostage the entire industry, if not the economy!!!

Free market anyone?

Why is this?

Could it be because the US Federal Reserve is a privately held corporation, bestowed with a monopolistic power to create and manage the country’s legal tender, whose complex web of owners could be some of the same institutions that are presently being rescued?

According to James Quinn, ``Most Americans believe that the Federal Reserve is part of the government. They are wrong. It is a privately held corporation owned by stockholders. The Federal Reserve System is owned by the largest banks in the United States. There are Class A,B, and C shareholders. The owner banks and their shares in the Federal Reserve are a secret.”

As Henry Ford once wrote, ``It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.”

So could Mr. Celente’s dire projections have been partly premised from such agency problem or conflict of interest issues that would perhaps gain national consciousness over the coming years?

Regulatory Arbitrage + Regulatory Capture=Market Distortion

In addition, considering the US banking industry have been a heavily regulated industry, why have the core institutions, which originally attempted to disperse risk by introducing financial innovations, ended up with the “risk concentrations”?

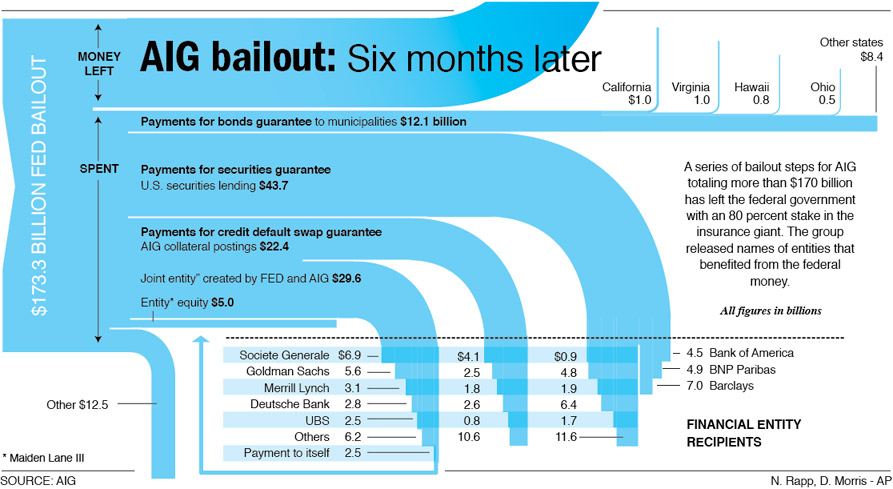

This from Gillian Tett of the Financial Times, ``After all, during the past decade, the theory behind modern financial innovation was that it was spreading credit risk round the system instead of just leaving it concentrated on the balance sheets of banks.

``But the AIG list shows what the fatal flaw in that rhetoric was. On paper, banks ranging from Deutsche Bank to Société Générale to Merrill Lynch have been shedding credit risks on mortgage loans, and much else.

``Unfortunately, most of those banks have been shedding risks in almost the same way – namely by dumping large chunks on to AIG. Or, to put it another way, what AIG has essentially been doing in the past decade is writing the same type of insurance contract, over and over again, for almost every other player on the street.

``Far from promoting “dispersion” or “diversification”, innovation has ended up producing concentrations of risk, plagued with deadly correlations, too. Hence AIG’s inability to honour its insurance deals to the rest of the financial system, until it was bailed out by US taxpayers.”

Institutions as the AIG Financial Product (AIGFP) circumvented or went around regulatory loop holes to ante up on leverage and increase risk exposure in order to generate additional returns. Arnold Kling of Econolib.org quotes Houman Shadab, ``AIGFP was treated as a bank for its counterparties' risk-weighting purposes, but AIGFP was not regulated as a bank (or an insurance company) for its own CDS credit exposures (had it been, it would've had to set aside capital/reserves).”

In short, this hasn’t been a free market problem as some anti-market pundits paint them to be, but one of regulators conspiring with Wall Street participants to “game the system”.

For Wall Street it had been one of regulatory arbitrage (profiting from legal loopholes) but for the regulators it has been one of regulatory capture (situations where government acts in favor of the interest groups of which it is regulating).

As we have previously quoted Robert Arvanitis Risk Finance Advisers, in Seeking Beta: Interview with Robert Arvanitis, ``Being mortal, the bureaucrats desire to avoid pain is as dear to them as the desire by their counterparts in private industry to seek gain. And it is far more profitable to game the rules, for example, than to enforce them. And any system can be gamed.”

To quote Mr. Celente, ``It was Fed finagling, Washington deregulation and Wall Street’s compulsive gambling that created the crisis.”

Yet people have been distracted by the most recent BONUS issue, which simply implies that Americans have been looking for an issue to vent their wrath on (a misguided one though).

To consider, the enormous backlash over the $168 Million is a pittance over the money spent by US taxpayers ($178 BILLION) to sustain AIG counterparties as Goldman Sachs ($12.9 billion), Merrill Lynch ($6.8 billion), Bank of America ($5.2 billion), Citigroup ($2.3 billion) and Wachovia ($1.5 billion). Big foreign banks also received large sums from the rescue, including Société Générale of France and Deutsche Bank of Germany, which each received nearly $12 billion; Barclays of Britain ($8.5 billion); and UBS of Switzerland ($5 billion) and some 20 largest states (New York Times).

Yet as the Federal government expands its presence into industries these governance conflicts, e.g. as in the proposed bonuses of Freddie Mac and Fannie Mae, will certainly serve or operate as a major disincentive that would impact diverse institutions from meeting desired goals, which eventually results to an increased overall inefficiency in the system.

Again, with big government comes the inevitable ramifications: resource allocation inefficiencies or wasteful spending, incompetence, corruption, dispensation of favors to political constituents, conflicts of interests, governance conflicts which may lead to organizational demoralization and reduced productivity, bureaucratic rigidities (tendency to be too technical or legal), crowding out of private sector investments, massive distortion of incentives, a vague pricing system which increased uncertainties and other impediments –all of which obstructs on the US’s economy wellbeing.

Obviously, governance policies based on populism will do harm than good.

Signs of Resurgent Inflation?

Now that the US policymakers appear to be losing out of ammunition, they have begun to openly resort to the crudest of all central banking policy approach-money printing.

As mentioned above our money experts have recommended “inflating away debts levels” which means reducing the currency’s purchasing power (or raise price levels) in order to diminish real debt levels, from which our policymakers have obliged.

According to the Economist, ``Mr Bernanke showed his own will on Wednesday March 18th, when the Fed’s policy panel said it would purchase $300 billion in Treasury debt, mostly maturing in two to ten years, starting next week. It will also boost its purchases of mortgage-backed securities to a total of $1.25 trillion from a previously announced $500 billion, and its purchases of debt issued by Fannie Mae and Freddie Mac, the mortgage agencies, to a total of $200 billion from $100 billion.”

But since the US is privileged to have her debts denominated on her own currency, when she can’t payback her obligations, instead of defaulting, she may resort to flooding the economy with money enough so as to reduce the value of liabilities at the expense of her existing creditors-i.e. local savers and foreign creditors.

Of course, these will temporarily benefit those who own financial assets, because “money out of thin air” will likely be absorbed by the institutions who will sell their portfolio of treasuries or mortgages to the US government. Eventually, the proceeds can be expected to be recycled into the financial markets. Although the policymakers are hoping that a revival in the capital markets will fire up the credit process by reigniting the speculative “animal” spirits.

Unfortunately the “moneyness” of Wall Street instruments (e.g. structured products, MBS, ABS etc…) has been lost and is unlikely to be revived anytime soon.

But on the other hand, any flow of credit to parts of the world where credit conditions have remained unimpaired is likely to fuel a surge in asset prices first, then consumer prices, next. Apparently such dynamics appear to have emerged, see Figure 4.

Figure 4: A Return of Inflation?

Figure 4: A Return of Inflation?

Oil has sprinted beyond the $50 mark and this has been accompanied by Dr. Copper (upper window) and even some industrial metals. Oil’s rapid rise may suggest of a rising wedge or a forthcoming decline. Anyway, the surge in key commodity prices comes alongside with a rally in Dow Jones Asia (ex-Japan) seen at the pane below the main window and Emerging Markets index (lowest pane), as the US dollar index suffered its 3rd largest one day decline.

The unfortunate part for the US is that a resurgent inflation will likely induce more sufferings to the middle and lower class and possibly worsen the political scenario by provoking a “class” conflict.

When price levels of consumer goods are raised at a time when unemployment is high or possibly even growing, where real income levels are also diminishing, and where corporations faced with a struggling environment will be faced with higher costs of operations, these combined could redound as the ingredients for a large scale hunger triggered political malcontent.

Moreover, inflation, as seen through higher cost of money and shrinking purchasing power, is likely to wreak havoc on the cash flows of those attempting repair their overleveraged balance sheet by increasing savings and paying off debts.

And the orthodoxy is putting so much hope that the authorities will know the right time when to close the barn doors before the horses run astray, a hope that seems unfounded to begin with as the authorities have failed to recognize the crisis in advance or limit the scale of its impact.

Again from Mr. Celente, ``What "steps?" The Bernanke Two-Step? Adjust interest rates or print more money? Neither stopped the credit crisis from worsening, the real estate market from tanking or the stock markets from crashing.”

Figure 5: yardeni.com: Net Foreign Selling Are These Signs On The Wall?

Figure 5: yardeni.com: Net Foreign Selling Are These Signs On The Wall?

The United States’ Treasury International Capital flow have registered a significant net foreign selling (excluding US T-bills) last January see figure 5, although as an important reminder-one month does not a trend make.

While others have argued that such fall in capital flows may have been a function of reduced growth of foreign exchange surpluses, the growing restiveness by global policymakers over the US dollar, could be another incipient dynamic at work.

Over the past weeks we heard resonating voices suggesting a move away from the US dollar as the world’s reserve currency- from Joseph Stiglitz, a UN Panel and Russia at the G20, which was reportedly backed by China, India, South Africa and South Korea.

While there has been no unanimity on the possible replacement, most have recommended the IMF’s Special Drawing Rights or the old European Currency Unit Ecu, albeit both of which have been “combinations of currencies, weighted to a constituent's economic clout, which can be valued against other currencies and against those inside the basket” (Reuters).

Importantly, a new currency can’t takeoff without OECD participation which includes the US. Thus, such cacophony appears to be more symbolic- an implied protestation over the risks of imprudent government spending.

Take The Risks of Hyperinflation With A Grain of Salt At Your Peril

Finally, we can’t discount the risks from the ravages from hyperinflation.

As we brought up in 2009: The Year of Surprises?, a tip over from deflation expectations towards a ramping up of inflation will be a tough act to manage. If government starts to tighten as inflation rises, the ensuing effect will be a sharp fall in prices from which government will need to restoke the inflation engine again.

Again to quote Murray Rothbard in Mystery of Banking,

``But if government follows its own inherent inclination to counterfeit and appeases the clamor by printing more money so as to allow the public’s cash balances to “catch up” to prices, then the country is off to the races. Money and prices will follow each other upward in an ever-accelerating spiral, until finally prices “run away,” doing something like tripling every hour. Chaos ensues, for now the psychology of the public is not merely inflationary, but hyperinflationary, and Phase III’s runaway psychology is as follows: “The value of money is disappearing even as I sit here and contemplate it. I must get rid of money right away, and buy anything, it matters not what, so long as it isn’t money.”

In essence Mr. Celente’s Tax Revolt, Food Riots, Revolution and the return to a banana republic or the state of an emerging market is nothing more than a function of hyperinflation. (Of course, we’re not suggesting that this will surely happen, but what we are saying is that the present actions of the US policymakers have been increasing the odds for such risks to occur. America’s hope depends on the world to absorb those surplus dollars enough to pull the US out of its debt trap.)

So for those hoping against hope that the present administration will deliver the economy’s much needed elixir in defiance of the fundamental function of the natural laws of economics, good luck to you. No economy has survived by merely the government running on the printing press, ask Dr. Gideon Gono.

One must be reminded of US 33rd President Harry S. Truman’s noteworthy comment, ``It's a recession when your neighbor loses his job; it's a depression when you lose your own.”

Take this risk with a grain of salt until such scenario becomes a personal depression.

Philippines leads in the technology usage of Microtransactions via SMS or text messaging...

Philippines leads in the technology usage of Microtransactions via SMS or text messaging... as the industry is backed by a 57% Penetration level in mobile subscription

as the industry is backed by a 57% Penetration level in mobile subscription

{kind=link}