If past history was all there was to the game, the richest people would be librarians—Warren Buffett

In this issue

A Terse Review of the Q3 and 9-Month Philippine PSEi 30 Financial Performance: Companies Turn Defensive

I. Q3 and 9-Month PSEi 30 Financial Performance: Companies Go Defensive

II. Financials Buoyed the Underperforming Revenue and Net Income Performance in Q3

III. San Miguel, JGS and BDO Among the Top Revenue and Income Performers

A Terse Review of Q3 and 9-Month PSEi 30 Financial Performance: Companies Turn Defensive

Economic uncertainty has prompted most of the PSEi 30 members to turn defensive.

I. Q3 and 9-Month PSEi 30 Financial Performance: Companies Go Defensive

Let us begin with the examination of the Q3 review of the PSEi 30 financial performance with this note.

Or, for clarity purposes, let me categorize the following charts.

A1. Consist of data covering the same PSEi 30 members during the stated period.

A2. This chart represents the typical apples-to-oranges, which discounts the marginal changes in PSEi 30 members in a given timeframe.

Figure/Table 1

The table summarizes the net 9-month changes (A1) of specific categories of the PSEi 30 in the last four years.

In the nine months of 2023, the marginal or net changes in all categories, namely, debt, revenues, income, and cash, were considerably lower than a year ago: All posted a contraction YoY in percentages.

The gist: Many companies went into a defensive mode.

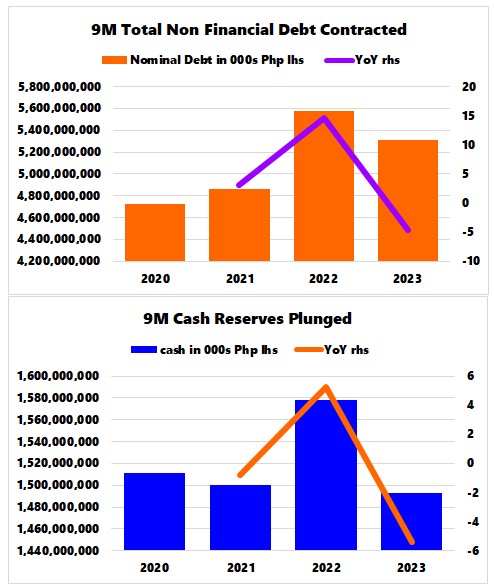

Figure 2

Some pared down the use of debt to finance operations, resulting in its decreases. However, that's after debt levels hit a high in 2022 (A2). (Figure 2, upper window)

Others tapped their existing cash stockpile, thereby the reduction in cash reserves. Since peaking in 2020, cash reserve growth has eroded, which led to a contraction last year (A2). (Figure 2, lower graph)

Many used a combination of the above.

Inflation has been an instrumental force in the decrease in revenues and income, as well as the surge in debt in 2023.

In the nine months of 2022 and 2023, the headline CPI averaged 5.1% and 6.6%, respectively.

Figure 3

Both revenues and income soared to a record in 2022 as inflation followed (A2). Though both categories topped the 2022 high in pesos, a slowdown in % growth characterized 2023. (Figure 3, top and middle graphs)

Revenue growth (33.3%) vastly exceeded the Nominal GDP (13.3%) in 2022, perhaps indicating a much higher inflation rate than published. (Figure 3, lowest chart)

Nominal GDP of 10.7% exceeded revenue growth of 6.4% in 2023, suggesting the embellishment of the former.

Total revenues of the elite 30 group signified 27.9% of the nominal GDP, which points to the degree of concentration of financial power held. And that excludes other non-PSEi 30 firms, which understates their contribution. Nonetheless, it is a symptom of the BSP's implicit "trickle-down" policies that have been instrumental in forging an oligarchic-crony (neo-socialist "fascist") capitalist political-economic system.

In any case, that many companies took upon economic uncertainty to reduce debt should be good news. However, the slump in cash levels indicated the emergence of liquidity strains.

II. Financials Buoyed the Underperforming Revenue and Net Income Performance in Q3

Figure/Table 4

Let us dissect the PSEi 30's performance by sector.

In the 9 months of 2023 (9M), the industrials registered the highest % increase in debt, but holding firms (which included their subsidiaries) had the highest peso increase.

The property sector posted the highest % gains in revenues and in net income.

However, the property sector used its liquid reserves to fund operations, resulting in the most % decline in cash.

The slowdown in Q3 2023 weighed on revenues and net income growth.

Though 9-month revenues posted a 9.08% growth, it was pulled lower by the 4.03% growth in Q3. Thanks to the outperformance of the Financials, which cushioned the general stagnation.

Q3 revenues and income contributed 34.03% and 32.84% to the 9M output, respectively, which revealed that Q3 activities had more impact on revenues than income.

Nota Bene: This analysis reports on the disclosures, the accuracy of which is beyond our jurisdiction.

To this end, all these exposed the weakness of the corporate world in the Q3 GDP, which reinforces the expanded role of deficit spending in Q3 GDP.

Bluntly put, the 5.9% Q3 GDP was a statistical mirage.

III. San Miguel, JGS and BDO Among the Top Revenue and Income Performers

Figure/Table 5

Finally, we examine the individual performance of the incumbent PSEi 30 members.

First, 13 of the 27 non-financial firms trimmed their debt levels.

While power firms ACEN and Meralco posted the highest % increase, SMC was singlehandedly the biggest borrower, with 72% of the Php 213 billion net increase.

JGS logged in the highest net income growth in % and pesos. In pesos, SMC and SM followed.

With aggressive lending and investing, the three banks (BDO, BPI and MBT) clocked in the fastest revenue growth, but SM and BDO had the most increases in pesos.

Newcomer food company CNPF had the most increase in cash reserves in %, but holding firm AEV and power Meralco posted the highest gains in pesos.

Meanwhile, while SMC had the most increase in debt, it also had the most decline in cash reserves in pesos.

Figure/Table 6

In Q3, SMC and JGS clocked in the fastest net income growth rate.

But the former and AC had the most gains in pesos.

Again, the top three banks monopolized the pace of advance in the revenue growth rates. Meanwhile, BDO and JGS recorded the highest revenue growth in pesos.

In the end, while many companies have started to reduce their leverage, income has yet to increase to levels necessary to provide sufficient liquidity. It also reveals that the incumbent business model of the PSEi 30 hasn't been organic or productivity-driven. Instead, it represents a debt-fueled growth paradigm.

Still, the skewed distribution of debt, revenues, net income, and cash puts into the spotlight the mounting manifold risks of credit-financed growth, malinvestments, concentration, and contagion.

No comments:

Post a Comment