``Joseph Schumpeter analysed the Great Depression in terms of "creative destruction". He thought that cyclical recessions and depressions wiped away obsolete economic systems and allowed them to be replaced by fresh structures. Recessions are necessary to speed up the capitalist forces of change. For the last 33 years, the Chinese economy has been growing two to three times as fast as the United States, and that has continued even in a year of recession. The Asian economy has been taking over the lead from the Western economy, though the performance of the Japanese economy has been disappointing. I expect that this Chinese outperformance will continue as the world moves into recovery. We can now see the pattern of the three centuries: 1815–1914 the British Empire; 1945–2008, the American era; about 2030–2100 or beyond, the new Chinese era. China is overtaking the West and the process has been accelerated by the recession. William Rees-Mogg The New Chinese Era

It’s a refreshing return from an extended vacation.

Not only have most people have recharged their energies, but even our Philippine Stock Exchange appears to have been rejuvenated as well.

Amidst persistent gloom, this analyst has been reiteratively asserting the case for a return of the bullmarket. For instance last March in Why An Increasingly Asset Friendly Environment Should Benefit The Phisix we outlined the reasons as: 1. Extremely Depressed Mainstream Sentiment, 2. Creative Destruction, 3. Perspective Shift from the Macro to Micro environment, 4. Policy Incentives Are Directed Towards Aggressive Risk Taking, 5. Signs of Improving Trends in the Marketplace, 6. Phisix: Learning From Market Cycles.

Already substantial segments of these variables have begun to sink in the collective psyche.

Global markets have been on a tear lately principally led by Emerging Markets and Asia. Key emerging markets (BRIC) have tallied double digit gains on a year to date basis [see Global Stock Market Performance Update: The BRICs and Emerging Markets Dominate Gains] against G-7 economies (except Canada) who still are on the red (as of April 16th), despite the March 9th rally using the US markets as the reference point.

This glaring disparity of performance in both the financial markets and economic growth rate (China registered a first quarter growth of 6.1% growth in 2009 while India reportedly grew less than 7% for 2008 relative to negative growth in G-7 economies) appears as significant validation of the much derogated or demeaned “decoupling” theme in 2008.

The Policies of Greed

Against mainstream macroeconomists and their coterie of followers, who tend to “tunnel” their visions of a world rigidly driven solely by US demand, and of the misguided worries of “deflation” given the premise of intractable debt, oversupplies and excess capacity as their elementary case for a global “stagdeflation” bust setting, the ping pong surges between global stock markets and commodities have been corroborating our case of a market response towards a collective policy overdrive from inflationary actions by global governments.

Put differently, inflationary policies in many parts of the world have started to offset losses from the financial and economic system and has begun to “leak” or percolate into financial assets as the stock markets and the commodities.

For as long as global government will continue to “print money” and adopt negative real rates, savers will be penalized, and “printed money” (if not from the private sector then by government spending) will find its way into assets as speculation have been the order of the day. Where unlimited money will be chasing limited goods or assets, the end result will be inflation.

For our blessed dear Pope Benedict XVI, let it be known that GREED is the OFFICIAL POLICY of collective governments. The seeds for the next crisis are patently being legally sown. People are being impelled to borrow and speculate than to save and produce. Hence, blame not greed on the public when the next crisis arrives because people would be simply responding to the incentives set forth by policymakers in order to survive. Otherwise, defiance to these policies translates to a loss of purchasing power.

And as day follows night, inflation will be succeeded by deflation. Last year’s collapse in the economic and financial system was a manifestation of a market response to an unsustainable system. Today’s government induced efforts to revive the marketplace with too much debt charged to the expense of the citizenry will ultimately end up with the same results- a crisis.

For as long as people continue to trust governments, governments will have the ability to counter deflationary forces with “money from thin air” or the printing press. But as history shows, the grandest experiment with the paper money system will ultimately reach a limit.

Nonetheless, the genesis of the next crisis begins almost always with a government sponsored boom.

Who Will Finance This Boom?

In contrast to 2003-2007 boom, which saw much of the easy money policies absorbed by real estate industry in developed economies which had been facilitated or greased by financial alchemy by both the banking system and the moneyness of Wall Street’s “shadow banking system”, this boom will probably be financed by financial conduits that would cater to the stock market and commodities boom.

Figure 1: US Global Investors: Credit as % of GDP

Figure 1: US Global Investors: Credit as % of GDP

Aside from global governments, it is not apparent yet where the private sector funding will emanate from, but our guess is that the scope of debt absorption will be greater for economies in the emerging markets where the leverage in the system have been low relative to developed economies see figure 1.

This is a chart I’ve shown in Will Deglobalization Lead To Decoupling?.

For instance the Philippines have one of the lowest exposures to credit by households. This explains why there have been aggressive marketing efforts to sell credit cards which I can attest to (I receive many offers to subscribe to bank credit cards).

Since most emerging markets are bank financed more than capital market financed, then we should see substantial growth in activities in these lagging but high growth areas. Although, for emerging markets to further capitalize in the speculative fever, we should equally expect a tremendous surge in non-banking finance to complement the growth in the banking system.

Figure 2: US Global Investors: Exploding Loan Growth in China

Figure 2: US Global Investors: Exploding Loan Growth in China

We have already been partly witnessing the emergence of this phenomenon in China, as loan growth amidst loose monetary policies has been exploding at a vertiginous pace see figure 2.

From Wang, Yam, Zhang and Tai of Morgan Stanley, ``In particular, policy-driven monetary expansion drove money and loan growth to record highs in March, up 25.5% and 29.8%Y, respectively, with new loans made in 1Q09 totaling Rmb4.6 trillion, almost 3.5 times the amount in the year-ago period, or 93% of 2008’s total.” Apparently the present policies have buttressed urban fixed asset or real estate investments and domestic consumption even as the external environment (exports) remains feeble.

The fact that such dramatic pace of growth in loans is unsustainable means that at some point this year these trends will need to moderate which likewise suggests of a meaningful correction in Shanghai’s index (up 37.5% year to date).

In addition, if China tacitly expects to expand the use of its currency, as possible challenger to the reign of the US dollar as the world’s international reserve currency, then it would have to make its currency convertible by liberalizing its capital account and importantly by deepening its capital markets. Importantly in terms of politics, it would have to expand its military might, which it has been doing reticently. According to the Wall Street Journal, ``The Pentagon views China as the country most to acquire the capacity to challenge the U.S. likely, at some point down the road, military on a global scale.” But this is a discussion for another day.

Hence, ASEAN and East Asian markets will likely revolve around the progress of China to augment the liberalization and the integration process of its markets and its economy to the region and to the world.

Has correlation an implied causation? Perhaps. See figure 3.

Figure 3 US Global Investors: Chinese Demand a Driver for Emerging Europe?

Figure 3 US Global Investors: Chinese Demand a Driver for Emerging Europe?

According to US Global Investors, ``Rapid monetary expansion in China would not only provide fundamental support for government-mandated fixed asset investment vital to reinvigorate domestic growth, but could also serve as a precursor to global economic recovery and sustain positive investor sentiment toward emerging markets in general. That Chinese money supply growth has been leading Emerging European equities in the past four years should not be mere fortuity.”

Hence, this crisis has only begun to show of China immensely expanding leverage in the global economy. As we wrote last October in Phisix and Asia: Watch The Fires Burning Across The River? ,

``In the “Secrets Of War: The 36 Stratagems” published by an unknown writer during the Ming Dynasty 300 years ago, one of the war stratagems include “Watch the Fires Burn Across the River”, which means to watch over your enemies wreak havoc upon themselves before making your move. As senseis.xmp.net interprets ``This is a kind of long-term, strategic version of the idea behind an inducing move. Before you intervene, see that the flow of the game started by action elsewhere brings the opportunity to its peak.”

``If the US took the hegemon away from the UK after the latter had suffered immensely from the harrowing years of devastation wrought by World War II, could Asia be in a seemingly parallel position in terms of fortuitously eluding the systemic calamity of a banking crisis besetting the West?”

Or has China used today’s opportunities to position herself for prospective strategic dominance?

Locally Driven Global Markets

Another important difference from the 2003-2007 boom: This emerging boom seems to be driven locally.

Figure 4: Danske Emerging Briefer: Phisix and Peso Lagged Emerging Markets in March

Figure 4: Danske Emerging Briefer: Phisix and Peso Lagged Emerging Markets in March

The Philippine Peso and the Philippine Phisix have lagged its emerging market peers last March.

One possible reason for this is that the Philippine Peso hasn’t been pummeled as the rest of its contemporaries during the most recent rout, where much of the recent spike in global equity markets have equally translated to a marked rebound in these downtrodden emerging market currencies. Said differently, the sharp volatile downturn resulted to an equally rapid upturn. This is in contrast to the Peso which had been impacted less and has similarly had muted improvements.

The other possible reason is that foreign participants remain as significant net sellers. The volume to push blue chip issues higher is relatively sizable, hence considering the low penetration level of local participants in the stock market (less than 1% percent directly invested, according to the PSE; our estimates at 1% including indirect placements), the market improvements have been seen mainly broadbased or spilling over to second or third tier issues- where less volume is required to spark upside volatility- but moderated in terms of blue chip issues or issues composing the Phisix.

Last week’s foreign selling had been substantial (Php 2.25 billion), such degree of volume foreign liquidation usually coincides with significant downsides in the Phisix. Yet the Phisix climbed 1% over the week.

In addition, the recent controversial “political” deals might have partly contributed to the persistent foreign disinterest to hold local equity assets.

In short, for the meantime there has been a dearth of firepower from local investors to sturdily power up blue chip issues. Yet foreign selling has weighed on both the Phisix and the Peso. But this is likely to change in the future as confidence or improving market sentiment gets reinforced. Perhaps local investors will be increasing their or we could see a return of foreign investors, possibly from Asia than from the West.

Has the Philippine experience likewise been reflected on its contemporaries? Perhaps.

An article from US Today appears to have misread an emerging market flow data because of its misleading headline “Emerging markets funds up, but rely on developed world”. The article reports that,

``This year, investors have put $5.5 billion of net new money into emerging market stock funds, says Brad Durham, managing director of Emerging Portfolio Fund Research, which tracks the funds.

``To put that into perspective, the funds have attracted new money equal to about 2% of their assets each week for the past month, according to TrimTabs.com, which also tracks fund flows.”

According to FP Trading Desk the market capitalization of Emerging Markets is around $12.8-trillion in March of 2008. Considering that half of this has been lost, this takes market cap to around $6.5 trillion, yet it is inconsistent to see how $5.5 billion or even 2% of assets could have made emerging markets “rely” on developed world.

Figure 5: US Global Investors Russia’s Investor’s Profile

Figure 5: US Global Investors Russia’s Investor’s Profile

Well Russian markets appear to be confirming the developments in the Phisix-local investors are driving the market.

According to US Global Investors, ``There was a significant increase in activity recently in Russian equity markets, mainly driven by domestic buyers. As the chart from J.P. Morgan shows, local activity outnumbers long international money by a two-to-one ratio.”

A locally driven stock market boom will be less susceptible to global gyrations and strengthen our case for decoupling.

Phisix: Rising Tide From Inflationary Forces

As we have noted earlier, the Philippine Stock Exchange have been experiencing a broad based recovery.

This can be seen in virtually ALL of our market internal indicators: advance-decline spread, number of traded issues, number of trades, peso volume or even the seeming emergence of a “rising tide lifts all boats” among sectoral trends see figure 6.

Figure 6: PSE: Rising Tide Lifts All Boats?

Figure 6: PSE: Rising Tide Lifts All Boats?

As you will note in the chart, ALL of the indices have turned positive, whereas only two of them, particularly the Industrial and Mining indices were on the upside early this year.

And leading the pack anew is the Industrial index, which has been up 35.01% year to date (pink), followed by Mining index up 28.26% (green), the Banking index 15.05% (black candle), the Sunlife and Manulife dominated ALL index 13.53% (maroon), the Holding index 13.11% (red), the Service Index 4.32% (silver) and the Property index 4.18%.

And as opposed to mainstream domestic analysts who are paid to peddle the uncorrelated, unproven and unconfirmed premise that “fundamentals” drive the stock prices, we have long argued from a contrarian standpoint that stock prices have essentially been propelled by mostly INFLATION and INFLATION DRIVEN SENTIMENT, with accentuated influence for the underdeveloped Philippine market setting. Hence the “rising tide lifts all boats phenomenon”.

All the rest are mere nattering nabobs of cognitive biases disguised as expert opinions.

Some of the previous concluding quotes by Vienna Professor Fritz Machlup (1902-1983) from his invaluable paper The Stock Market, Credit and Capital Formation I cited in our January article Are Stock Market Prices Driven By Earnings or Inflation?, which I’d like to reemphasize (all bold highlights mine):

-A continual rise of stock prices cannot be explained by improved conditions of production or by increased voluntary savings, but only by an inflationary credit supply.

-Extensive and lasting stock speculation by the general public thrives only on abundant credit.

-Abundant funds, especially those of inflationary origin, may not find ready outlets in real investment.

-Any decrease in the effective supply of money capital is likely to cause disturbances in the production process.

-An inflated rate of investment can probably be maintained only with a steady or increasing rate of credit expansion. A set-back is likely to occur when credit expansion stops.

And if this is the genuine incipient boom phase of the next chapter of the imminent bubble cycle as we think it is, we’d most likely see “basura” issues or third tier highly speculative issues to SPECTACULARLY OUTPERFORM blue chips.

The Hazards and Relevance of Chart Reading, My Technical Outlook

Lastly as we have previously mentioned, the cogency of our bullmarket can be identified from several indicators, particularly: signals from market internal activities, regional performances, benchmark credit spreads and finally technical picture.

Figure 7: Stockcharts.com: PHISIX: Missing One Element To A Full Blow Bullmarket

Figure 7: Stockcharts.com: PHISIX: Missing One Element To A Full Blow Bullmarket

A short notice on chart reading: Although I began my market analyst work as a chart reader, I came to realize that charts depend only on past information and the subsequent pattern recognition as basis for predictions.

Despite the so-called “market efficiency” where all necessary information as supposedly imbued in the depicted prices, this isn’t accurate at all. Considering that markets have been repeatedly distorted by government intervention, with accelerating emphasis today, markets hardly convey price “efficient” signals as many dogmatic practitioners infer them to be. Hence, they have been highly vulnerable to “tail” risks.

Moreover, charting as a primary device for market reading is a tool beneficial for those who benefit from churning trades than from those working to achieve or generate ALPHA returns. Besides, by assuming only past information as the principal basis for market analysis, this represents, for me, as highly prone to cognitive biases, since our reflexes would be oriented towards spotting pattern recognition through the significance of the historically determined path dependent outcome (hindsight bias) and the oversimplification in the understanding of events as related to unfolding market action.

Thereby, I’d recommend the use of charts as vital guidepost for determining phases of the market cycle, as confirmation metric of inter-market developments to ascertain the whereabouts of the market cycle or of the stages of an investment theme and as for entry-exit parameters for a defined trade and NOT as primary “investment” or “HOLY GRAIL” formula for determining the risk reward tradeoffs.

Institutions that accustom clients towards short term trades are only subjecting the latter to low-return high-risk exposure, which serve nothing more than a euphemism for punts, especially for momentum trades. That’s where we always warn of the perils of the “agency problem” or the conflict of interest issues.

Going back to the market, the Phisix alongside the Asian bourses ex-Japan (DJP2), the Emerging Market (EEM) index and the Southeast Asian (FSEAX) index appears to have carved a similar basing feature which may be indicative of the bottoming phase of the present market cycle (double bottom?).

Moving forward, all four indices have simultaneously broken above their resistance levels which could be indicative of an advancing momentum tilted towards a transition to a full blown bullmarket. The Phisix recently overcame its hurdle (see green circle) at Friday’s close by going over the resistance (red horizontal line).

Although, only the EEM index has had a material breach above the resistance level, it remains to be seen if the other indices will suffer from a “head fake” or sustain a breakout that validates the advent of a nascent bullmarket for regional and emerging market equities. This will be evident in the coming sessions.

Given the near convergence of the motions of the major indicators, particularly market internal signals, regional performance, credit spreads and technical picture; it seems to be the first time in nearly two years where the alignment of these forces strongly suggests of a continuity of the present trend than of a reversal.

In addition, except for the Shanghai index which is not shown in the chart above, all four indices above are likewise closing in on their respective 200-day moving averages (for the Phisix the red descending line at approximately the 2,200 level), which serves as my last major obstacle for the Phisix (and the other equity benchmarks) to officially reclaim the next phase of the market cycle.

And after a successful breach of the 200-moving averages we can expect the Phisix to perhaps to recapture or regain some of the lost grounds in between the two targets (2,289 or 2,300 and 2,750 or 2,800) by the yearend. And optimistically, a full recovery and even an attempt at 5,000 during the market friendly Presidential election cycle year.

Because there seems to be no other asset class in Western nations that can absorb much of the paper money being thrown into the global financial system, as the tug of war between deflation and inflation will persist to generate extended market volatility, perhaps the inflation in the stock markets in Asia and Emerging Markets and in the commodities frontier will accelerate faster than the previous, as the ``inflated rate of investment can probably be maintained only with a steady or increasing rate of credit expansion” as Professor Machlup explains. Governments at the moment will resist a setback in the credit expansion that may reverse the present trends simply because rescues by printing money have become a political trend.

In short, the odds are greatly favoring a bull run for the Phisix, Asia, Emerging Markets and commodities going forward.

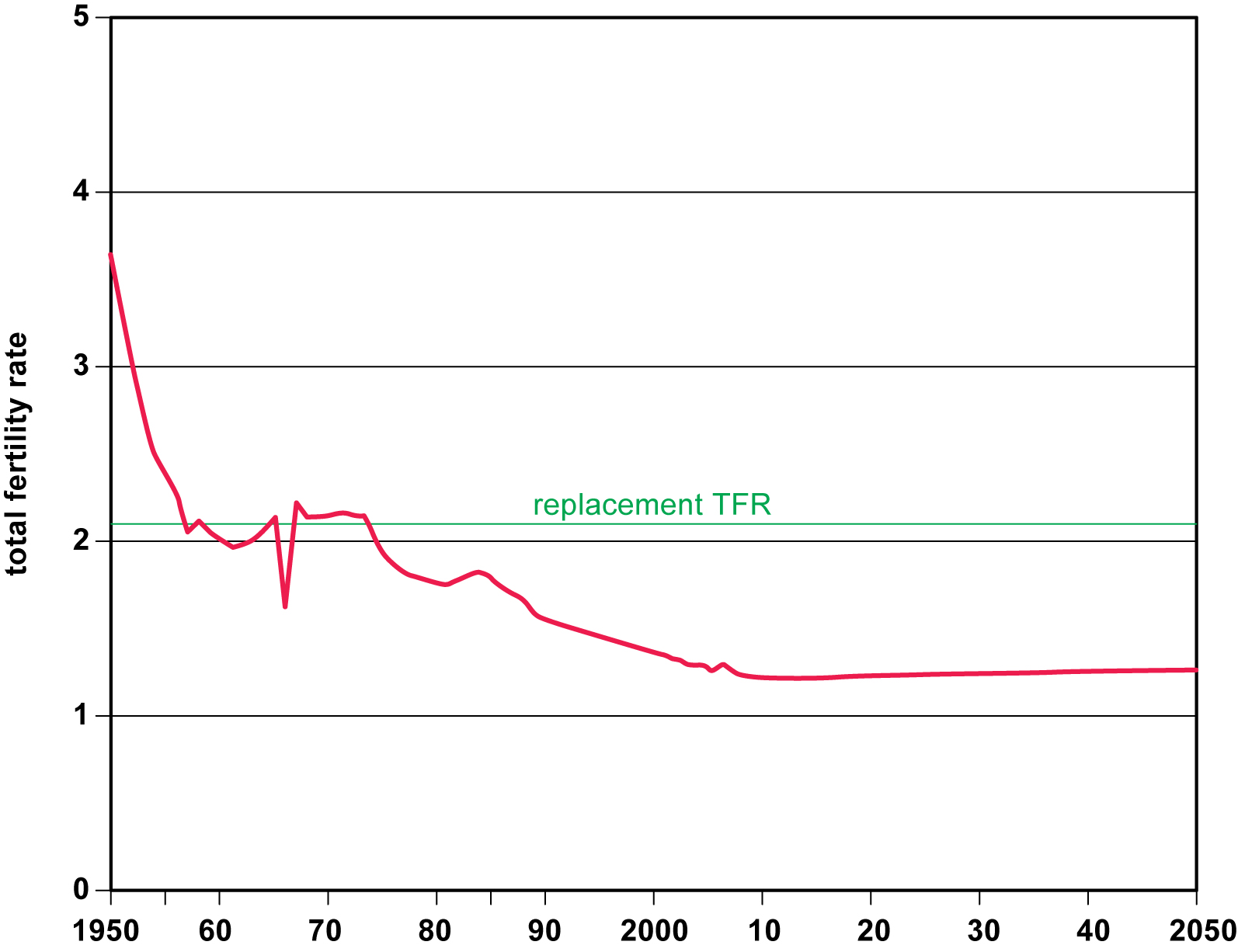

The present recession will not last forever. And as its economy recovers, Japan's dwindling population (see the above chart from japanfocus.org) will endure strains from labor shortages.

The present recession will not last forever. And as its economy recovers, Japan's dwindling population (see the above chart from japanfocus.org) will endure strains from labor shortages.

{kind=link}