I cannot find a single convincing argument that tells me that astrologers won’t do better than economists…The problem is the arrogance of these economists, they’re making people rely on theories that have not worked, do not work, and are really dangerous—Nassim Nicholas Taleb

In this issue

What Surprise is in Store for the 2024 Year of the Wooden Dragon?

I. Year of the Dragon: Leap Years, US Presidential Elections, Culmination and Escalation of Global Conflicts

II. Year of the Dragon: Eve of the Great Depression and the Year of the Dotcom Bubble Bust

III. Year of the Dragon’s Impact on the Philippines: GDP and CPI

IV. Year of the Dragon’s Impact on the Philippines: USD and the PSE

What Surprise is in Store for the 2024 Year of the Wooden Dragon?

Will the Wood Dragon roar in 2024?

From The Chinese Zodiac: The Year of the Wood Dragon 2024 is also known as Yang Wood on Dragon, or Jia Chen 甲辰 in Chinese. The fixed element of the Dragon (Chen) is Earth (Wu 戊), which represents stability, honesty and loyalty. The variable element of the Dragon in 2024 is Yang Wood, or Jia 甲, representing growth, creativity and flexibility. The Wood Dragon is the most creative and visionary of the dragons. They are optimistic, ambitious and adventurous. They like to explore new ideas and challenge themselves. They are also generous, compassionate and loyal to their friends. Therefore, the Year of the Dragon in 2024 is expected to be a time of visionary leaders, innovators and problem solvers. 2024 is also predicted to be a great year to start new projects, explore new opportunities and create value for yourself and others. (bold original)

I. Year of the Dragon: Leap Years, US Presidential Elections, Culmination and Escalation of Global Conflicts

Leap years are an outstanding feature of the Year of the Dragon.

Further, they are associated with US presidential elections. From 1952 to 2012, the distribution of Presidential victors had been even: 3 Republicans (Eisenhower 1952, Bush Sr. 1988, and Bush 2000) and 3 Democrats (Johnson 1964, Carter 1976 and Obama 2012). But a Democrat, Lyndon Johnson, won in the last Wooden Dragon in 1964. Will a Democrat President prevail this year?

We're no believers in astrology, but they occasionally provide propitious or serendipitous clues.

For instance, we cited the possibility of an outbreak of war in 2022, which included a buildup of Russia-Ukraine tensions. A month later, Russia launched its Special Military Operation against Ukraine, which remains ongoing.

The Year of the Dragon highlights both the end and escalation of conflicts. The Treaty of Taipei, signed and ratified in 1952, ended the Second Sino-Japanese War. The Soviet Union also withdrew from Afghanistan in 1988.

World War 2, which began in 1939, escalated in 1940 with the widening of the theater of war, which included the Battle of France, Netherlands, Belgium, and others.

In 1964, newly elected President Lyndon Johnson escalated U.S. involvement in the Vietnam War following the Gulf of Tonkin incident.

Also, the US military causalities in the fateful Afghan War reached a milestone of 2,000 in September 2012 and concluded in 2021 with a Taliban victory.

Applying to current events, could the Russia-Ukraine War culminate this year of the Dragon...with a Russian victory?

Will the Israel-Palestine War expand into a regional, if not a global war? The US and its allies have started to strike at Iranian-supported targets in Yemen, Syria, and Iraq even before the year of the Dragon.

The former US Presidential advisor, Ms. Pippa Malmgren, recently wrote that World War III is already here but unfolding in an unconventional process. (bold added)

People strangely assumed that WWIII would have to look and feel like WWII. They could not make allowances for the fact that technology had evolved and the domains of warfare have changed. As the Pentagon said last week, space is now the most important warfighting domain, and “space-based missions are essential to the U.S. way of war.” The war in Ukraine and the attacks from and in Gaza are only possible because of satellites. But, the media needs visuals and a storyline to explain conflict. Ukraine and Gaza are easy for the media because they fulfill the old requirements. There are dead humans, and there are shocking photo ops. The old rule still applies, “if it bleeds, it leads.” These events reinforced the idea of what a war looks like. It provided clear symbols of war, including tanks, troops, and bombings. Both are also land wars, which makes them easy to report on. You can send a journalist there. However, the actual war we are in is vastly larger and more serious, but it is in places the public can’t see and where there are no journalists – space, above and below the open oceans, in the realm of technology and cyberwar. The actual war between the superpowers and their proxies has been, until now, invisible. It has had no overarching framework in the media that a regular person can comprehend. So, the sudden warnings from a range of senior NATO Commanders that the public must be ready for war matter because the gap between the invisible war, and the visible war is finally closing. Spectators can start to see the invisible war now. (Malmgren, 2023)

Let us see.

February 2022: Russian-Ukraine War

October 2023: Israel-Palestine War

If the year of the Dragon spotlights escalation, will a third "major" front open in 2024? Where? The Middle East? Central Asia? East Asia? South Asia? Southeast Asia? The Arctic region? Europe? South America?

We carry over the same conclusion as last year.

Today, there are barely any signs that primary participants in the "hegemonic war" will sue for peace.

The lack of interest in negotiations by opposing parties, the sustained shipment of arms, the continued provocations and counter provocations, the widening coverage of the war to include economic and trade protectionism, and the weaponization of finance (US dollar) and commodities, and intensifying political propaganda—all point to mounting risks of escalation (nuclear exchange).

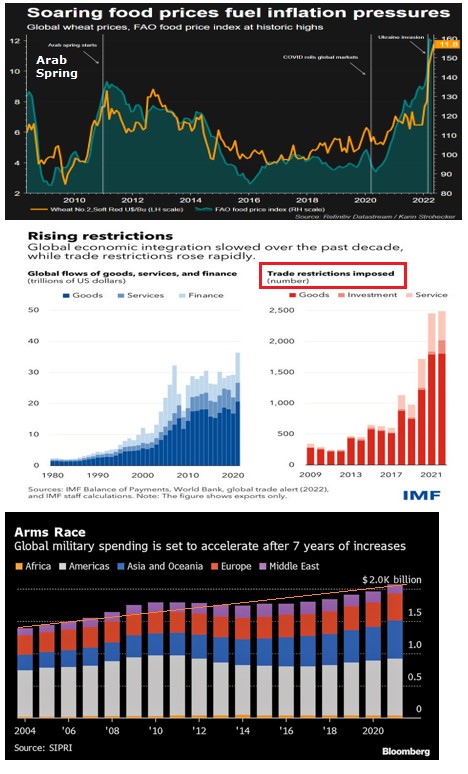

While trade protectionism has been on the rise, the war aggravated it.

Further, with the global economy skating on thin ice, wars serve as a convenient scapegoat to extend or expand the political tenures of the leaders.

Even worse, with expanding vested interests of the politically influential "triumvirate" sectors, perhaps the backbone of the deep state—the military-industrial complex, oil and energy, and finance industries—benefiting immensely from the "proxy" conflict, amicable settlement becomes less of an option for their political leaders.

The surprising path that may end the war this year is when one party succeeds in subjugating the other. (Prudent Investor, 2023)

Will the outcome of the US elections alter their incumbent foreign policy framework?

II. Year of the Dragon: Eve of the Great Depression and the Year of the Dotcom Bubble Bust

It is not just about geopolitics. The Year of Dragon played a pivotal role in ushering in economic eras.

1928 (Year of the Dragon) represented the climax, the inflection point, or the eve of the Great Depression of 1929.

2000 also saw the implosion of the Dotcom bubble.

Figure 1

Today, while global debt spirals into unprecedented heights, the leveraged speculative asset bubbles have intensified. (Figure 1, upper chart)

For the first time, global asset bubbles have conjointly been inflating spurring mania in AI, FANG, and meme stocks, cryptos, and several national equity benchmarks have morphed into the "everything bubble," anchored on hopes of support from credit easing policies by central banks. (Figure 2, lower graph)

These are symptoms of the worsening monetary disorder.

So, if history should rhyme, and if the zeitgeist of this Chinese horoscope prevails, the Year of the Dragon could showcase either an implosion of this massively inflating bubble or see its culmination.

III. Year of the Dragon’s Impact on the Philippines: GDP and CPI

How did the Philippines do under the previous Year of the Dragon?

Nota Bene: Because of the uniqueness of different periods, past performance does not guarantee future results.

Figure 2

In the Year of the Dragon, headline GDP fluctuated from a low of 3.4% in 1964—the year of the Wooden Dragon as today—to a high of 8.8% in 1976. The average GDP in the last 6 Dragon years was 6.04%. (Figure 2, upper chart)

The CPI helped shape the GDP. The dragon years captured the upside trend of the CPI cycle, which culminated with 13.9% in 1988, and equally the downside. (Figure 2, middle and lowest diagrams)

In the Wooden Dragon of 1964, the CPI was 7.3%. The average CPI of the last five dragon years was 8.06%.

IV. Year of the Dragon’s Impact on the Philippines: USD and the PSE

Figure 3

In the last four years of the dragon, the USD-Php increased in two and decreased in the other two. But because of the outsized 24% return of the end-of-the-year (BSP) quote in 2000, the average USD-Php payoff was 4.9%.

Figure 4

Domestic stock market returns have been volatile during the Year of the Dragon.

Caught with the bursting dotcom bubble, the PSEi 30 cratered by 30.3% in 2000 but soared by 21% in 1976 (pre-Presidential Referendum 1977) and 33% in 2012 (post-Great Recession and 2010 Philippine elections). Thus, the average 5-year return was 7%. Nonetheless, the PSEi 30 rose in four of the last five dragon years.

But when adjusted for inflation, the average 5-year "real" return was a deficit of 1.1% from the sharp plunge in "real" returns in 2000.

Despite a lower than the government target GDP in 2023, the PSEi 30 raced to a 6.2% return in the first six weeks of 2024 or on the eve of the Year of the Dragon.

Will global and domestic financial conditions remain favorable to the bulls?

Or will the "problem-solving" Dragon help inflate local and international asset bubbles to its climax?

____

References

Pippa Malmgren, WWIII: An Update for Taylor Swifties and Other "Mere Spectators”, Dr. Pippa’s Pen & Podcast, February 4, 2024

Prudent Investor Newsletter, What Surprise is in Store for the 2022 Year of the Water Tiger? January 23, 2022