Like all bubbles, it ends when the money runs out—Andy Kessler

In this issue:

The Philippines’ Top 5 Property Developers: 2023 and Q4 Performance: The Seen and Unseen

I. Top 5 Property Developers: Remarkable Headline Performance in 2023

II. 2023 Top 5 Property Developers: Beneath the Headlines, Soaring Debt, Interest Expense and Decaying Liquidity

III. Big Boys’ Club: Q4 2023’s Incredible Spike in Real Estate Sales!

IV. The Real Estate Sector’s Predicament: More Signs of Escalating Concentration and Other Risks

V. Slowing Consumers, Rising Risks of a Material Slowdown in Rental Revenues

VI. Rising Imbalances from Credit-Funded Real Estate Demand Amidst Rising Debt-Financed Supply

VII. How Inflation Benefited the Top 5 Developers and Why this is Unsustainable

VIII. The BSP’s Path Dependence: The Rescuing of Banks and the Property Sector

The Philippines’ Top 5 Property Developers: 2023 and Q4 Performance: The Seen and Unseen

The Philippines' top 5 real estate developers showed an impressive headline performance in 2023 and Q4. Beyond that, there are rising risks from multiple fronts.

I. Top 5 Property Developers: Remarkable Headline Performance in 2023

Here's a summary of the aggregate financial performance of the top 5 PSE-listed property developers—or the 'Big Boys Club' (BBC)—in 2023. The firms included are SM Prime Holdings [PSE: SMPH], Ayala Land [PSE: ALI], Megaworld [PSE: MEG], Robinsons Land [PSE: RLC] and Vista Land & Lifescape [PSE: VLL].

The headlines looked great!

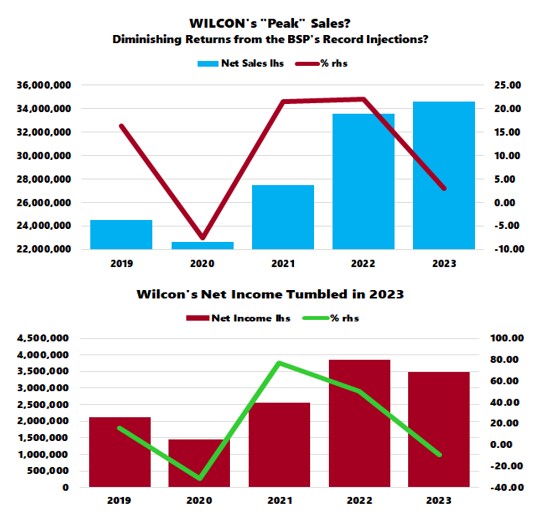

Figure 1

First. Despite a 15.4% increase to Php 422.7 billion, revenues remained lower than the 2019 record of Php 431.2 billion. (Figure 1 topmost pane)

Moreover, the pace of growth moderated from 19.9% in 2022 to 15.4% last year. SM Prime led the pack with a 21.09% growth rate, while RLC's 7.7% contraction pulled revenues lower.

Second. Real estate (RE) sales surged from 7.8% to 11.03% in 2023, driven by ALI and VLL's growth of 20.44% and 19.07%, respectively. It's important to note that ALI's RE sales included rental revenues. However, RE sales in pesos remained 12.8% below the 2019 peak. (Figure 1, second to the highest image)

But here’s the thing: since peaking in 2021, the share of RE revenues to the total plummeted to its lowest level in 2023, indicating that the bulk of the BBC’s revenues emanate from rent. (Figure 1, second to the lowest graph)

Third. While rental revenues represented the core, growth slowed from 51.5% to 20.7%. In pesos, rental revenues in 2023 reached an all-time high of Php 157.6 billion, surpassing the previous milestone of Php 133.43 billion set in 2019. (Figure 1, lowest chart)

Figure 2

Fourth. Net income reached a record of Php 112.9 billion, marking a brisk increase of 29.6% or a net gain of Php 25.8 billion. This marks the second consecutive year of 29% growth in 2023. VLL and SMPH posted the fastest growth, with increases of 39.2% and 32.92%, respectively. (Figure 2, topmost visual)

II. 2023 Top 5 Property Developers: Beneath the Headlines, Soaring Debt, Interest Expense and Decaying Liquidity

Fifth. The cumulative debt level surged to a record Php 950.5 billion, marking a 5.8% increase and reaching back-to-back record highs in pesos. (Figure 2, second to the highest window)

While the pace of increase was slower than income or revenue growth, it still grew by Php 52.31 billion, more than DOUBLE the income growth.

Ayala Land and SMPH, the two largest developers, saw the most significant peso gains of Php 22.215 billion and Php 14.3 billion, respectively.

Sixth. High-debt loans and elevated interest rates pushed financing costs higher. Interest expenses surged by 14.6%—the second-highest growth rate since 2018—to a historic Php 5.121 billion in 2023, representing the highest-level share of revenues at 1.21%. (Figure 2, second to the lowest graph)

Seventh and last.

The cash reserves of the Big Boys Club fell for a second consecutive year to their lowest level since 2018, dwindling to Php 90.4 billion. This represents the lowest level in the context of cash-to-debt and cash-to-interest payments since 2018. (Figure 2, lowest image)

With record net income and debt increases, why the plunge in the BBC’s liquidity conditions?

Are these companies overstating the headlines or understating the delinquencies?

That's the unseen segment behind the good news.

III. Big Boys’ Club: Q4 2023’s Incredible Spike in Real Estate Sales!

More to the point.

Another perspective is the performance on a quarterly basis. After all, the annual report signifies an accumulation of the four quarters. From here, we observe changes that led to the annual outcome.

Surprisingly, after slightly picking up in Q2 and Q3 compared to last year and Q1's slack, real estate sales spiked in Q4, both in peso (Php 78.8 billion) and in percentage (25.8% YoY).

However, it's important to note that ALI includes rent in its real estate revenues.

Figure 3

The record surge in RE sales (in pesos) powered total revenue growth (20.3% YoY) to a fresh record of Php 126.4 billion. (Figure 3, topmost chart)

Stunningly, the Q4 spike elevated the sales level of the Big Boys' Club, resulting in its higher share of Q4 (nominal) NGDP. (Figure 3, second to the highest image)

IV. The Real Estate Sector’s Predicament: More Signs of Escalating Concentration and Other Risks

Alternatively, if the Real Estate GDP estimates are accurate, the BBC accounted for 35.35%, which means that even with numerous competitors, the group continues to corner a larger share of the industry! Talk about the Big Boys getting Bigger! (Figure 3, second to the lowest diagram)

The Real Estate NGDP and Real Estate revenues seem to have parted in direction in Q4. (Figure 3, second to the lowest window)

With the spike in RE revenue growth and a 35% share, it's curious that the industry reported only an 8.7% growth rate (NGDP)—which likely indicates that the rest of the playing field experienced significantly below-average growth in Q4!

Or, has the BBCs cannibalized the markets of their lesser competitors, including the SMEs?

Importantly, it reveals the industry’s mounting concentration risks.

Figure 4

After all, the sector's declining contribution to real GDP, coupled with its increasing share of the bank lending portfolio, is symptomatic of credit-fueled overspending or malinvestments. (Figure 4, topmost chart)

Rising vacancies are just another sign of imbalances or supply-demand disorder.

Furthermore, given that the growth of the BSP’s real estate index materially slowed in Q4, this likely indicates a slowdown in speculative activities in the secondary markets, with the same activities shifting towards sales via the primary markets (property acquisition via developers). (Figure 4, middle picture)

It is important to point out too that the property sector and banks are closely intertwined or "joined at the hip." The property sector accounted for a significant share of Universal Commercial Bank loans: 23.8% of production loans, 21.1% of net RRPs loans, and 20.4% of gross RRPs loans. (Figure 4, lowest diagram)

That is to say, the industry’s decaying liquidity conditions and overreliance on leveraging to generate revenue and income growth are also manifestations of accruing imbalances.

V. Slowing Consumers, Rising Risks of a Material Slowdown in Rental Revenues

There’s more.

Risks are rising even in the industry’s core revenues: rental operations.

Figure 5

The decelerating cumulative revenue growth of listed non-construction retailers (SM Retail, Puregold, Robinsons Retail, SSI Group, Philippine Seven, and Metro Retail) mirrors the moderating growth of the BBC's rental revenues. (Figure 5, topmost window)

Since reaching its peak of 28.6% in Q2 2022—attributed to the BSP’s unprecedented injections and the ‘reopening’—year-over-year growth has steadily declined. The aggregate sales growth of the retail titans slowed further from 8.27% to 8.23% in Q4. (Figure 5, middle image)

Following the money trail, the slowing universal commercial bank credit growth rate has aligned with the BBC’s rent revenue growth. Credit growth has been indicative of the demand for rents.

By inference, rising rates would eventually exert pressure on rental revenues as vacancies increase due to retailers' faltering viability.

Such increasing divergence should amplify the exposure of malinvestments as unviable ventures.

VI. Rising Imbalances from Credit-Funded Real Estate Demand Amidst Rising Debt-Financed Supply

It's not just rent, but also the demand for real estate that has been anchored by bank credit expansion.

Therefore, it's unsurprising to see real estate (RE) revenues boosted by an upswing in the bank's consumer real estate credit growth.

The banking system’s real estate consumer loans grew by 7% in Q4 2024. However, its 38.4% share of consumer loans signifies the lowest since March 2020, as credit cards and salary loans have outperformed. (Figure 5, lowest diagram)

By the same token, unless productivity defines the character of the economy's development, the increasing credit-funded bets on the property sector would prove unsustainable.

Rising supply in the face of leveraged demand further magnifies its various financial and economic risks.

VII. How Inflation Benefited the Top 5 Developers and Why this is Unsustainable

That's not all.

Figure 6

The era of inflation has benefited property firms. Profit margins rose alongside the core CPI. Expanded profit margins have contributed immensely to the so-called 'bottom line,' supported by bank credit growth. (Figure 6, topmost and middle charts)

The fact of the matter is that the industry breathes in leverage, which drives the industry’s survival and expansion while providing less and less economic value added. (Figure 6, lowest graph)

The fiat money-based financial system requires ascending property prices to increase collateral values that buttress credit expansion. Therefore, policies have always been geared towards this process.

Unfortunately, diminishing returns plague the artificial boom from inflationism—where rising rates in response to inflation, malinvestments, and falling savings offset easy money policies.

VIII. The BSP’s Path Dependence: The Rescuing of Banks and the Property Sector

Ultimately, despite elevated inflation, the BSP will likely resort to its 'path dependence' of implementing an easy money regime when confronted with economic and financial risks.

It will likely deliver the 2020 bailout template, incorporating a mix of monetary policy rate cuts, direct and indirect liquidity injections (via financials), and revive, extend, and expand capital, regulatory, and operational relief measures.

On the other hand, political authorities will ramp up their fiscal tools, 'stabilizers,' where the political justification to increase defense spending will likely play a critical role in the coming series of 'stimulus.'

Deficit spending to GDP will hit new milestones.

The vent for all the series of political rescues of the elites will be vented on the exchange rate: the USD Peso.

Figure 7

Lastly, the recent market rout stock market rout has been led by the shares of the BBC.

If anything, the recent downshift in their share prices reinforces a massive "rounding top." (Figure 7)

Have share prices of the Big Boys' Club been showing the way?