To sum up, we are left with a paradox. Markets are liquid when they work both ways. Market participants, though, find themselves increasingly needing to move the same way. This is not only because of procyclical regulation; it is also because central banks have become a far larger driver of markets than was true in the past. The more liquidity the central banks add, the more they disrupt the natural heterogeneity of the market. On the way in, it has mostly proved possible to accommodate this, as investors have moved gradually, and their purchases have been offset by new issuance. The way out may not prove so easy; indeed, we are not sure there is any way out at all. –Matt King, Managing Director and Global Head of Credit Products Strategy, Citigroup Inc, Research Division

In this issue

Phisix 7,550: The Many Myths of the Falling Peso

-Sugarcoating the Falling Peso: The US Federal Reserve Scapegoat

-Sugarcoating the Falling Peso: Ignoring the Regional Dynamics

-Sugarcoating the Falling Peso: Ignoring the Growing Risks of an Asian Crisis 2.0

-Falling Peso Equals Slower Economy and Vice Versa

- The OFW as Embodiment of Policy Failure

-Philippine April PMIs: Media Says G-R-O-W-T-H, Regardless of Retail-Wholesale Crash!

-No Bubble? BSP 1Q 2015 Data Reveals Makati CBD Property Prices Skyrocketed by a Staggering 25%!!!

-China’s Stock Market Crashes 10% as Xi Jinping Put Mutates into the Frankenstein Stock Market

-PSEi 7,550: Market Internals Erode Again, Death Cross, and Seasonality (The Ghost Month Superstition)

Phisix 7,550: The Many Myths of the Falling Peso

The mainstream’s agitprop campaign on the weak peso has begun.

I predict that there will be imbecilic rationalizations where the weak peso will associated with more purchasing power from USD based OFW and BPO remittances. The coming rationalizations will omit the insight of the transmission mechanism of import prices into the system. It’s the kind of same nonsensical popular imputations that says low oil prices equals stronger consumption spending.

The peso, which fell by .54% to 45.74 to a US dollar, was a toast this week and so the spin.

From the Inquirer[2]: “The weak peso will provide a welcome boost to the Philippine economy, which grew by 5.2 percent in January to March, the slowest pace in three years. Last year, the economy expanded by 6.1 percent. Several of the Philippine economy’s major drivers are dollar-earning industries such as tourism and business process outsourcing (BPO). Remittances from overseas Filipino workers (OFW)—the biggest source of dollar income for the economy—accounted for nearly a tenth of domestic output.”

Sugarcoating the Falling Peso: The US Federal Reserve Scapegoat

If media really believe in what they are saying, then why not appeal to the authorities to make the peso a permanently weak currency as it has been in 45 years or from 1960 to 2005 (see left)?

Yet what has the devalued peso delivered then? Has prosperity from the boiling frog crash from Php 2 to a US dollar in 1960 to 2014’s Php 44.395 (left window) been achieved?

Since a weak peso supposedly should “boost” the economy then why not even push this to the extremes? Why not ask authorities to destroy the peso through hyperinflation ala Zimbabwe or presently Venezuela (right from Cato’s Troubled Currencies Project)! Perhaps these nations have found nirvana (or a nightmare as Venezuela)!

The swooning peso has been popularly imputed to expectations of an interest rate liftoff by the US Federal Reserve. But if the economy has truly been “sound” as popularly held, then the peso wouldn’t even fall. If the Fed tightens, then the BSP can match it. The BSP can even preempt the FED! So why the dilly dallying by the BSP?

Could it be because of too much credit issuance by the domestic banking system, or entrenched dependence on credit by the formal economy’s “too big to fail” institutions, have made the system’s balance sheets vulnerable to rate increases?

And could it also be because such actions would imply the end to the implicit subsidy to the Philippine government and to firms owned by politically connected elites?

And could it likewise be that all the previous FDIs and portfolio flows have mostly emerged from leveraged carry trades anchored on the Fed’s policies and the BSP’s (negative real rates) financial repression policies such that a tightening may send them stampeding out?

Or how about all of the above?

Media and their favored experts bloviate as if tourism, OFW remittance, BPOs or exports have been a standalone thing. They don’t seem to realize of the consequences from the actions by the Fed.

If the Fed tightens, then how will the global economy respond?

Yet it has not been the first time.

The Fed floated a trial balloon of withdrawing stimulus in May 2013. The consequence? Global financial markets went into turmoil. This episode has been known as the “taper tantrum”.

While the sustained easing by many central banks kicked the proverbial can down the road, continued balance sheet leveraging has been prompting for a shrinking liquidity dynamic on a global scale. The declining growth rate of global forex reserves has been a testament to this.

And liquidity strains have been compounded by monetary policies (QE) and bank regulations (Dodd Frank and Basel Accord).

The progressive reduction of liquidity can be seen unfolding through several phases and through feedback loops. Today they are seen as crashing commodity prices, floundering emerging markets, diminishing global trade, and finally, slowing advanced economies.

And to take the 2Q GDP in the context of two year performance, the Wall Street Journal exuded disappointment[3] (bold mine): “The economic expansion—already the worst on record since World War II—is weaker than previously thought, according to newly revised data. From 2012 through 2014, the economy grew at an all-too-familiar rate of 2% annually, according to three years of revised figures the Commerce Department released Thursday. That’s a 0.3 percentage point downgrade from prior estimates. The revisions were released concurrently with the government’s first estimate of second-quarter output. Since the recession ended in June 2009, the economy has advanced at a 2.2% annual pace through the end of last year. That’s more than a half-percentage point worse than the next-weakest expansion of the past 70 years, the one from 2001 through 2007. While there have been highs and lows in individual quarters, overall the economy has failed to break out of its roughly 2% pattern for six years.”

The following day, labor data was even more dismal. Wages and salaries reportedly grew by only .2% in 2Q, the slowest pace on record since Labor Department began tabulating them in 1982, according to Bloomberg. This followed a .7% increase in the first quarter.

The dampened labor outlook, which markets momentarily saw as a possible reason for another deferral by the FED to increase rates, sent the US dollar plummeting on Friday.

And in conjunction, along with currencies of ASEAN neighbors, on the news breakout, the peso sharply recovered to the Php 45.40+ levels. Unfortunately, the gains had been short lived as the US dollar scaled back to reclaim most of the day’s early losses.

So there could be some recovery by Asian currencies early next week. But I doubt if the rebound will last.

Yet two insights from the above.

One. The FED seems reluctant to pull the trigger.

The US FED is in a bind. Current string of economic data has not been as vigorous as expected. But the Fed will be left with limited traditional interest rate “tools” when signs of a significant downturn reemerge. So if the FED will increase rates, then it will likely do so conservatively. This will mostly be symbolical rather than intended as policy tightening.

Besides, last week’s FOMC statement exhibited indications that the Fed may be moving goalposts anew. The broader coverage of variables for policy assessment makes them look increasingly tentative.

Nonetheless, Friday’s wage and salaries data pulled back the probability of a rate hike in September, from 100% in Thursday to 88% on Friday as seen in the CME Groups’ Fed Futures. Perhaps this coming Friday’s non farm payroll may determine their actions.

Moreover, during the 2013 taper tantrum, yields of 10 year treasuries soared to almost 3% as against last Friday where the same notes yielded at 2.2%. The treasury markets hardly seem convinced that the Fed will meaningfully tighten.

To consider, all these has been happening even when the FED balance sheet still drifts at record highs ($4.5 trillion). Additionally, the total assets of major central banks (FED, ECB, BOJ, PBOC) has been estimated at a record $14.4 trillion. This account for a stunning 18.5% of global GDP (2014)!

In short, fantastic amounts of central bank stimulus have repeatedly been injected into the system, yet the global economy has been foundering.

Besides, a 25 bps hike seems all so problematic for the FED. Why?

Sugarcoating the Falling Peso: Ignoring the Regional Dynamics

This leads as to the second insight.

USD based revenues of tourism, exports, OFW remittances and BPOs all DEPEND on global economic conditions. Should the FED’s actions worsen global economic conditions, then NO amount of devaluation will boost these industries.

Remember, tumbling currencies have not been exclusive for the Philippines. With the exception of China, the entire region has almost been afflicted.

While pressures on regional currencies have emerged in 2013, this has become conspicuous over the last month or so.

The silent run on the rupiah, as well as the ringgit, remains unflinching. While the Taiwan dollar was last week’s biggest loser, the rupiah and ringgit continues to hemorrhage profusely. Apparently the strengthening of the US dollar continues to spread and intensify throughout the region.

In Thailand, growth in non-performing loans (+15.5%) in the nation’s top four banks continues vastly outpace and surpass bank profits (+1.6) and lending growth (1.6%) last June according to Nikkei Asian Review.

Now the question is how much more losses on domestic currencies can be tolerated before a financial blowup occurs?

But any risks (or costs), according to the mainstream, should be ignored. Just focus on the (superficial) benefits.

Forget about how currencies affect real economy prices and therefore the production process, investments and consumption, interest rates or debt.

This means that the frail currencies are good news for the entire region. Based on the economic shaman’s logic, except for China, because the region’s currencies have been weak, then all of them should economically flourish!

Yet, the more anemic the currency, the stronger the economy!

Sugarcoating the Falling Peso: Ignoring the Growing Risks of an Asian Crisis 2.0

Forget too that tanking currencies could be symptoms of an emerging financial crisis.

A currency crash is technically defined as an annual depreciation (devaluation) greater than or equal to 15 percent per annum[4]. So the rupiah and the ringgit, as of Friday, have been more than halfway there. Large exposure by domestic banks on debts outstanding denominated in foreign currency may “lead to a banking cum currency crisis” (Reinhart Rogoff)

Besides, the leading indicators of a currency crisis, according to the ECB[5], include rising money market rates, worsening government balances, and falling central bank reserves.

Not only has the trend of the growth rate foreign exchange reserves by central banks of emerging markets been on a decline since the apex in 2009, they have been in contraction in 2015.

The IIF observed last week[6] (bold added): One reflection of these strains can be seen in the very sharp and unusual decline in EM FX reserves in recent quarters (Chart 1.2). While China accounts for about 50% of the total, reserves in other EM countries have also been under pressure: Malaysia, for example, which has been intervening to support the ringgit amid political strains, has seen FX reserves drop close to levels last seen during the 2008-09 financial crisis. Russia’s reserves, at just over $360 billion, are at levels last seen in 2007.

So the run in Malaysia’s ringgit could have been deeper. The Malaysian government has depleted a little over 30% of her forex currency reserve (as of June) to defend the ringgit. Yet the plummeting currency has been adding strains to Malaysia’s burgeoning external debt, which presently accounts for 53.11% of her GDP according to National Debt Clock. Should a slowdown in Malaysia’s annual GDP persist, then the debt and interest rate ratios will soar! Curiously this has been happening even as Malaysia’s trade balance and current account has been positive.

The popular wisdom of the strengths “macro” statistics is being tested. And my bet is that popular wisdom will fail.

Interestingly it is not just Malaysia. While Philippine media sells platitude that everything remains copacetic, elsewhere in the Emerging Market world, central bankers have become increasingly nervous. The Bloomberg notes that “the selloff” in currencies of emerging markets “has become so swift and so deep that officials are abandoning hands-off policies on concern the drop will fuel inflation, deter investment from foreigners and act as a drag on their economies at a time when global growth is already decelerating. To counter the declines, policy makers from Mexico to South Africa and Turkey have either stepped up intervention, increased interest rates or signaled an end to monetary easing”[7]

You see, the problem has not just been about falling currencies, but also about the scale of volatility from the recent declines.

The emerging market forex reserves chart and current developments reminds me of the “deficit without tears” from the US dollar standard.

Since the Nixon Shock in August 15, 1971, the US has been exporting inflationism via paper dollars and dollar denominated debt and other financial instruments to the world in exchange for goods and services.

Emerging markets, on the other hand, who wanted to keep their currency from rising, to benefit from global financialization, stacked up on those dollars (forex reserves) in exchange for the printing of domestic currencies. This became pronounced when Fed Chairman Greenspan unleashed his string of bailouts, most notably during the dotcom crash.

Nonetheless such policies has led to bubbles everywhere.

And such bubbles have been epitomized by excess capacity that had been financed by cheap credit. Now excess capacity has translated into crashing prices. Along with the increasing onus of debt, excess capacity has served to restrain on economic activities.

French economist Jacques Rueff[8] once warned of the US dollar standard’s “deficit without tears” in stating that this “allowed the countries in possession of a currency benefiting from international prestige to give without taking, to lend without borrowing, and to acquire without paying. The discovery of this secret profoundly modified the psychology of nations. It allowed countries lucky enough to have a boomerang currency to disregard the internal consequences that would have resulted from a balance-of-payments deficit under the gold standard”

Well that “internal consequences that would have resulted from a balance-of-payments deficit” have now come home to roost. Chronic maladjustments has surfaced as collapsing prices of commodities, soaring US dollar, strained emerging market economies, slowing global trade, declining forex reserves, signs of a slowdown in advanced economies and innate strains in financial market (as China).

It’s the periphery to the core phenomenon dynamic in progress and accelerating.

The phase of this cycle will flow from economic slowdown to financial losses to cash flow problems to debt servicing problems to constrictions on access to credit, to insolvency and finally to liquidations.

And what more if the US Federal Reserve does tighten.

Yet no amount of brainwashing will change this.

Falling Peso Equals Slower Economy and Vice Versa

Devaluations hardly perform as famously advertised.

The peso as represents a price that has real economy effects. As I noted last week[9],

A falling peso isn’t legislated. A falling peso also doesn’t emerge out of metaphysical or supernatural causes. Instead, a falling peso is a product of human action. A basic explanation: demand for the USD is GREATER than the demand for the peso.

A greater demand for the USD means that there will be LESS incentive to HOLD onto Philippine peso assets (whether bonds, currency, stocks or property). There will also be LESS incentive to invest in peso. This applies to whether demand emanates from resident, nonresident or currency speculators…

Furthermore, given the sharp volatility in the currency, how will this impact the entrepreneur’s economic calculation? Falling peso means more pesos required to buy foreign goods or higher local prices of foreign goods.

If the pesos’ fall has been gradual or can be anticipated, then importers may have some leeway to assess if they can pass the price increases to consumers, or if they will merely shoulder the profit squeeze.

But what of the sharp volatility in the exchange rate? How will importers determine the profit and losses and the market’s ability to absorb imported supply? So what does the importer do? Here’s a guess. They will likely try to secure currency forwards from banks to hedge their imports or they could REDUCE imports

The peso’s impact to the statistical economy can be seen below

The peso-annual GDP growth shows of meaningful correlations.

One can divide the chart above into two epochs: the post Asian crisis and the post Great Financial crisis (GFC).

In the wake of the Asian crisis, the peso (upper window) continued to decline in the face of post crisis adjustment…and that’s until 2005.

However, in between there had been countervailing trends.

For instance, the peso rallied in 2002 to mid-2003, Philippine GDP picked up over the same period.

The peso resumed its decline by mid 2003, but the rate of decline has sharply decelerated until its inflection point in 2005. From then, the peso rallied strongly.

Over the same period, except for the odd 2004 spike which apparently had been smoothened out by an equally steep decline in economic growth in the next quarters, the pesos’ turnaround essentially coincided with an acceleration of the GDP from 2005 to 2007.

Then GFC appeared which caused the GDP to collapse from 2007 to 2009. The peso appreciated at the onset of the GDP slowdown. It was only by early 2008 when the peso commenced to deteriorate as the statistical economy sustained its downtrend.

However, the USD peaked or the peso hit a trough ahead of the GDP.

From 2009 to 2013, the peso confirmed on the GDP’s ascent.

Since 2013, the gradual weakening of the peso coincided with the slowing tempo of the statistical economy.

Post GFC, the correlation between the USD peso (USDphp) and GDP has been more pronounced than during post Asian crisis.

As pointed above, losses of Asian currencies have been intensifying. And so with the peso.

Theory and empirics on tells us that mainstream projections (or propaganda) will badly miss on their estimates.

The OFW as Embodiment of Policy Failure

Curiously, the OFW leftist group Migrante International downplayed the Philippine president’s latest SONA in stating that OFW growth hallmarked a policy failure. That’s because OFW growth has been prompted by “prevailing high unemployment rate and low wages in the Philippines”

The group cited data from Philippine Overseas Employment Administration (POEA), where average daily deployment of Filipino workers rose from 4,018 in 2010 to 4,624 in 2011 and to 4,937 in 2012. Likewise, in 2013, the POEA posted an average of 5,031 daily deployment and the figure went up to 5,054 a year ago.

On the other hand, the group noted that employment data based on the Philippine Statistics Authority (PSA) showed that the number of locally employed Filipinos was only 1.02 million in 2014, or an average of 2,805 additional employed in the country daily.

Thus the group declared, “the Aquino administration breached the two million mark in overseas Filipino worker (OFW) deployment processing in 2013, the highest in history of Philippine migration”[10]

Thus, whatever boom that has been published has been a boom in the economic interests of politically connected elites and of the government.

Headline booms have hardly been about the general economy but of the feel good justifications of invisible redistributive policies.

As I have been saying here, OFWs are symptomatic of the severe LACK of economic opportunities. Most of such opportunities have been corralled by these elites.

Yet the more the peso falls, the greater the inclination for the unprivileged sectors to look for ‘green pasture’ opportunities abroad.

From 1960s to the present, the boiling frog collapse of the peso has only produced “people” exports.

So much for the façade of headline credit fueled booms.

Philippine April PMIs: Media Says G-R-O-W-T-H, Regardless of Retail-Wholesale Crash!

As always, the spin has been about G-R-O-W-T-H, but media admits to a much reduced levels

The BSP provides a fascinating data on April PMIs.

The consolidated April PMI of services, manufacturing, and retail and wholesale trade came at an estimated at 57.1 points in April, down from March’s 58.6 points.

The breakdown includes Manufacturing at 52.2 from March’s 54.9. Wow. Manufacturing seems headed for a contraction.

The service sector was the strongest at 59.9.

But here’s the zinger. From the inquirer (bold mine), “The weakest performers in April were retailers and wholesalers. The sub-sector’s PMI significantly declined to 53.7 in April 2015 from 60.5 the month before. All the tracking variables—purchases, sales revenues, employment, supplier deliveries, and inventories—expanded at a slower rate from their month-ago levels. “Both the retail and wholesale sub-sectors slowed down in April, which could be attributed to sluggish activities during the Holy Week,” the BSP said.”[11]

More Wow! That’s a whopping 11.23% crash in retail-wholesale activities! Yet the crash in the said sector has been broad based!

The BSP claims that the slowdown in retail activities must be due to the Holy Week. Really now??? Going to church makes people spend less? Or has it been that there has been less income to spend even during holidays??? The BSP should have cited if this has been seasonal (every Holy Week of each year) or a deviation. Instead, they came up with a bumbling alibi.

Even more, perhaps the BSP failed to look at the NSCB’s retail growth trends. The NSCB’s 1Q GDP 2015 shows of a general decreasing trend on retail activities since 2Q 2013. While 1Q 2015 supposedly showed a bounce, this comes a considerable number of store vacancies at shopping malls surfaced.

Yet if the April PMI gets included on 2Q GDP, then this could imply that the 1Q rebound has faded anew.

Another irony, part of the service sector should reflect on retail activities, then why the glaring disparity?

Given the “significant decline” in retail and wholesale, what happens now to the race to build major malls, strip malls, and other retail spaces? Perhaps ghost buyers will emerge?

No Bubble? BSP 1Q 2015 Data Reveals Makati CBD Property Prices Skyrocketed by a Staggering 25%!!!

The mainstream has repeatedly been in massive denial over the existence of bubbles. Yet here’s a stunner from the Inquirer[12]:

The price of land at Makati’s central business district (CBD) rose by more than a quarter over the past year to match in nominal terms the record-highs reached before the 1997 crash, the Bangko Sentral ng Pilipinas (BSP) said. In a report, the BSP said land values in Makati City, the country’s economic center, rose by 25.4 percent year-on-year to reach P443,750 per square meter at the end of March 2015. Quarter-on-quarter, implied prices were up 0.9 percent. Similarly, implied values in the Ortigas Center rose by 1.9 percent quarter-on-quarter and 10.3 percent year-on-year to P161,500 per sqm of land, the BSP said, citing data from consulting firm Colliers International.

Let us put into perspective what a 25.4% surge in property prices for the Makati CBD means.

If the Philippines grew by 6.5% a year then Makati CBD’s property growth rates implies 3.91 years of growth compressed into in a year in the 1Q 2015!

Yet ironically, 1Q statistical GDP was only at 5.2%!

Meanwhile banking loan growth to the economy has been on a downtrend since July 2013, yet the growth rates have been above 10%. 1Q 2015 hardly posted any recovery.

In June 2015, bank loans to the general economy eked higher to 14.5% from 14.2% in May according to the BSP.

Domestic liquidity in the 1Q 2015 recoiled off from a crash following 10 consecutive months of 30%+++ money supply growth.

In June, domestic liquidity sputtered again. M3 growth rates slipped to 9% from 9.3% in May. But here is the kicker: month on month M3 decreased by 0.3 percent (seasonally-adjusted basis) according to the BSP

June CPI sagged further to 1.2% also based on BSP data. (right window)

Bank loan growth, money supply growth and CPI have been in a chorus. They seem to be confirming the Philippine economy’s ongoing contraction of systemic liquidity. Add to this the flattening of the yield curve.

Even worse, they highlight on incipient indications of monetary deflation!

But in the 1Q, concomitantly with 1q real estate, the PSEi was pushed to a string of record highs.

In other words, while the statistical economy, and most likely, the real economy have materially been slowing, the toys for the big boys have become the object of intense speculative actions.

It is perhaps a reason why prices on the general economy have been on a downfall as rampant speculations on asset markets have substituted real economy investments and consumption activities in 1Q 1015.

Interesting, because the data above emanates from the BSP’s own report, as indicated by the Inquirer. Yet the BSP seems utterly blind on how all these manic speculations have been funded.

And bizarrely, the BSP continues to dish out NPL ratios (Universal Commercial banks and thrift banks) which because of still soaring prices conceals on the widespread malinvestments.

NPLs will become an issue once real estate and stock prices slump.

China’s Stock Market Crashes 10% as Xi Jinping Put Mutates into the Frankenstein Stock Market

All that PBoC backed mind blowing $800 billion firepower, forced buying by state owned companies, capital controls (prohibition of selling by major investors), interest rate easing, PBoC injections, censorship, demonization of short sellers and of foreigners have gone to naught as the Shanghai Index crashed 10% anew over the week.

But again this won’t stop the Chinese version of tainted version of the legendary King Canute.

The Chinese government’s war against sellers has only intensified.

Nikkei Asia reports of the suspension of trading at 24 brokerage accounts, including that of a subsidiary of U.S. hedge fund and high frequency trader Citadel. Part of the suspension of the said accounts has been due to the Chinese government’s expanded list of targets to include spoofing, according to Bloomberg.

The CNBC reports that the Chinese futures regulator will tighten rules governing trading that it regards as "irregular" to tackle what it sees as excessive speculation in the markets

Apparently any speculation that sees rising overvalued stocks are ok, but not dropping stocks.

The China Securities Regulatory Commission will also tighten censorship of mostly local media. The CSRC said that “Speculative reports…must first be confirmed by the CSRC in order to prevent the spread of false information and market disturbance.” (FT)

The Chinese government has extended their investigation on sellers overseas. They are pressing “foreign and Chinese-owned brokerages in Hong Kong and Singapore to hand over stock trading records, sources said, extending its pursuit of "malicious" short sellers of Chinese stocks to overseas jurisdictions” according to Reuters.

Chinese insurers have been asked to refrain from selling equities, according to Zero Hedge. Chinese insurers have bought stocks and stock mutual funds worth 110 billion rmb according to SCMP’s George Chen.

Since markets are about exchanges or buying and selling, if one of the main function is banned, or severely regulated or impaired through the arbitrary interferences by politicians, who determine and impose on the price levels, then markets do not exist at all. Liquidity will practically shrink, if not evaporate. People’s resources will get stuck into assets that have no exit mechanism. So Xi Jinping Put will mutate into a Frankenstein market.

Capital controls not only inhibits movements or confiscates people’s properties, they reduce the economy’s access to capital.

Yet if the ‘war against sellers’ fails, which will be manifested through sustained downfall of Chinese stocks, then the Chinese government may likely declare a stock market holiday.

It’s pretty odd for the “stability obsessed” Chinese government to panic. I know that there are lots possible nasty economic and social consequences for a continuing crash which risks leading to a financial crisis. But the Chinese government’s own actions have been another major source of the uncertainty, which consequently could a cause for panic.

Worst, unintended consequences have appeared. Pork prices have been soaring (Nikkei Asia). Perhaps this may partly be a stock market related supply side factor constraint. Farmers who gambled and lost in the stock market through margin debt may have lost all resources to replenish stocks of pigs. Reduced supply of pigs may have led to shortages thus, rising prices. Add to these all those PBoC pumps on the system which may have increased demand pressures on pork.

Yet if Chinese inflation starts to surge, then all those stock market-property and real economy rescues will most likely grind to a halt.

PSEi 7,550: Market Internals Erode Again, Death Cross, and Seasonality (The Ghost Month Superstition)

The PSEi lost 1.51% over the week.

The losses would have been larger save for Friday’s last minute marking the close pump which delivered a stupendous 100% of the day’s gains!

With an incredible four days of session end weakness, perhaps index managers wanted recognition of their presence.

Over the month, the Philippine benchmark has been hardly changed (down by .19%)

This week’s selloff only affirmed my suspicions that the broad based rebound two weeks ago was nothing more than a severe oversold bounce.

Losing issues regained dominance with a substantial 158 margin. Losing issues gained the upper hand in 4 out of the 5 trading days even when the PSEi closed up in 3 days.

Of the 30 issues within the PSEi basket, 6 posted gains as against 24 decliners.

Bears seem as closing in for supremacy even in the PSEi basket which has been a bastion of the index managers.

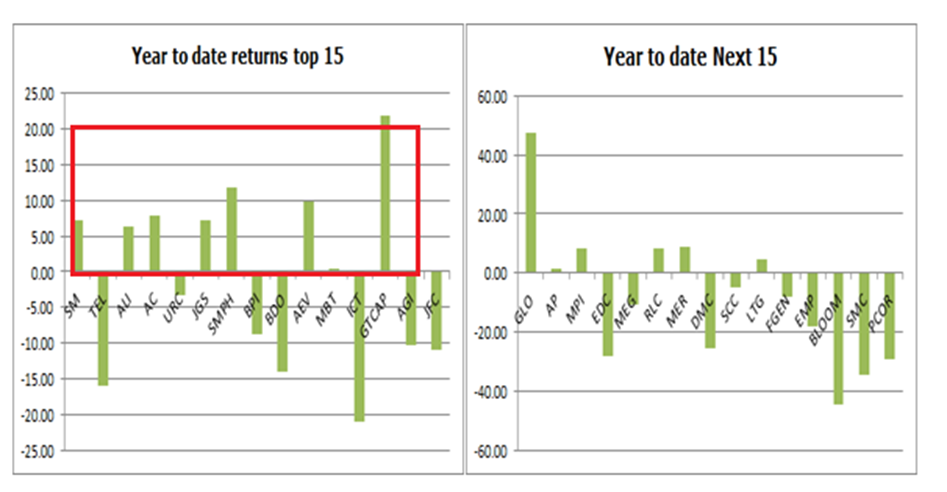

Except for record high SMPH which has become the main issue to keep the PSEi from falling apart, 5 among top 15 biggest market cap issues seem as clinging for dear life. One is already part of the bears.

Yet any sustained selling will likely bring them to the fatal embrace of the bears.

Index managers would have to muster more volume to stave off the bear’s coming onslaught.

Moreover, sustained low volume and lethargic total number of trades evinces of the Philippine equity market’s shrinking liquidity.

Curiously, banking issue have become sudden candidates to bear’s membership role. BDO’s weekly 4.29% rout was prompted by market’s frustration over the 6% earnings growth during the 1H of 2015.

Here is a notable segment from BDO’s earnings news. From the ABS-CBN (bold mine)[13]: “BDO also said it sustained momentum in its core lending, and its deposit-taking businesses yielded a net interest income growth of 10 percent, which was tempered by the prevailing liquidity in the system.”

Gotcha!

The transmission effects of the flattening yield curve have now become apparent in the banking system’s loan portfolio, and subsequently, to earnings!

While BSP credit to the banking system continues to grow at above 10%, they have been declining. The 10+% growth still provides the income to the banking system’s core lending operations. But this room has been narrowing. BDO admits to this.

With economic G-R-O-W-T-H pulling back, growth in the banking system’s loan portfolio should slowdown. Even more, decelerating economic G-R-O-W-T-H and/or a downshift in the growth of the banking system’s loan portfolio will INCREASE NPLs. (Pls see Thailand experience above)

The banking system is the heart of the Philippine financial system. And bank credit serves as the lifeblood to the current economic G-R-O-W-T-H paradigm. Hence, a slowdown in the banking system will percolate to the rest of the economy.

So funding for index managers could likely be in peril. No funding, no manipulation.

Let me add that I believe there are a lot of skeletons in many of the banking and financial system’s accounting closet. The recent DBP market manipulation exposé, which had been intended to hide financial losses, shows the way.

Furthermore, Japan’s Toshiba’s accounting scandal also exhibits the likelihood that many books of non-financial have likely been cooked—perhaps in a variant from the Toshiba way.

Soaring US dollar (faltering peso) have in the past been a drag on the stock market. That’s unless we are going to see hyperinflation ala Venezuela or Argentina.

The logic is once again simple: greater demand for US dollar means less demand for Philippine assets. Philippine assets include stocks. So lesser demand at extremely overvalued pricing levels translates to greater risks for a downside move.

That’s aside from the price function of a falling currency to the economy and to earnings as noted above.

It’s why stocks of our ASEAN peers have all been struggling.

I’m not a believer in charts as charts can be engineered as recently demonstrated by the index managers.

Nonetheless with so many followers spanning institutions and retail, I have to keep an eye on them.

What does the present PSEi chart say?

Well, momentum suggests that a DEATH CROSS is imminent. That’s why index managers have to work doubly hard next week. They have to produce massive upside moves to whiplash this seminal bearish sentiment.

Otherwise, the death cross may spark an avalanche of selling by practitioners of charts.

The last time the death cross appeared was in the heat of the selling spree sparked by the taper tantrum in August 2013. It took about 7 months to reverse the bearish sentiment.

A death cross may mean the closure of the bull market.

Finally we are entering a season considered as hostile to stocks.

The BSP incredibly incorporated the Ghost Month in their ‘economic’ data and analysis as I pointed out here.

Yet through 30 years of August, 19 or 63.33% posted losses while 11 or 36.67% registered gains (see left-red are bear markets, green are bull markets and blue are market top). August losses have no trend specificity, they appear just about everywhere.

But again it doesn’t mean that the historical probability of in favor of losses implies losses are certain. That would be a gambler’s fallacy.

Instead, current deterioration in economic fundamentals, diminishing systemic liquidity, dropping peso, corrosion of stock market internals to even chart ‘death cross’ momentum suggest that losses will likely happen if the markets see these factors as unsupportive of prices at current levels.

Of course, this also depends on how index managers will fare.

In closing, the preeminence of hidden bear market has not been restricted to Philippine stocks.

Most of the world stocks based on the MSCI World Index seem to bear the cross of spreading bear markets.

The perceptive Gavekal Team enumerates the numbers: US 21%, Canada 68%, Hong Kong 30%, Singapore 29%, Brazil 82% China 82%, Indonesia 77% and Russia 81%

.png){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

.png){kind=link}

.png){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}