Devaluation is not a tool for exports. It is a tool for cronyism and always ends with the demise of the currency as a valuable reserve—Daniel Lacalle

In this issue

Is the Philippine Peso’s

Rise a Secret Bargaining Chip in Trump’s Trade War?

I. BSP Denies Currency

Manipulation Amid Trade Talks

II The Mar-a-Lago

Framework: Dollar Devaluation as Trade Strategy

III. Asian Geopolitical

Allies Lead Currency Appreciation Against USD

IV. Market Signals Point

to Implicit Bilateral Deals

V. Taiwan’s Hedging

Frenzy: Collateral Damage of FX Realignment?

VI Gross International

Reserves Tell a Different Story

VII. Breaking Historical

Patterns: GIR Decline Amid Peso Strength

VIII. Yield Spreads and

Market Disruptions Signal Intervention

IX. Conclusion: The Hidden Costs of Currency Leverage; Intertemporal Risks and Economic Feedback Loops

Is the Philippine Peso’s Rise a Secret Bargaining Chip in Trump’s Trade War?

How the BSP's currency interventions may be hiding an implicit trade deal with Washington

I. BSP Denies Currency Manipulation Amid Trade Talks

From a syndicated Reuters news, the Interaksyon reported May 20: "The Philippine central bank said there is no indication that its management of the peso’s exchange rate is part of trade negotiations with the U.S. government, as it signalled a preference for non-interest rate tools to manage capital inflows. The Bangko Sentral ng Pilipinas said while it expected to further ease monetary policy because of a favourable inflation outlook, it favoured a more nuanced approach to managing liquidity and exchange rate volatility. “The BSP does not normally respond to capital flow surges or outflows, or even volatility, using policy interest rate action,” the BSP said in an emailed response to questions from Reuters. Philippine officials met U.S. authorities on May 2 to discuss trade. Although not directly involved in the talks, the BSP said there was no indication foreign exchange considerations were explicitly part of the negotiations. The Philippines has not been spared from President Trump’s tariffs, although it faces a comparatively modest 17% tariff, lower than regional neighbours Malaysia, Thailand, Indonesia, and Vietnam. “The BSP adopts a pragmatic approach in managing capital flow volatility, combining FX interventions when necessary, the strategic use of the country’s foreign exchange reserve buffer, and macroprudential measures,” it said." (bold added)

II The Mar-a-Lago Framework: Dollar Devaluation as Trade Strategy

Though the Mar-a-Lago Accord, coined by analysts like Zoltan Pozsar and popularized by Stephen Miran, is a speculative framework, it draws inspiration from the 1985 Plaza Accord, where G5 nations coordinated to depreciate the U.S. dollar to boost American exports. Stephen Miran, now Chairman of the White House Council of Economic Advisers, published a paper in November 2024 titled ‘A User’s Guide to Restructuring the Global Trading System.’

It argues that the U.S. dollar’s persistent overvaluation harms American manufacturing by making exports less competitive and imports cheaper, contributing to a $1.2 trillion trade deficit in 2024.

To address this, Miran proposed devaluing the dollar by encouraging foreign central banks to sell dollar assets or adjust monetary policies, while using tariffs as a ‘stick’ to pressure trading partners into currency adjustments or trade concessions.

While dedollarization—reducing reliance on the dollar in global trade and reserves—is often cited as the cause of recent dollar weakness, this may apply to countries with geopolitical tensions with the U.S., such as China or Russia or other members of the BRICs.

However, it doesn’t explain the currency strength among staunch U.S. allies like the Philippines, Japan, and South Korea, suggesting a different motive: implicit negotiations with the Trump administration.

III. Asian Geopolitical

Allies Lead Currency Appreciation Against USD

Figure 1

Year to June 13, 2025, the USD dropped against 8 of 10 Bloomberg-quoted Asian currencies, led by USDTWD (Taiwan dollar) -9.9%, USDKRW (Korean won) -7.8%, and USDJPY (Japanese yen) -8.35%. (Figure 1, topmost and middle charts)

These countries, staunch U.S. allies that host American military bases, are the most likely to accommodate Washington’s demands.

In ASEAN, major currencies appreciated more modestly: USDMYR (Malaysian ringgit) fell 5.05%, USDTHB (Thai baht) 5.49%, and USDPHP (Philippine peso) 2.8%.

In contrast, USDIDR (Indonesian rupiah) rose 1.06%, indicating rupiah weakening—likely due to Indonesia's neutral stance, persistent fiscal concerns, and weaker ties to the U.S.

IV. Market Signals Point to Implicit Bilateral Deals

On May 23, MUFG commented: "Markets have seemingly perceived that President Trump is looking for a weaker US dollar versus several Asian currencies as part of bilateral trade negotiations. Bloomberg News recently reported that the Taiwanese authorities had allowed the TWD to appreciate sharply earlier this month. The deputy governor of CBC has said that this strategic move is to allow market expectations for TWD gains to play out. But this is apparently at odds with the Taiwan central bank’s past preference to intervene in the FX market to smooth out volatility. The Korean won has also advanced sharply on the news that the US-South Korea finished the second technical discussions on 22 May." (bold added) (Figure 1, lowest graph)

This MUFG insight—"A weaker US dollar versus several Asian currencies as part of bilateral trade negotiations"—suggests an implicit bilateral Mar-a-Lago deal.

V. Taiwan’s Hedging

Frenzy: Collateral Damage of FX Realignment?

Notably, Taiwan’s insurers recently suffered massive losses during the USD selloff and may have even contributed to it. Taiwan’s Financial Supervisory Commission (FSC) summoned insurers for reportedly “rushing to hedge their US bond holdings.” This could reflect unintended effects of TWD appreciation, potentially tied to an implicit Mar-a-Lago deal.

In a nutshell, it’s likely no coincidence that currency appreciation aligns with the U.S.’s closest allies, suggesting implicit bilateral Mar-a-Lago deals driven by Trump’s tariff leverage, despite official denials.

VI Gross International Reserves Tell a Different Story

"Never believe anything in politics until it is officially denied"—Ottoman Bismark

Taiwan’s central bank’s denial of involvement closely mirrors that of the Bangko Sentral ng Pilipinas (BSP).

The BSP has washed its hands from using the peso as a tool for negotiation, despite the Philippines status as a client state in ASEAN, bound by the 1951 Mutual Defense Treaty and hosting U.S. military bases.

Given the Mar-a-Lago framework of coupling dollar devaluation with tariffs, trade negotiations with the U.S. would likely involve the BSP, making its denial implausible.

While no official agreement exists, the BSP noted it could use a combination of “FX interventions when necessary” and “the strategic use of the country’s foreign exchange reserve buffer” for capital flows management.

This rhetoric suggests using the Philippine peso as strategic leverage for trade negotiations, aligning with the Mar-a-Lago goal of weakening the dollar to reduce the U.S.$1.2 trillion trade deficit, including the Philippines’ $5 billion surplus from $14.2 billion in exports.

VII. Breaking Historical Patterns: GIR Decline Amid Peso Strength

Figure 2

Consider the evidence: When the USDPHP fell in 2012 and 2018, the increase BSP’s Gross International Reserves (GIR) accelerated, evidenced by aggregated monthly inflows.

As a side note, May’s GIR saw a marginal increase, supported ironically by gold, which has served as an anchor. (Figure 2, topmost and middle images)

Recall that last February, the BSP dismissed gold’s role, citing the "dead asset" logic: Gold prices can be volatile, earn little interest, and incur storage costs, so central banks prefer not to hold excessive amounts." Divine justice?

Yet ironically, unlike past trends, the current USDPHP decline has led to a reduction in the GIR. (Figure 2, lowest visual)

The BSP’s template, repeated in January, March, and April, states: "The month-on-month decrease in the GIR level reflected mainly the (1) national government’s (NG) drawdowns on its foreign currency deposits with the Bangko Sentral ng Pilipinas (BSP) to meet its external debt obligations and pay for its various expenditures, and (2) BSP’s net foreign exchange operations."

The USDPHP remains far from the BSP’s ‘Maginot Line’ of Php 59—the upper band of its informal ‘soft-peg’ range—so why is its GIR eroding?

While part of the decline may be due to ‘revaluation effects’ from rising long-term U.S. Treasury yields (falling bond prices) and a softer dollar, this insufficiently explains the GIR’s decline amid an appreciating peso, contrary to historical patterns.

Figure 3

BSP data shows its net foreign assets contracted year-on-year in April 2025, the first decline since July 2023. (Figure 3, topmost diagram)

This partly reflects changes in the FX assets of Other Deposit Corporations (ODCs), but the primary driver has been the BSP’s dollar-denominated assets. (Figure 3, second to the highest pane)

Either we are seeing 'revaluation effects' from a GIR heavily weighted in USD assets—given that the BSP was the largest central bank gold seller in 2024, reducing its gold holdings to bolster reserves—or the BSP has been offloading some of its FX holdings to weaken the USD, thereby supporting the peso’s rise. It could be both, distinguished by scale.

VIII. Yield Spreads and Market Disruptions Signal Intervention

The spread between 10-year Philippine and U.S. Treasury yields has drifted to its widest since 2019, when BVAL rates replaced PDST in October 2018 as the benchmark for Philippine bonds. (Figure 3, second to the lowest and lowest graphs)

Historically, this was linked to deeper USDPHP declines, but since the BSP adopted its ‘soft-peg’ regime in 2022, its interventions have significantly reshaped this correlation—altering market signals and shifting currency allocations within the financial system

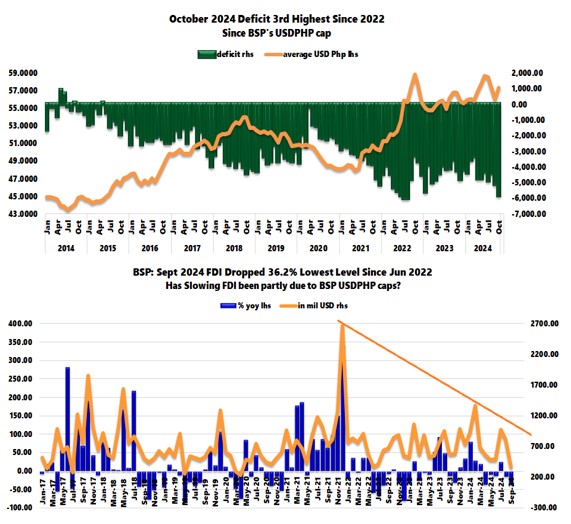

Figure 4

Weak organic FX revenues—contracting FDIs (-45.24% YoY Jan-Mar 2025), tourism (-0.82% Jan-Apr, including overseas Filipino visitors), March 2025 remittances at a 9-month low, and volatile portfolio flows ($923 million Jan-Apr)—don’t support the peso’s strength, except for services exports (+7.2% Q1 GDP). (Figure 4)

Insufficient FX flows explain the surge in external

debt, as the Philippines borrows heavily to bridge the gap, with external

debt increasing to support trade, fiscal needs, and the defense of the USDPHP

soft peg.

Figure 5

Philippine external debt surged by a staggering 14% in Q1 2025, driven by a 17.4% rise in public FX debt, which now accounts for approximately 59% of the total!

The BSP calls a sustained spike in FX debt 'manageable'—color us amazed!

IX. Conclusion: The Hidden Costs of Currency Leverage; Intertemporal Risks and Economic Feedback Loops

These factors strengthen the case that the BSP is using the peso as leverage for trade negotiations—an implicit bilateral Mar-a-Lago deal.

These interventions have intertemporal effects—or unintended consequences from pursuing short-term goals—that will likely surface over time.

The USD’s decline will likely accelerate FX-denominated borrowings, becoming more evident once the peso weakens—similar to the 2018 and 2022 episodes—amplifying currency, interest rate, and other risks through mismatches that could exacerbate market disruptions.

This poses risks of dislocations in sectors reliant on merchandise trade, remittances, or FX or USD fund flows, potentially triggering feedback loops that could negatively impact the broader economy or lead to economic and financial instability.

And with escalating risks of a fiscal shock—one that could trigger and amplify unforeseen ramifications—that would translate into a perfect storm, wouldn’t it?