The

shift to negative interest rates is all the more problematic. Given

persistent sluggish aggregate demand worldwide, a new set of risks is

introduced by penalizing banks for not making new loans. This is the

functional equivalent of promoting another surge of “zombie

lending” — the uneconomic loans made to insolvent Japanese

borrowers in the 1990s. Central banking, having lost its way, is in

crisis. Can the world economy be far behind?—Stephen S. Roach,

former chairman Morgan Stanley Asia and Senior Fellow at Yale

University

In

this issue:

Phisix

6,800: Shocking! BSP Hid Data of OFW Remittances as October and

November Monthly Reveals of CONTRACTIONs! PSE Censors 3Q Performance

of Listed Firms!

-Shocking!

BSP Revamps 2014-5 OFW Remittances Data, Concealed October and

November 2015 Massive Contractions!

-Negative

Numbers Spur PSE to CENSOR 3Q 2015 Performance of Listed Firms as

Philippine NGDP and PSE’s NGDP Goes on DIVERGENT Directions!

-Philippine

Bonds: The Fascist Crony Political Economy and The Escalation of the

Yield Curve Inversions!

-Robinson’s

Land Corp: Leveraging UP on a Vulnerable Topline

-Phisix

6,800: Global Central Banks Talk Up Risk Assets as Philippine Stocks

Approaches Overbought Conditions

Phisix

6,800: Shocking! BSP Hid Data of OFW Remittances as October and

November Monthly Reveals of CONTRACTIONs! PSE Censors 3Q Performance

of Listed Firms!

Shocking!

BSP Revamps 2014-5 OFW Remittances Data, Concealed October and

November 2015 Massive Contractions!

Just

what has been going on with the Philippine central bank, the Bangko

Sentral ng Pilipinas (BSP)?

Have

they been panicking over the state of OFW remittances?

The

BSP disclosed that they have reached their yearend target1:

“Personal remittances from overseas Filipinos (OFs) amounted to

US$2.7 billion in December 2015, posting a 4.9 percent growth

year-on-year. This is the highest monthly level recorded thus far.

Consequently, full-year personal remittances from OFs reached US$28.5

billion, higher by 4.4 percent than the previous year’s level and

exceeding the BSP’s projection of 4 percent for 2015”

That’s

nice unless one sees how the supposed target had been met, and

secondly, how the previous or original numbers had been glossed over

by the current (December) report.

You

see, the numbers for the November data in the December report had

been different from the November report. Here’s the disclosure:

“Personal

remittances from overseas Filipinos (OFs) amounted to US$2.4 billion

in November 2015, representing a year-on-year growth of 3 percent. On

a cumulative basis, personal remittances in January-November 2015

rose by 3.4 percent to US$25.2 billion”2.

Let

us take personal remittances for November 2015: in the November 2015

report, the numbers were US $2.416 billion for the month and $25.25

billion in cumulative. These compared to December 2015 report’s US

$2.06 billion for the month, and $25.7 billion cumulative. The

difference for the monthly data alone was a staggering $356 million!

Because

the headline numbers were different, so should this be reflected on

the growth rates: for the same period based on November report, 3%

and 3.4% for monthly and cumulative, respectively. That’s against a

NEGATIVE 6.2% for the month and 4.4% cumulative!

Gadzooks

huge NEGATIVE numbers!

I

had the initial impression that these were merely one month

‘revisions’. But the BSP hardly makes revisions for OFW

remittances.

So

upon further scrutiny, I

realized that the entire

data

set for the year 2014 to 2015 had been overhauled!

(November

data released January 2015

and December

data released last week February 2015)

To

highlight the difference, let me use the personal and cash remittance

data on a cumulative basis for December 2014 extracted from both

reports.

In

the November report, December 2014 personal and cash remittance were

at $26.97 billion and $24.348 billion, respectively. In the December

report, December 2014 personal and cash remittance were at $ 27.273

and $ 24.628 correspondingly (see blue rectangles above). The

difference amounts to $303 million and $280 or 1.2% a piece.

Yet

once the base or reference numbers changes, everything else changes.

The

critical question is why

the sudden overhaul of the entire 2014 and 2015 data set???!!

(I

haven’t seen any explanation from the BSP’s report)

The

BSP cited that they reached the target. But they also didn’t

mention of the BIG NEGATIVE numbers from the altered data.

It’s

stunning to see that the modified numbers revealed of two consecutive

months where OFW remittances growth rates actually crashed! Yes, read

my lips, remittance output substantially SHRANK!!! (see

red rectangles at the above BSP table)

For

October and November, monthly growth rate for Personal remittances

cratered -4.1% and -6.1% while Cash remittances plummeted by -4.2%

and -6.2%, respectively!!!!

Moreover,

stagnation

in August and September numbers compounded

on the crash. Monthly growth rates for Personal remittances were -.8%

and +1.3% while Cash remittances -.6% and +1.3% correspondingly!

So

in the last 3 out of the 5 months for 2015, OFW

remittance monthly

year on year changes for both personal and cash output exhibited

CONTRACTION!!!!

The

last time remittances showed of growth shrinkage was in November of

2014 were monthly personal and cash remittances posted deficits of

4.5% and 4.4%. Apparently, the November 2014 episode seems to have

paved way for this year’s incredible downturn. I warned about the

spillover risks from November

2014’s remittance decline here.

Yet

to compare with the original

data (see green rectangle in the table above), the only negative

number that surfaced in the monthly change was in August,

specifically -.8% for personal remittance and -.6% for cash

remittance. Two other months, particularly July and October posted

less than 1% growth, namely .5% for both personal and cash remittance

in July and .2% for both categories in October.

This

implies that if the December figures were the accurate measure, then

what the BSP did was to camouflage the crashes of the October and

November figures, in the hope that December data would provide the

necessary enhancements for the yearend! Astounding!

Nonetheless,

what made the BSP hit their annual target was the sudden remarkable

increase in the growth rate of the personal and cash remittances

cumulative at 4.9% each, last December! But

this came about after only a major recalibration of the remittance

numbers for 2014 and 2015!

[As

a side note 5% used to be the low end, look at the charts, now it is

the high end]

Question

is: How much of the yearend increase had been a result of the

juggling of remittance numbers? Could

it be that the 2014 figures have been deliberately suppressed in

order to inflate the 2015 counterparts?

Notice

too the end of the year numbers were hoisted by the huge surge in the

growth rates of March and June 2015. The gains from these months

padded up on the remittance data that essentially cushioned the

erosion during the last 5 of 6 months! (see horizontal orange

ellipses in BSP table above)

Just

to cite the numbers for personal remittances: in March, for the

revised December data, growth rates were 15.5% monthly and 9.4%

cumulative. The original data registered 11% and 5.1%. Original

BSP disclosure here.

In June, for the revised December data, growth rates were 10.5%

monthly and 9.0% cumulative as against the original data 5.8% and

5.3%, original

BSP disclosure here.

Again,

did the BSP wait for the December data in the hope that the numbers

would improve significantly to elevate the yearend tally? In

the apparent failure to meet the BSP’s expectations, did the BSP

panic, thus prompting them to facelift the entire data set for 2014

and 2015 so as to cosmetically embellish the yearend outcome?

Has

the government’s recent floating of an “OFW

crisis”

been a trial balloon or a public conditioning for this?

Yet

even from the cumulative perspective, remittance growth rates, for

both personal and cash in the 2H (specifically from the collapse of

the 4Q), dived to its lowest

level since October 2009!

Additionally,

those revised numbers have

not erased

the inflection point or the law of diminishing returns or diminishing

growth rates for OFW remittances (see orange ellipses)

If

OFW remittances stagnated in Q4, then just how did the government

compute for Household

Final Consumption Expenditure for Q4 2015? (The same question

should apply to the Q3 2015)

HFCE

constant 2000 and NGDP both rose during the said period (upper

window) even when the average monthly growth rate (based on revised

data) of OFW remittances for the quarter decreased.

Previously,

remittance growth rates mirrored the undulations of the NGDP and RGDP

(constant 2000) as shown in the lower window. But for Q4 things

changed. Again, HFCE, which accounted for 72% of the 4Q RGDP grew by

6.9% NGDP and by 6.4% RGDP even as the average monthly (nominal|)

remittance growth rates for the same period shriveled by 1.5%.

Stunning deviations!

Once

again, OFWs have been stripped by government statisticians as

economic heroes!

Said

differently, just where did 6.3% Q4 GDP (5.2% NGDP), as well as, 6.1%

Q3 GDP (4.4% NGDP) emerged from? (see lower window)

Contrary

to consensus thinking, I have been warning that OFW remittances have

not been static or permanently embedded growth numbers and have been

vulnerable to global economic

as well as geopolitical

developments.

Now

my warnings appear to have arrived.

And

again, it would appear that the BSP has employed statistical mirages

in order to beef up the highly symbolic and economic sensitive OFW

remittance numbers.

Unfortunately,

in spite of the Potemkin numbers, a sustained slump in remittances

will show up in the real economy.

So

expect one of the next hot political issues to be the “OFW crisis”.

Of

course, forget

that the reason OFWs exist have been because of the legacy of

consistent government failures, as demonstrated by the slomo boiling

frog collapse of the peso. The current boom bust cycle will only

exacerbate on this.

And

given the considerable data revisions which exposed of the massive

downturn in OFW remittance growth rates in 2H 2015, just

what will happen to the mythical consumer economy?

The

ballyhooed ‘consumer economy’ has in reality has been about the

massive debt financed race to build the supply side predicated on

catering to mainly OFW spending!

Yet

in the face of falling exports, wilting manufacturing, stagnating

agriculture and slumping remittances, just where will the incantation

of “domestic demand” emanate from?

Most

likely from statistical

Sadako!

{kind=link}

Negative

Numbers Spur PSE to CENSOR 3Q 2015 Performance of Listed Firms as

Philippine NGDP and PSE’s NGDP Goes on DIVERGENT Directions!

It

appears that the establishment has been getting so desperate to keep

up with façade of the phony boom.

So

they increasingly resort to rampant financial market (stock market,

bonds and currency) pumps, statistical chicanery, flagrant media

spins and information censorship and manipulation

Well

as expected, the Philippine Stock Exchange (PSE) did it again.

Like

in the second quarter, the PSE has CENSORED or blacked out the

aggregate performance of ALL listed companies during the third

quarter from their press

release.

So

in the absence of disclosure, the PSE’s dismal 3Q fundamentals

translated to a virtual VACUUM in mainstream media.

So

what the PSE did was to announce the NINE month performance of the

PSE’s composite members in their monthly outlook (December issue)

WITHOUT the 3Q numbers!

And

to consider that the distribution of PSE monthly outlook have been

restricted to only paid

subscribers, and that the monthly report are technical, and more

importantly, long winded, the likelihood has been that the reach of

audience for the content of such reports have been very limited.

But

why does the PSE want to bury such information? Below is the original

format

The

answers as provided by the PSE3

(bold mine)

-The

total income of listed companies decreased

by 1.8%

year-on-year in the first nine months of 2015. Data from the latest

financial statements submitted by 2481 out of 260 listed companies

showed that their aggregate income totalled P441.40 billion, P8.17

billion lower than the P449.56 billion income recorded in the same

period last year. Out of the 248 reporting listed companies, 179

posted net gains, 68 posted net losses, while one posted zero income.

The decline in overall earnings performance of listed companies was

primarily

brought about by higher foreign exchange losses and significant

decline in metal prices.

-Listed

companies garnered a combined P4.90 trillion in revenues during the

first nine months of 2015, lower

by 0.6%

from their total revenues of P4.93 trillion in the same period last

year

-The

combined net income of companies comprising the PSEi amounted to

P317.61 billion during the first nine months of 2015, 0.7% higher

than their aggregate net income of P315.51 billion in the same period

last year.

-The

combined net income of PSEi companies represented 72.0% of the total

net income of the 248 reporting listed companies, slightly

higher

than its 70.2% share to total income in the same period last year.

-Twenty

nine of the PSEi members registered net profits, with TEL posting the

highest net income for the period at P25.34 billion. SMPH followed

with net profits amounting to P22.87 billion, while SM came in third

with earnings of P19.43 billion. SM posted a 7.0% increase in income

during the first nine months mainly due to higher revenue

contributions of its key business segments.

-Twenty

one

of the thirty PSEi companies posted improved

net income performances during the period with LT Group, Inc. (LTG),

SMPH, Semirara Mining and Power Corporation (SCC), GLO, and PCOR,

posting remarkable increases of 88.7%, 69.9%, 58.8%, 34.4%, and

34.3%, respectively. LTG recorded an income of P4.71 billion driven

by the improved bottomline of its core businesses.

-Meanwhile,

the remaining nine

companies

recorded

decreases

in their net income in the first nine months of 2015 with Bloomberry

Resorts Corporation (BLOOM), Megaworld Corporation (MEG), SMC, Energy

Development Corporation (EDC), and First Gen Corporation (FGEN),

posting contractions of 145.3%, 56.9%, 53.2%, 43.5%, and 25.0%,

respectively. Higher operating costs and expenses associated with the

operation of the Sky Tower and related amenities pulled down BLOOM’s

bottomline.

-Two

out of six sectors posted higher net incomes

for the first nine months led by the Property sector, which

registered the highest growth at 6.4% for the period. The Services

sector followed, with its aggregate net income rising by 4.1%.

Meanwhile, total

profit of companies in the Financials, Holding Firms, Industrial, and

Mining & Oil sectors declined by 0.5%, 0.5%, 2.9%, and 54.1%,

respectively.

-The

net income of companies in the Small, Medium & Emerging Board

(SME) increased by 6.2% to P187.98 million during the first nine

months of 2015 from P177.03 million in the same period last year. The

growth in mobile consumer business pulled up Xurpas Inc.’s (X) net

profit by 19.0%. On the other hand, the net profits of Makati Finance

Corporation (MFIN) and Alterra Capital Partners, Inc. (ALT) fell by

12.5% and 163.2%, respectively

Only

two sectors have now been lifting the profits of the PSE universe as

the majority have begun to underperform. It’s the periphery to the

core in motion. The backlash from inflationary boom has been gnawing

at the core of the bubble industries.

The

PSE notes that aside from metals or commodities, foreign exchange has

signified a key factor in the nine month deterioration.

As

previously admonished4:

(bold original)

For

domestic production, prices of imported production inputs will

also increase.

Rising input costs should put a squeeze on

the profits of producers. And profit margin strains will

mean lesser investments,

which subsequently should extrapolate to lesser

outputs and diminished

jobs and wage improvements.

And lesser production output means HIGHER domestic prices. In short, again whatever gains from the lower peso on OFW, exports, BPOs and or tourism will be mostly neutralized by rising domestic prices overtime.

And again, the ascendant domestic prices have been the effects of higher import prices.

Moreover, in the financial dimension, any USD based liabilities will require MORE peso to service. Once again this adds to the cost side of firms exposed on USD borrowings that will amplify debt servicing onus that may reduce access to credit, thereby, put strains on profits and magnify credit risks.

The

PSE forgets that the profit squeeze has not just been about cost

side, but likewise on the top line. This means that aside from higher

prices on imported consumer goods brought about by the falling peso,

those 10 months of 30%+++ money supply growth (July 2013 to April

2014) that have led to a belated surge in consumer inflation (3%+ for

13 months or from November 2013 to November 2014) have buffeted on

the PSE’s gross revenues or the NGDP.

Curiously

just where has mainstream’s touted double digit earnings growth for

the PSE in 2015 been???

Remember,

the above represents the Nine Month report for 2015.

Again,

missing in the above had been the third quarter performance.

Well,

the likely reason they have been expunged the 3Q from the report can

be seen above

You

see, reporting

of losses may have been disallowed most probably because they are

construed as politically

incorrect.

Revenues and profits for the PSE can only go up! And everything else

outside this premise represents an anomaly or deemed as unreal.

Income

of both PSEi and PSE listed firms were down by a huge 10.66% and

1.68% in the 3Q. NGDP (Gross revenues) of listed firms was down by

-.6% but was slightly up by .46% for PSEi firms. Though

NGDP showed slight improvements for both, income remained

significantly down.

So

essentially, the big income gains of 1Q, which

was a result from the outperformance of select issues, diminished

the declines of the NINE month report.

What

a way to spin the story!

But

haven’t you noticed of the disparity between real and statistical

numbers?

The

Philippine government announced that

3Q GDP grew by 4.4% NGDP or 6.1% (2000) constant/headline GDP,

but the PSE’s NGDP (gross revenues) of all listed firms shriveled

by -.06%!!!

Realize

that the PSE’s NGDP, which accounts for street level accounting

based activities, constitute 51.6% of the survey based statistical

(Nominal or current priced) GDP.

What

this exhibits has been that the PSE’s (street level) numbers and

the Government’s (survey based) numbers seem to

be pointing at DIVERGENT directions!

Government says G-R-O-W-T-H! On the other hand, PSE firms say

S-T-A-G-N-A-T-I-O-N!

So

what we have been witnessing has been a blatant departure from real

developments relative to glorifying headline statistical numbers.

As

I commented on the bowdlerization of the 2Q report5

And

this also demonstrates why statistical GDP has basically little

relevance with actual economic conditions!

Instead

of Gross Domestic Products, GDP should be called Grossly

Deceptive Politics

And yet

those 2Q unpleasant numbers signify as the smoking

gun revelation of the hissing bubble ‘smoke and mirrors’

economy. The 2Q data essentially DEFIES the politically constructed

one way consensus expectations.

And

this shocking reality may have incited the Philippine Stock Exchange

to exorcise, purge, exclude or censor such figures out of existence!

Such that when the PSE reported 1H 2015 performance, 2Q seemed to

have almost existed in a black hole.

Add

3Q to the picture.

Philippine

Bonds: The Fascist Crony Political Economy and The Escalation of the

Yield Curve Inversions!

Given

that the government raised Php 25 billion in fund raising via 5 year

tender last week, which reportedly drew

in “double” the government’s offer from mostly banks due to

“strong demand”, I expected a significant rally on domestic

treasuries this week.

Yet

my expectation was not fulfilled. The rally on the 5 year bonds

turned out to be short lived as 5

year bond yields increased by 37.5 bps to 4.313% at the close of

the week from last week’s 3.938%.

So

the alleged “strong demand” for government “tenders” turned

out to be a dud, as the secondary market sold the same treasuries

(perhaps) right after bidding them up.

More

of the same publicity gimmicks or smokescreens?

Moreover,

I expected the peso to rally hard given that the government announced

that they will raise dollars through “planned

sale of dollar-denominated bonds”. It didn’t. The USD peso rose

by .32% to Php 47.665 this week from Php 47.51 the previous week.

Perhaps, the peso rally may happen when the sale will be formalized

or concluded. There has been no definite schedule announced. Though

it was tipped to be “soon”.

Yet

the government

have “hired eight banks” as their book runners.

Let

me interpose my terse political inquiry on these.

Think

of the banks that have been commissioned to underwrite and sell bonds

in behalf of the government. They are bound to make millions of

dollars in fees and commissions as agents for the government. These

institutions are essentially beholden to the government by virtue of

the latter’s administrative and regulatory controls, the

distribution of economic rent from government activities (such as

book running or underwriting government securities), and most

importantly, as conduits and beneficiaries of financial repression

policies imposed by the government

(e.g. tax agents, intermediaries for the government securities,

credit agents and etc.).

So

do you think that such entities will risk or sacrifice all the

prospective emoluments or economic rent and other privileges by

citing risks from the current activities or by making radical

downside G-R-O-W-T-H projections against the government’s outlook,

or more explicitly, by deviating from the interests of the

government? Do you think that the same financial entities will put

their depositors’ and fiduciary interests ahead of that of the

government?

Do

you think mainstream media, whom are paid for by advertising revenues

from mostly firms owned or attached or affiliated to these

institutions, would publish materials or opinions against them? Do

you think that academic experts, whose schools have been bankrolled

or owned by the same or related institutions, would rail against

their benefactors?

Much

of what one sees as “debates” or “criticism” among media’s

talking heads center on the superficial rather than a thorough

examination of the system. Most of them are fixated on personalities.

And

the centralization, or the particularly, the politicization of system

is what makes everything inherently fragile or vulnerable to a

meltdown.

By

virtue of social policies, resources have virtually been funneled

into vested interest groups affiliated with the government, and to

the government. Such translates to the amassment of systemic

distortions or imbalances.

And

with everyone being told by the government, cronies, and by media

lapdogs, backed by their ‘experts’, that everything has been

hunky dory, these simply extrapolates to the desired sustainment of

the facilitation of such invisible transfers—where, again, such

invisible redistribution or hidden taxation has been intermediated by

these private sector appendages of political institutions.

And

what has been presented in media as economic news has signified as

nothing more than sales

pitches

ornamented with statistical numbers and emblazoned with economic

variables to justify the status quo.

This

by the way HARDLY represents free markets at all. Instead, such are

fascist-corporatist/cronyism political economy guised under the

simulacrum of a market economy.

One

cannot operate a genuine market economy with half of every

transaction being perverted in favor of political agents through

unsound monetary policies. Add to this the mountains of regulatory,

tax and welfare mandates.

The

market economy has been setup as the fall guy once these

maladjustments will unravel.

So

risks or negative news or developments that will serve as obstacles

to the free lunches for the establishment will forcibly be submerged

into oblivion.

Such has been the likely reasons behind the BSP’s December OFW

report and to the PSE’s 2Q and 3Q report.

Unfortunately

for establishment, there is such a thing called the law of scarcity.

And the law of scarcity tells us that the vast misallocation of

resources will have natural limits regardless of what the

establishment yearns for.

The

fundamental lesson: There is no such thing as a free lunch.

And

NO free lunch is being expressed today on the Philippine bond markets

Despite

the sustained interventions to facelift the Philippine treasury

markets, yield

spreads point to a forthcoming significant stress in the domestic

financial system’s liquidity.

As

of Friday, the yield differential between the 10 year bond and 6

month bill has flattened to near zero (4.2 bps). Stealth

interventions pushed the 1 month spread off from a negative spread

last week. But the variance still remains at near zero (47.4 bps)

Yet

the negative yield curve phenomenon has been spreading.

ADB’s

benchmark the 10 year 2 year yield spread remains flat with only 23.8

bps away from zero. The 10yr-3yr spread has been on a second week of

inversion. The 10yr-4yr spread has also inverted! The negative spread

of the curve’s belly, the 10yr-5yr, has only deepened to 49.7 bps!

So

despite constant interventions, negative yield phenomenon prevails.

While

narrowing interest margins may dissuade banks from expanding credit,

this may not be enough. Desperate for profits, banks may seek to

replace thinning margins with volume. But the substitution of volume

with margin means assimilating on more credit risk than necessary.

And this is where things will get aggressively dicey.

And

financial institutions will likely run rings around the regulatory

climate.

Nonetheless,

if

credit conditions will tighten as the yield curve continues to

indicate, then economic weakness can only be expected to permeate

into a larger segment of the economy.

Unlike

the consensus experts who read the economy through painting by the

numbers or by shouting statistics, remember the economy represents a

complex network of interrelated and interdependent agents. Like the

Butterfly effect of the chaos theory, where a flapping of the

butterfly’s wings may ripple into a storm, one’s sector’s

weakness may spread into the rest of the economy, even while the

mainstream remains blind to these.

Yet

such blindness has not been because they are unintelligent, most of

them are incredibly smart, but rather incentives to protect the

status quo and the principal agent problem represent as the primary

causes of such myopia.

The

fantastic

spreading of the negative yield spreads will most likely serve the

key transmission mechanism for the unwinding of the domestic bubble.

In

2009,

the BSP declared the adaption of an accommodative monetary policy,

or the reconfiguration of the economy, by tweaking the yield curve as

a means to promote domestic demand. Now

the basis for the soi-disant “domestic demand” is being reversed

by the market place.

Since

Philippine asset bubbles have emerged and has been nurtured and

fostered on credit expansion from the BSP’s credit easing policies,

then a reversal of monetary accommodation either through policies or

from the marketplace would entail of the taking away or undermining

of the credit pillar. And once such pillar has been disestablished,

then these bubbles will fall like a house of cards.

Robinson’s

Land Corp: Leveraging UP on a Vulnerable Topline

One

of the companies to have reported earnings for December 2015 has been

key property developer and shopping mall operator, Robinsons Land

(RLC)

Curiously,

while RLC reported gross revenues to have jumped 12.5% for its first

3 months (RLC’s fiscal year ends in September) what has been

evident has been real estate sales have significantly underperformed

having been up by a measly 3.99%! Has this signified possible signs

of weakening

property sector in the 4Q?

RLC’s

real estate sales have lagged for two straight years (up .26% in

2014)! (top window)

Yet

shopping mall revenues, which grew by 14.38%, and which was

responsible for the gist of the topline for the period, had largely

been driven by the “contribution

of the new malls namely Robinsons Place Antipolo, Robinsons Place Las

Pinas, Robinsons Place Antique and Galleria Cebu”6.

The company reported that “same

mall rental revenue growth of 7%” and stunningly, “system-wide

occupancy rate was stable at 95% as of December 31, 2015”.

From

the surface, about half of RLC’s mall revenues came from existing

malls and the other half from new malls.

Yet

what defines same mall rental revenue? Has it been increases in

rental rates? Or has it been from the overrides/royalties on the

lessee’s store sales? Or how has these been distributed?

It

matters because even from the government’s GDP,

growth of retail sales moderated in Q4 to 7% from 8.7% in Q3

(current) or 7% from 8.3% (constant 2000). So if retail sales have

been slowing, then most of the top line growth from same mall rents

must have come from rate increases. So if rental rate increases

stall, then RLC’s top line will be in jeopardy or will

substantially fall.

Yet

the addition of 4 malls (11.7%) to its inventory, which now has

reached 38 malls, suggest that the contribution from new malls have

not been optimized (I am speaking here of only malls not actual

retail spaces in sqm for rent). What will happen to its vacancy

rates, which are now at 5%, if diminishing returns affect the new

malls? How will RLC maintain its topline growth conditions and its

profitability?

It’s

the first time I have encountered RLC mention “occupancy rates”

in their December reports since 2009. So I have no idea what their

definition of “stable” means. What I ascribed to as “stunning”

was because the firm’s occupancy rates seem to have now fallen to

US levels.

In

the US, dead malls or the extinguishment of excess capacity over the

years along with improvements in retail sales had brought about

occupancy

rates to rise to 94.2% at the end of 2014. As explained last

week, this could be much lower today.

Yet

if RLC, a major developer and mall operator, has vacancy rates of 5%,

how much more for the rest of the industry, especially for the lesser

known or established contemporaries?

(Yes in my recent mall sorties I can attest to this bulging turnovers

and vacancies)

And

what will happen to the industry vacancy rates, not only if topline

declines, but if the supply side like RLC will continue to add

inventories? RLC

reported a capex of Php 16-17 billion for 2016 up 6.67% to 13%

from 2015’s Php 15 billion.

Here’s

more. What has been striking from the report has been the dearth of

cash flows from populist headline G-R-O-W-T-H! RLC’s receivables

have ballooned by 49% in 2014 and 29.26% in 2015 even as real estate

sales have been dismal. (lower left window) Has this been about late

payments?

And

like her peers, RLC has huge uncollected accounting profits.

Also

because RLC has engaged in massive inventory buildup in 2014 and

investments in 2015, financing of such activities entailed that the

firm’s total debt swelled by 40.36% in 2014 and 69.33% in 2015

(lower right window)!

While

RLC’s topline has become increasingly vulnerable to an economic

downturn, the company has rampantly been levering or gearing up on

expectations that Filipino consumers have hit the national lottery

with no end!

RLC

seem to have been transformed from a conservative (little debt) to a

high roller (heavy debt) firm…all predicated on hope.

When

the impact from those yield curve inversions spread to a broader

sector of the real economy, backed by the sustained fall in the peso,

RLC’s derring-do gambit will put her balance sheet in a parlous

position.

RLC

officials better be right that too the Philippines will be “immune”

to external developments and that strong/robust/resilient “domestic

demand” represents a linear thing. Though they didn’t directly

say these, their balance sheet expresses on such convictions

(demonstrated preference).

Actions

have consequences. Actions premised on wrong expectations can have

nasty consequences.

Phisix

6,800: Global Central Banks Talk Up Risk Assets as Philippine Stocks

Approaches Overbought Conditions

Last

week I wrote7

This

is not to say that actions of central banks will have no effects on

the markets. Rather, present dynamics have shown diminishing returns

in terms of boosting risk assets. Or said differently, central bank

magic has been fading. But it won’t stop them from trying.

Central

bankers ensured that they were on the spotlights last week. They were

there to soothe on the scathed nerves of increasingly apprehensive

casino gamblers.

The

Chinese central bank, the People’s Bank of China (PBoC), opened the

lunar New Year by firming the yuan’s fixing, which according to the

Bloomberg,

“was the most in three months”.

China’s

PBOC Governor Zhou Xiaochuan broke his long silence to declare

support on the yuan by saying “there’s

no basis for continued yuan depreciation”. Chinese officials

stepped on the stimulus rhetoric in stating that they would be

“making

more money available to local governments to fund new infrastructure

projects”. Authorities also floated the plan to lower “the

minimum ratio

of provisions that

banks must set aside for bad loans, a move that would free up

additional cash for lending”.

In

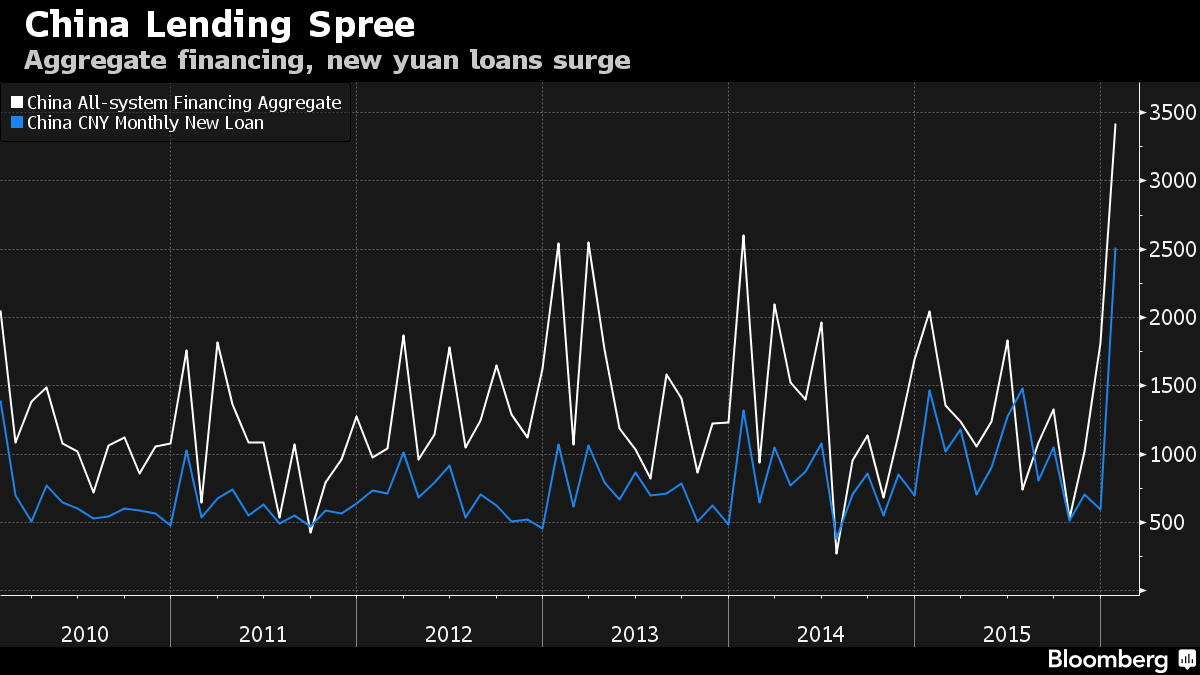

the meantime, China’s January’s lending skyrocketed to a new

record, HALF a trillion USD (3.42

trillion yuan or $525 billion) in a month!!! (see chart

here). This comes even

as January’s external trade has collapsed while December NPLs soar

to milestone highs!

{kind=link}

Meanwhile,

ECB’s Mario Draghi reasserted that the European

Central Bank won't hesitate to boost its stimulus in March if it

believes recent financial-market turmoil or lower oil

prices could

weigh further on stubbornly low inflation.

Meanwhile,

Federal

Reserve Bank of St. Louis President James Bullard called

for a delay in interest rate hikes saying that “I regard it as

unwise to continue a normalization strategy in an environment of

declining market-based inflation expectations”. Mr Bullard added,

“The recent sell-off in global equity markets, along with increases

in risk spreads in corporate bond markets, may have made this risk

less of a concern over the medium term…These data-dependent changes

likely give the FOMC more leeway in its normalization program”

In

the meantime, at

the G-20 meeting, Bank of Japan’s

Haruhiko Kuroda appealed to other counterparts “to find ways to

stabilize global financial markets”.

The

OECD

joined the calls for fresh stimulus mostly from government

spending and not just credit easing by central banks. They said that

“Governments in the U.S., Europe and elsewhere should take "urgent"

and "collective" steps to raise their investment spending

and deliver a fresh boost to flagging economic growth…In its most

forceful call to action since the financial crisis, the OECD said the

global economy is suffering from a weakness of demand that can't be

remedied through stimulus from central banks alone.”

Governments

have been panicking over the latest financial market turmoil. And

central banking coordinated opiates haves served to fuel massive

short covering or short squeezes that have led to broad based

resurgence in risk assets.

Most

of Asia’s equity markets went into overdrive with benchmarks

posting gains by 1.5% and above. (see left window)

Japan’s

Nikkei, for instance, soared 6.79% this week after collapsing 11.1%

the other week.

The

intense tug of war between the bears and the bulls has been a

manifestation of developing instability. Sharp volatilities are

hardly signs of bottom. Instead they are most like manifestations of

a denial phase.

The

question is how long before central bank assurances begin to fade?

On

the other hand, those central bank jawboning appears to have worked

less in the favor of Asian currencies. Despite the risk ON, the USD

has risen against most Asian currencies this week.

This

means that the USD has ignored central bank assurances.

Meanwhile,

the Philippines joined the global stock market party.

With

this week’s 2.07% advance, the Philippine Phisix racked up its

third week of substantial gains in four.

This

week’s gains had been broad based. All sectors rose led by the

service (+3.08%) and the industrial sector (+3.06%).

Among

the 30 issue composite index, 25 registered gains while 5 posted

losses.

Market

breadth was heavily tilted towards advancers. The spread in favor of

advancers hit the second highest level for the year.

Peso

volume increased modestly. This week’s average volume at Php 7.232

billion was the second highest for the year.

(Due

to space constraints posting of charts have been limited)

However,

given the degree of advances over the past four weeks, specifically

11.63% from the January 21 2016 lows (or in 21 days), peso volume

should have been way much much much bigger.

For

comparison, the average peso volume during minor bear rallies in 2013

were much larger than today.

In

August 28 to October 23 2013, where the PSEi returned 15.63% the

average peso trading volume during the period was at Php 10.483

billion. In June 25 to July 24 2013, where the PSEi rallied by

17.53%, the average volume was at Php 8.295 billion.

During

the 2016 cycle, from January 21, the average daily volume had been a

puny Php 6.673 billion! This means that current volume accounted for

only 64% of the August-October rally and 80.44% of the June-July

rebound.

As

previously noted, bear markets are characterized

by rallies that have been fast and furious. A volumeless rebound

seems indicative of a lack of conviction.

Yet

at .58%, the rate of the average daily gains seems as decelerating,

perhaps indicating signs of emerging fatigue.

Helped

by several sessions of last minute pumps by Team

Viagra, the PSEi now approaches critical resistance levels and

have emitted signs of overbought conditions.

Yet

current gains of the PSEi seem as hardly being supported by the still

weak peso, the incredible spreading of yield curve inversions on

domestic sovereign bonds and little signs of meaningful improvements

in earnings.

Most

of the

gains have been anchored on HOPE.

____

1

Bangko

Sentral ng Pilipinas Personal

Remittances Exceed 4 Percent Growth Projection for 2015; Full-Year

Level Reaches US$28.5 Billion February 19, 2016

2

Bangko

Sentral ng Pilipinas, Personal

Remittances Sustain Growth in November 2015; Year-to-Date Level

Reaches US$25.2 Billion January 15, 2016

3

Philippine

Stock Exchange, December 2015 Monthly Report VOL. XXII NO. 12

4

see

Phisix

7,050: The Peso in the Face of Crashing Emerging Market and ASEAN

Currencies September 6, 2015

5

See

Phisix

6,900: Smoking Gun Evidence: PSE Listed Firm’s 2Q NGDP Drops By

3%, as Income Dives 7.5%!

December 6, 2015

6

ROBINSONS

LAND CORPORATION AND SUBSIDIARIES SEC

Form 17-Q Philippine Stock Exchange