If there is one common theme to the vast range of the world’s financial crises, it is that excessive debt accumulation, whether by the government, banks, corporations, or consumers, often poses greater systemic risks than it seems during a boom. Infusions of cash can make a government look like it is providing greater growth to its economy than it really is. Private sector borrowing binges can inflate housing and stock prices far beyond their long-run sustainable levels and make banks seem more stable and profitable than they really are. Such large-scale debt buildups pose risks because they make an economy vulnerable to crises of confidence, particularly when debt is short term and needs to be constantly refinanced—Carmen Reinhart and Kenneth Rogoff

In this issue

BSP’s Aggressive RRR

Cuts: A High-Stakes Gamble?

I. Decline

in 2024 Bank Non-Performing Loans Amidst Record-High Debt Levels and a Slowing

Economy

II. Deepening Financialization: Financial Assets Surge in 2024

as Banks Drive Industry Monopolization

III. Viewing Bank’s Asset Growth Through the Lens of the PSE

IV. March 2025 RRR Cuts and the Liquidity Conundrum: Unraveling

the Banking System’s Pressure Points

V. Liquidity Drain: Record Investment Risks and Elevated

Marked-to-Market Losses

VI. Despite Falling Rates, Bank’s Held-to-Maturity Assets Remain

Near Record High

VII. Moral Hazard and the "COVID Bailout Playbook"

VIII. The Bigger Picture: Are We Headed for a Full-Blown Crisis?

IX. Conclusion: RRR Cuts a High-Risk Strategy?

BSP’s Aggressive RRR Cuts: A High-Stakes Gamble?

The BSP announced another round of RRR cuts in March amid mounting liquidity constraints. Yet, the reduction from 20% in 2018 to 7% in 2024 has barely improved conditions. Will this time be different?

I. Decline in 2024 Bank Non-Performing Loans Amidst Record-High Debt Levels and a Slowing Economy

Inquirer.net, February 14, 2025: Soured loans held by Philippine banks as a ratio of total credit eased to their lowest level in a year by the end of 2024 as declining interest rates and softer inflation helped borrowers settle their debts on time. However, a shallower easing cycle might keep financial conditions still somewhat tight, which could prevent a big decline in bad debts this year. Preliminary data from the Bangko Sentral ng Pilipinas (BSP) showed the gross amount of nonperforming loans (NPLs)—or credit that is 90 days late on a payment and at risk of default—had cornered 3.27 percent of the local banking industry’s total lending portfolio as of December, down from November’s 3.54 percent. That figure—also known as the gross NPL ratio—was the lowest since December 2023, when bad loans accounted for 3.24 percent of banks’ total loan book.

An overview of the operating environment

In any analysis, it is crucial to understand the operating environment that provides context to the relevance of a statistic in discussion.

The Bangko Sentral ng Pilipinas (BSP) initiated its ‘easing cycle’ in the second half of 2024, which included three rate cuts and a reduction in the reserve requirement ratio (RRR). Meanwhile, inflation (CPI) rebounded from a low of 1.9% in September to 2.9% in December. Additionally, the BSP tightened its cap on the USDPHP exchange rate. Fiscal spending over the first 11 months of the year reached an all-time high.

Yet, there are notable contradictions.

Despite record-high bank lending—driven largely by real estate and consumer loans—GDP growth slowed to 5.2% in the second half of 2024 primarily due to the weak consumer spending. The employment rate was also near an all-time high.

Figure 1

Meanwhile, real estate prices entered deflationary territory in Q3, with the sector’s real GDP growth falling to its lowest level since the pandemic-induced recession. Its share of total GDP also dropped to an all-time low.

Notably, the real estate sector remains the largest borrower within the banking system (encompassing universal, commercial, thrift, and rural/cooperative banks). (Figure 1, topmost chart) This data depends on the accuracy of the loans reported by banks.

However, despite recent rate cuts and significant reductions in RRR, the sector remains under pressure. Additionally, sluggish GDP growth suggests mounting risks associated with record levels of consumer leverage.

Upon initial analysis, the decline in non-performing loans (NPLs) appears inconsistent with these economic developments. Gross NPLs dropped to one-year lows, while net NPLs reached levels last seen in June 2020. (Figure 1, middle window)

Ironically, the BSP also announced another round of RRR cuts this March.

II. Deepening Financialization: Financial Assets Surge in 2024 as Banks Drive Industry Monopolization

Let's now turn to the gross assets of the financial system, also known as Total Financial Resources (TFR).

The BSP maintained its policy rate this February.

Ironically, BSP rates appear to have had little influence on the assets of the bank-financial industry.

In 2024, TFR surged by 7.8% YoY, while bank resources jumped 8.9%, reaching record highs of Php 33.78 trillion and Php 28.255 trillion, respectively.

Why does this matter?

Since the BSP started hiking rates in April 2022, TFR and bank financial resources have posted a 9.7% and 10.9% compound annual growth rate (CAGR), respectively. In short, the growth of financial assets has accelerated despite the BSP’s rate hikes.

Or, the series of rate hikes have barely affected bank and financial market operations.

By the end of 2024, TFR stood at 128% of headline GDP and 152% of nominal GDP, while bank resources accounted for 107% and 127%, respectively. This reflects the increasing financialization of the Philippine economy—a growing reliance on credit and liquidity—as confirmed by the Money Supply (M series) relative to GDP. (Figure 1, lowest image)

Banking Sector Consolidation

Figure 2

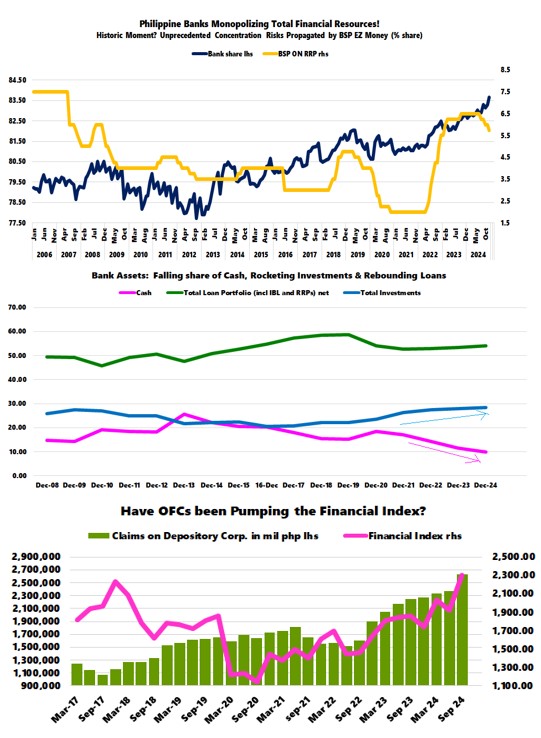

More importantly, the rate hikes catapulted the bank's share of the TFR from 82.3% in 2023 to an all-time high of 83.64% in 2024, powered by universal and commercial banks, whose share jumped from 77.6% to 78.3%! (Figure 2, topmost diagram)

Effectively, the banking industry—particularly UCBs—has been monopolizing finance, leading to greater market concentration, which translates to a build-up in systemic concentration risk.

As of December 2024, bank assets were allocated as follows: cash, 10%; total loan portfolio (inclusive of interbank loans and reverse repurchase agreements), 54%; investments, 28.3%; real and other properties acquired, 0.43%; and other assets, 7.14%.

In 2024, the banking system’s cash reserves deflated 6.01% YoY, while total loans and investments surged by 10.74% and 10.72%, respectively.

Yet over the years, cash holdings have declined (since 2013), loan growth has been recovering (post-2018 hikes), and investments have surged, partially replacing both. (Figure 2, middle image)

Notably, despite the BSP’s historic liquidity injections, banks' cash reserves have continued to erode.

The catch-22 is that if banks were profitable, why would they have shed cash reserves over the years?

Why the series of RRR cuts?

III. Viewing Bank’s Asset Growth Through the Lens of the PSE

During the Philippine Stock Exchange Index (PSEi) 30’s run-up to 7,500, Other Financial Corporations (OFCs)—potentially key players in the so-called "national team"—were substantial net buyers of both bank and non-bank equities.

BSP, January 31, 2025: "The q-o-q rise in the other financial corporations’ domestic claims was attributable to the increase in its claims on the depository corporations, the other sectors, and the central government. In particular, the other financial corporations’ claims on the depository corporations grew as its holdings of bank-issued debt securities and equity shares increased. Likewise, the sector’s claims on the other sectors grew as its investments in equity shares issued by other nonfinancial corporations and loans extended to households expanded. The growth in the OFCs’ domestic claims was further supported by the rise in the sector’s investments in government-issued debt securities" (bold added)

The OFCs consist of non-money market investment funds, other financial intermediaries (excluding insurance corporations and pension funds), financial auxiliaries, captive financial institutions and money lenders, insurance corporations, and pension funds.

In Q3 2024, claims on depository corporations surged 12% YoY, while claims on the private sector jumped 8%, both reaching record highs in nominal peso terms.

Meanwhile, the PSEi and Financial Index surged 15.1% and 23.4%, respectively. The Financial Index hit an all-time high of 2,423.37 on October 21st, and as of this writing, remains less than 10% below that peak. The Financial Index, which includes seven banks (AUB, BDO, BPI, MBT, CBC, SECB) and the Philippine Stock Exchange (PSE) as the sole non-bank component, has cushioned the PSEi 30 from a collapse. (Figure 2, lowest chart)

Figure 3

It has also supported the PSEi 30 and the PSE through the private sector claims. (Figure 3, topmost pane)

The irony is that OFCs continued purchasing bank shares even as the banking sector’s profit growth (across universal-commercial, thrift, and rural/cooperative banks) materially slowed (as BSP’s official rates rose)

In 2024, the banking system’s net profit growth fell to 9.8%, the lowest in four years. (Figure 3, middle chart)

Meanwhile, trading income—despite making up just 2.2% share of total operating income—soared 78.3% YoY.

The crux is that the support provided to the Financial Index by the OFCs may have enabled banks to increase their asset base via their ‘investment’ accounts, while simultaneously propping up the PSEi 30.

Yet, this also appears to mask the deteriorating internal fundamentals of Philippine banks. (Figure 3, lowest graph)

There are several possibilities at play:

1. The BSP’s influence could be a

factor;

2. Banks may have acted like a cartel

in coordinating their actions

3. The limited depth of Philippine capital markets may have forced the industry’s equity placements into a narrow set of options.

But in my humble view, the most telling indicator? Those coordinated intraday pumps—post-recess "afternoon delight" rallies and pre-closing floats—strongly suggest synchronized or coordinated activities.

The point of this explanation is that Philippine banks and non-bank institutions appear to be relying on asset inflation to boost their balance sheets.

Aside from shielding banks through liquidity support for the real estate industry, have the BSP's RRR cuts also been designed to boost the PSEi 30?

IV. March 2025 RRR Cuts and the Liquidity Conundrum: Unraveling the Banking System’s Pressure Points

Philstarnews.com, February 22, 2025: The Bangko Sentral ng Pilipinas (BSP) surprised markets yesterday as it announced another major reduction in the amount of deposit banks are required to keep with the central bank. The BSP said it would reduce the reserve requirement ratios (RRR) of local banks, effective March 28, to free up more funds to boost the economy. “The BSP reiterates its long-run goal of enabling banks to channel their funds more effectively toward productive loans and investments. Reducing RRRs will lessen frictions that hinder financial intermediation,” the central bank said…The regulator slashed the RRR for universal and commercial banks, as well as non-bank financial institutions with quasi-banking functions (NBQBs) by 200 basis points, to five percent from the current level of seven percent.

The BSP last reduced the reserve requirement ratio (RRR) on October 25, 2024. With the next cut taking effect on March 28, 2025, this marks the fastest and largest RRR reduction in recent history.

In contrast, the BSP previously cut RRR rates from 18% to 14% over an eight-month period between May and December 2019.

Why the RRR Cuts if NPLs Are Not a Concern?

Figure 4

BSP’s balance sheet data from end-September to November 2024 shows that the RRR reduction led to a Php 124.5 billion decline in Reserve Deposits of Other Depository Corporations (RDoDC)—an estimate of the liquidity injected into the system. The downtrend in bank reserves since 2018 reflects the cumulative effect of these RRR cuts. (Figure 4, topmost image)

Yet, despite the liquidity injection, the banking system’s cash and due-from-bank deposits continued to decline through December. It has been in a downtrend since 2013. (Figure 4, middle pane)

Cash reserves dropped 6% in 2024, marking the third consecutive annual decline. The BSP’s 2020-21 historic Php 2.3 trillion injection has largely dissipated.

Since peaking at Php 3.572 trillion in December 2021, cash levels have fallen by Php 828 billion to Php 2.743 trillion in December 2024—essentially returning to 2019 levels. (Figure 4, lowest chart)

Figure 5

The BSP’s other key liquidity indicator, the liquid assets-to-deposits ratio has also weakened, resonating with the cash reserve trend. This decline, which began in 2013, was briefly offset by the BSP’s historic Php 2.3 trillion liquidity injection but has now resumed its downward trajectory. (Figure 5, topmost diagram)

Other Factors Beyond Cash and Reserves

The slowdown isn’t limited to cash reserves.

Deposit growth has also decelerated since 2013, despite reaching record highs in peso terms. Ironically, a robust 12.7% rebound in bank lending growth (excluding interbank loans and repos) in 2024, which should have spurred deposit growth, failed to translate into meaningful gains. Peso deposits grew by just 7% in 2024. (Figure 5, middle pane)

The question arises: where did all this money go?

This brings attention back onto the BSP’s stated goal of "enabling banks to channel funds more effectively toward productive loans and investments." This growing divergence between total loan portfolio growth and peso deposit expansion in the face of RRR cuts—20% before March 2018, now down to just 7% last October—raises further questions about its effectiveness in boosting productive lending and investment.

A Deeper Liquidity Strain: Rising Borrowings

Adding to signs of the increasing liquidity stress, bank borrowings hit an all-time high in 2024, both in gross and net terms. (Figure 5, lowest graph)

Figure 6

Total borrowings surged by Php 394.5 billion, pushing outstanding bank debt to a record Php 1.671 trillion.

More importantly, the focus of borrowing was in bill issuance, which accounted for 65% of total bank borrowings in 2024 (!)—a strong indicator of tightening liquidity. (Figure 6, topmost image)

If banks are highly profitable and NPLs are not a major issue, why are they borrowing so aggressively and requiring additional RRR cuts?

The liquidity squeeze cannot be attributed solely to RRR levels alone—otherwise, the 2018–2020 cut from 20% to 12% should have stemmed the tide.

V. Liquidity Drain: Record Investment Risks and Elevated Marked-to-Market Losses

There’s more to consider.

Beyond lending, bank investments—another key bank asset class—also hit a record high in peso terms in 2024.

Yet, despite lower fixed-income rates, banks continued to suffer heavy losses on their investment portfolios: Accumulated investment losses stood at Php 42.4 billion in 2024, after peaking at Php 122.85 billion in 2022. (Figure 6, middle diagram)

Banks have now reported four consecutive years of investment losses.

These losses undoubtedly strain liquidity, but what’s driving them?

The two primary investment categories—Available-for-Sale (AFS) and Held-to-Maturity (HTM) securities—accounted for 40% and 52.6% of total bank investments, respectively.

Accumulated losses likely stem from AFS positions, reflecting volatility in equity, fixed-income, foreign exchange, and other trading activities.

VI. Despite Falling Rates, Bank’s Held-to-Maturity Assets Remain Near Record High

Interestingly, despite easing fixed-income rates, HTM assets remained close to their all-time high at Php 3.95 trillion in December 2024, barely below the December 2023 peak of Php 4.02 trillion.

Since January 2023, HTM holdings have hovered tightly between Php 3.9 trillion and Php 4 trillion.

Government Financing and Liquidity Risks

Yet, this plateau may not persist.

Beyond RRR cuts, the banking system’s Net Claims on Central Government (NCoCG) surged 7% to a new high of Php 5.541 trillion in December 2024.

Per BSP: "Net Claims on CG include domestic securities issued by, and loans extended to, the central government, net of liabilities such as deposits."

While this is often justified under Basel III capital adequacy measures, in reality, it functions as a quasi-quantitative easing (QE) mechanism—banks injecting liquidity into the financial system by financing the government.

The likely impact?

The losses in government securities are categorized as HTMs, effectively locking away liquidity.

BSP led Financial Stability Coordination Council (FSCC) noted in their 2017 Financial Stability Report in 2018 that: "Banks face marked-to-market (MtM) losses from rising interest rates. Higher market rates affect trading since existing holders of tradable securities are taking MtM losses as a result. While some banks have resorted to reclassifying their available-for-sale (AFS) securities into held-to-maturity (HTM), some PHP845.8 billion in AFS (as of end-March 2018) are still subject to MtMlosses. Furthermore, the shift to HTM would take away market liquidity since these securities could no longer be traded prior to their maturity" (bold mine)

Curiously, discussions of HTM risks vanished from BSP-FSCC Financial Stability Reports after the 2017 and 2018 H1–2019 H1 issues.

VII. Moral Hazard and the "COVID Bailout Playbook"

Although NCoCG has been growing since 2015, banks accelerated their accumulation of government securities as part of the BSP’s 2020 pandemic rescue package.

Are banks aggressively lending to generate liquidity solely to finance the government? Are they also using government debt to expand the collateral universe for increased lending? Government debt is also used as collateral for interbank loans and repo transactions.

Have accounting regulations—such as HTM—transformed into a silo that shields Mark-to-Market losses?

The growth of HTM has aligned with NCoCG. (Figure 6, lowest chart)

While this may satisfy Basel capital adequacy requirements, ironically, it also exposes the banking system to investment concentration risk, sovereign risk, and liquidity risk.

This suggests that reported bank "profits"—likely inflated by subsidies and relief measures—are overshadowed by a toxic mix of trading losses, HTM burdens, and potentially undeclared or hidden NPLs.

These pressures have likely forced the BSP to aggressively cut RRR rates.

As anticipated, authorities appear poised to replicate the COVID-era bailout playbook, which they view as a success in averting a crisis.

The likely policy trajectory template includes DIRECT BSP infusions via NCoCG, record fiscal deficits, further RRR and policy rate cuts, accelerated bank infusions NCoCG, a higher cap on the USD/PHP exchange rate, and additional subsidies and relief measures for banks.

This is unfolding before us, one step at a time.

VIII. The Bigger Picture: Are We Headed for a Full-Blown Crisis?

Given the moral hazard embedded in this bailout mindset, banks may take on excessive risks, exacerbating "frictions in financial intermediation". Debt will beget more unproductive debt. "Ponzi finance" risks will intensify heightening liquidity constraints that could escalate into a full-blown crisis.

Further, given the banking system’s fractional reserve operating framework, riskier bank behavior, whetted by reduced cash buffers, heightens the risks of lower consumer confidence in the banking system—which translates to a higher risk of a bank run.

The Philippine Deposit Insurance Corporation (PDIC) reportedly has funds to cover 18.5% of insured deposits, or P3.53 trillion, as of 2023.

So, with the RRR cuts, is the BSP gambling with this?

IX. Conclusion: RRR Cuts a High-Risk Strategy?

BSP’s statistics cannot be fully relied upon to assess the true health of the banking system.

1. The decline in non-performing loans (NPLs) is inconsistent with slowing economic growth and the deflationary spiral in the real estate sector. Likewise, falling NPLs contradict the ongoing liquidity pressures faced by banks.

2. Evidence of these liquidity strains is

clear: bank borrowings have surged to record levels, with bill issuances

dominating the market. The BSP’s RRR cuts only reinforce the mounting liquidity

constraints.

3. Beyond lending, banks have turned to

investments to strengthen their balance sheets—including supporting the

Philippine Stock Exchange (PSE), even as asset prices have become increasingly

misaligned with corporate earnings.

4. In a bid to further boost systemic liquidity, implied quantitative easing (QE) spiked to an all-time high in December, which will likely translate into a higher volume of Held-to-Maturity (HTM) assets.

Through aggressive RRR cuts, is the BSP taking a high-risk approach merely to uphold its statistical narrative?

No comments:

Post a Comment