This is the same mentality that drives every sovereign debt crisis. Governments become disconnected from the source of their funding. They begin treating taxpayer money as an unlimited resource rather than the product of someone else’s labor. Every expenditure can be justified. Every program becomes essential. Every privilege becomes a necessity. Meanwhile, the national debt continues to rise—Martin Armstrong

In this issue

Stagflation Part 11: The Intervention Ecosystem Behind

Moody's and Fitch's Banking Warnings

Part 1: The Ratings Agencies Finally Catch Up

Part 2: The Political Economy of the Intervention

Ecosystem

2A. Basel, Sovereign Debt, and the

Savings-Investment Gap

2B. Five Relief Measures, One Intervention

Regime

2C. Confidence Management: BSP Rebuts Fitch

2D. Policies Are Never Neutral

2E. The Feedback Mechanism Begins to Fail

Part 3: Wile E. Coyote Begins to Lose Altitude

3A. Sovereign-Bank Doom Loop: Financing the

State Before Financing the Economy

3B. The Hidden Losses Continue to Grow

3C. Liquidity Reveals What Capital Ratios

Conceal

3D. Deposits Rise—But Why?

3E. Funding Conditions Become Increasingly

Demanding

Part 4: Conclusion: The Balance Sheet Speaks

Stagflation Part 11: The Intervention Ecosystem Behind Moody's and Fitch's Banking Warnings

Moody's and Fitch have finally caught up. The balance sheet explains why.

Part 1: The Ratings Agencies Finally Catch Up

Within days, the world's two largest credit-rating agencies issued successive warnings on the Philippine banking system.

Moody's first revised its outlook on Philippine banks to ‘Negative’, citing weakening household consumption, softer loan demand, rising credit impairments, and slowing government spending.

Days later, the agency issued a second warning, describing the BSP's latest capital-relief measure as ‘credit negative’, arguing that excluding unrealized losses on government securities from regulatory capital calculations reflected increasing balance-sheet pressures rather than genuine strengthening.

Notably, the warning represented a marked shift from Moody's assessment only months earlier, when the agency viewed the BSP's capital-relief measures more favorably. The reversal illustrates how rapidly external assessments can change once balance-sheet vulnerabilities become more difficult to ignore.

Fitch Ratings soon followed.

It downgraded its outlook on Philippine banks from ‘Neutral’ to ‘Deteriorating,’ warning that slower economic activity, rising credit costs, rapid unsecured consumer lending, and weakening profitability would increasingly pressure the sector. Earlier, Fitch had also revised the Philippine sovereign outlook to Negative, citing slower public spending, fiscal deterioration, and the inflationary consequences of higher oil prices.

Both agencies have finally acknowledged stresses that balance-sheet data, market behavior, and this series have documented for years.

Ironically, neither Moody's nor Fitch identified the gradual deterioration while it was unfolding. Instead, both reacted only after a series of highly visible developments—including the Middle East oil shock, concerns over public spending associated with the corruption investigation, the persistent rise in Philippine Treasury yields, and the deterioration in bank share prices—made the underlying fragilities increasingly difficult to ignore.

This pattern is not an isolated shortcoming. It reflects the institutional character of modern credit-rating agencies.

Major rating agencies—Moody's, Fitch, and S&P—operate under an issuer-pays business model that embeds a persistent principal-agent problem. They are compensated by the very institutions whose creditworthiness they evaluate, making their commercial incentives structurally dependent on maintaining long-term issuer relationships. At the same time, their reputations depend on avoiding assessments that diverge too sharply from prevailing market consensus before the evidence becomes widely accepted. Ratings that prove prematurely pessimistic risk damaging institutional credibility, while ratings that move alongside emerging market consensus are considerably easier to defend ex post. The resulting incentive structure favors gradual convergence rather than early diagnosis of structural deterioration.

The 2008 Global Financial Crisis remains the clearest illustration. Rating agencies assigned investment-grade ratings to mortgage-backed securities even as the quality of their underlying collateral deteriorated. Subsequent investigations concluded that the combination of the originate-to-distribute model and issuer-paid ratings systematically weakened independent credit assessment, allowing confidence to persist until the financial system itself became unstable.

The Philippine experience exhibits similar characteristics.

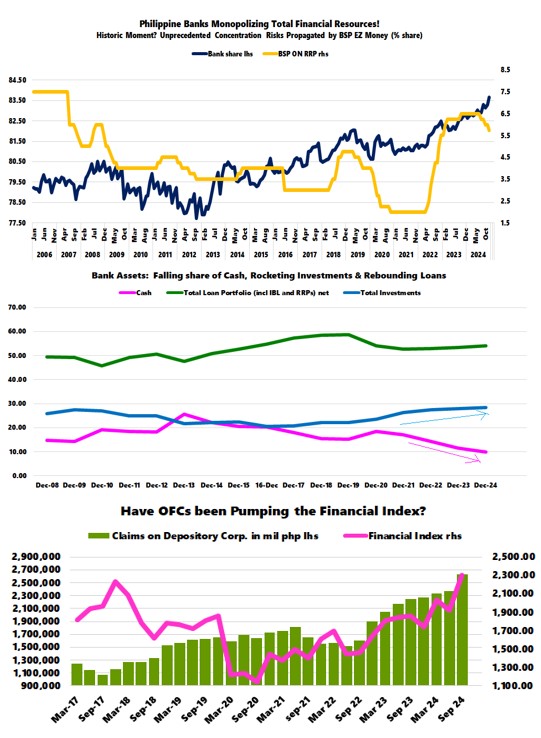

For years, Philippine bank profitability had already begun slowing. Profit growth peaked around the second quarter of 2021 before entering a prolonged deceleration. Yet the PSE Financial Index continued advancing, reaching its cyclical peak only in March 2025. The divergence between weakening earnings momentum and rising market valuations reflected an expanding disconnect between underlying fundamentals and market expectations.

Figure 1

The eventual reversal should not have been surprising.

Today, both profit growth and the Financial Index are declining as market valuations gradually converge toward balance-sheet realities that had long been obscured by abundant liquidity, optimistic narratives, expectations of continued policy accommodation, and price support originating from large financial institutions. (Figure 1, topmost pane)

The phenomenal rise in the Financial Index from September 2020 to March 2025, largely reflected appreciation in its dominant constituents. As of late June 2026, BDO, BPI, and Metrobank accounted for nearly four-fifths of the index's market capitalization, making movements in a handful of banks sufficient to sustain the appearance of sectoral strength. Although they comprised less than one-fifth of the PSEi 30 (also as of late June), their size and influence made them likewise important contributors to the performance of the headline index.

During much of the previous bull market, other financial corporations (OFCs) also played a material role in supporting banking share prices, further weakening the informational content of market prices.

OFC claims on depository corporations rose broadly in tandem with the Financial Index, suggesting that expanding OFC financing helped support bank share prices. However, after reaching a record high in the fourth quarter of 2025, OFC claims began to diverge from the Financial Index beginning in the first quarter of 2025, indicating that this source of support had begun to weaken. (Figure 1, middle image)

With the Financial Index declining throughout 2025, however, market valuations began adjusting before the rating agencies revised their assessments.

Their recent actions therefore represent confirmation rather than discovery. The warnings validate developments that had already become evident in BSP statistics, in the progressive deterioration of bank profitability, in weakening banking-equity/Financial Index performance, and in the increasingly frequent policy accommodations undertaken by the BSP.

This distinction is fundamental because it separates empirical description from causal explanation. Rating agencies describe conditions once they become sufficiently visible. They do not explain why those conditions emerged.

The factors emphasized in the recent downgrades—higher oil prices, slower government spending, weaker household demand, and rising credit costs—are undoubtedly relevant. But they function primarily as catalysts rather than causes.

Philippine banking-sector fragility did not originate with the latest geopolitical shock, nor did it suddenly emerge because of corruption investigations or weaker fiscal spending. Those developments merely exposed vulnerabilities that had accumulated over many years through policy choices, regulatory incentives, and increasingly interventionist financial arrangements.

Understanding that process requires moving beyond current events toward the institutional framework governing Philippine finance. The common thread connecting slowing profitability, declining liquidity buffers, record sovereign exposures, repeated BSP capital-relief measures, and successive rating-agency warnings is not the latest external shock.

It is the cumulative consequence of a policy regime that has increasingly substituted intervention for adjustment.

Modern central-bank intervention is no longer a collection of isolated policies. It has become an ecosystem. Understanding that ecosystem—not merely its latest manifestations—is the central objective of this essay.

Part 2: The Political Economy of the Intervention Ecosystem

If Part 1 established that Moody's and Fitch merely recognized Philippine banking stress after it had become increasingly visible, the more important question remains unanswered.

Why has the banking system become progressively dependent on successive regulatory accommodations in the first place?

The answer cannot be found in the recent oil shock, the corruption investigation, or slowing GDP growth. Those developments merely exposed vulnerabilities that had accumulated over many years.

The deeper explanation is institutional.

The Philippine banking system has gradually evolved into an intervention ecosystem in which fiscal policy, monetary policy, prudential regulation, and financial markets increasingly reinforce one another. The result is a self-reinforcing sovereign-bank nexus, where interventions introduced to alleviate one problem progressively create the conditions requiring the next.

2A. Basel, Sovereign Debt, and the Savings-Investment Gap

The BSP's latest relief measures did not emerge in isolation.

Their foundations were laid years earlier.

Modern prudential regulation under the Basel framework assigns highly preferential regulatory treatment to sovereign obligations. Government securities generally receive lower regulatory capital charges while simultaneously qualifying as high-quality liquid assets for liquidity requirements.

Banks responded accordingly.

As fiscal deficits widened and the domestic savings-investment gap persisted, government borrowing increasingly flowed through the banking system. Philippine banks accumulated record holdings of government securities, which now comprise roughly one-third of total banking assets—the highest in Asia, while debt securities classified under amortized cost likewise reached unprecedented levels. (Figure 1, lowest graph)

Note: The share reported here differs from the roughly 30% figure cited elsewhere because of differences in measurement. This chart uses net claims on the central government as a share of total banking-system assets, whereas other sources often report total holdings of government securities (or include broader public-sector claims) as a share of assets. Although the definitions differ, both measures point to the same underlying trend: Philippine banks have become increasingly exposed to sovereign debt.

The arrangement appeared mutually beneficial while interest rates remained exceptionally low. Governments obtained inexpensive financing. Banks benefited from favorable regulatory treatment. Reported capital ratios remained strong. Expanding sovereign portfolios came to be viewed as evidence of prudence rather than concentration.

Yet policies are never neutral.

The same incentives that encouraged banks to finance government deficits also concentrated duration risk on bank balance sheets. Once long-term interest rates began rising, unrealized losses accumulated almost inevitably.

The present mark-to-market problem therefore did not originate with the recent rise in Treasury yields. Higher yields merely exposed vulnerabilities embedded years earlier through regulatory incentives and reinforced by persistent fiscal dependence on the banking system.

Viewed through this lens, today's banking pressures are not an isolated financial event. They are the institutional consequence of a prolonged policy regime.

2B. Five Relief Measures, One Intervention Regime

Against this backdrop, the succession of recent BSP interventions becomes considerably more revealing.

Figure/Table 2

Within only a few months, regulators and the National Government implemented a remarkable sequence of accommodations. (Figure/Table 2)

Following Executive Order No. 110 and the declaration of a National Energy Emergency, in April, banks received temporary regulatory relief allowing affected loans to avoid immediate non-performing classification while repayment schedules for agricultural borrowers were extended.

The government subsequently lengthened salary-loan maturities to as much as seven years, reducing immediate repayment burdens while extending household leverage further into the future.

The BSP introduced a Positive Neutral Countercyclical Capital Buffer framework, permitting banks to draw down previously accumulated capital during periods of stress.

Regulators also revised rules governing intragroup guarantees and credit-risk transfers to provide greater flexibility in regulatory capital treatment.

Finally, the BSP temporarily excluded unrealized losses on peso-denominated government securities from regulatory capital calculations, preventing mark-to-market losses from immediately reducing reported Common Equity Tier 1 ratios.

The pattern of interventions is clear. As banking-sector pressures emerge, authorities increasingly respond through regulatory accommodation rather than balance-sheet adjustment.

- Accommodation postpones adjustment.

- New pressures subsequently emerge.

- Additional accommodations follow.

Intervention increasingly becomes the primary mechanism through which adjustment itself is managed.

Intervention thus evolves from a temporary response into a self-reinforcing mechanism that perpetuates the need for further intervention.

This is precisely why Moody's second warning deserves closer attention.

Ironically, while the BSP presented its latest capital-relief measure as supporting financial stability, Moody's characterized the same measure as ‘credit negative.’

The significance lies not in Moody's opinion itself. Rather, the rating agency inadvertently acknowledged what the policy implicitly reveals. If Philippine banks were genuinely as “resilient” as official narratives repeatedly suggest, successive relief measures would be unnecessary.

The interventions themselves become evidence of the underlying condition they are intended to manage.

2C. Confidence Management: BSP Rebuts Fitch

The same pattern emerged following Fitch's decision to revise its outlook on the Philippine banking sector to "deteriorating." Rather than engaging the underlying balance-sheet concerns raised by Fitch—slowing profitability, rising credit costs, deteriorating consumer-credit quality, and mounting macroeconomic risks—the BSP issued an official rebuttal emphasizing the banking system's resilience, strong capitalization, and prudent supervision.

The response illustrates another dimension of the intervention ecosystem: confidence management.

Financial stability increasingly depends not only on liquidity facilities and regulatory accommodation but also on sustaining confidence through official communication, supervisory discretion, accounting treatment, statistical embellishments, market-price support, and managing information.

Here one is reminded of Otto von Bismarck's famous observation:

"Never believe anything in politics until it has been officially denied."

The quotation need not be interpreted literally. Rather, it illustrates a broader principle: official denials often reveal where authorities perceive the greatest political or financial vulnerability. Communicative reassurance, when accompanied by repeated intervention, creates its own internal contradiction.

Demonstrated preference in motion: Actions ultimately reveal more than statements.

If the banking system is indeed as resilient as repeatedly claimed, the growing sequence of relief measures, accounting accommodations, capital waivers, repayment extensions, and supervisory flexibility becomes increasingly difficult to reconcile with that narrative.

As a whole, Moody's first warning, Moody's second warning, Fitch's deteriorating outlook, and the BSP's official rebuttal are best understood not as separate news events but as different responses to the same underlying balance-sheet reality.

2D. Policies Are Never Neutral

Modern intervention rarely operates through monetary policy alone. To remain effective, it increasingly extends into prudential regulation, accounting treatment, supervisory discretion, statistical presentation, market-price support, and official communication. The objective gradually shifts from correcting underlying imbalances toward preserving confidence despite those imbalances.

Confidence, however, is not synonymous with resilience.

Market prices, capital ratios, official statistics, and regulatory classifications increasingly become components of a broader architecture of confidence management.

This recalls the argument developed in Stagflation Part 9 regarding statistical simulacra. Confidence management increasingly involves directing public attention toward officially presented indicators while managing information about underlying conditions.

Policies are never neutral.

Every policy accommodation redistributes costs and benefits while reshaping future incentives. Banks carrying substantial unrealized losses receive capital relief. Governments retain easier access to domestic financing. Institutions that managed liquidity and duration risk more conservatively receive comparatively fewer advantages. The public receives progressively less transparent balance sheets, while future taxpayers inherit greater contingent liabilities, capital is consumed, and the purchasing power of money erodes.

Perhaps more importantly, repeated accommodation alters expectations.

When losses repeatedly receive regulatory relief, incentives increasingly favor postponement over recognition. When accounting treatment becomes progressively more flexible, opportunities for accounting arbitrage naturally expand. When capital requirements become adjustable, pressure to raise fresh equity correspondingly diminishes.

Policies influence behavior because they alter the expected rewards and penalties facing economic actors.

As the great Ludwig von Mises argued, intervention possesses its own internal logic. Each intervention generates distortions that subsequently justify additional intervention.

Historian Charles Kindleberger's sauve qui peut similarly reminds us that periods of financial stress intensify incentives to preserve appearances, transfer adjustment elsewhere, and ultimately culminate in what he famously described as the "emergence of swindles."

Economist János Kornai's soft-budget constraint explains how repeated accommodation gradually conditions institutions to expect further accommodation, thereby entrenching dependence on future intervention.

As one, these perspectives describe how policy reshapes the political economy. The intervention ecosystem does not merely postpone adjustment. It alters the adaptive behavior of the financial system itself.

2E. The Feedback Mechanism Begins to Fail

Perhaps the greatest cost of repeated intervention is not its immediate fiscal expense or temporary accounting opacity.

It is the gradual deterioration of the market's feedback

mechanism.

- Markets are increasingly managed to produce an optic of stability.

- Prices become less informative.

- Balance sheets become more difficult to manage and interpret.

- Statistics increasingly reflect administrative treatment more than the underlying economic reality.

- Capital allocation responds progressively more to regulation than entrepreneurship.

Meanwhile, scarce domestic savings continue flowing toward sustaining existing politically induced structures rather than financing new productive investment.

Austrian economist Frank Shostak's observation becomes increasingly relevant. Fiscal and monetary rescue measures appear effective only while supported by an adequate stock of genuine private savings. As real savings become progressively constrained, successive interventions generate diminishing economic benefits while simultaneously increasing distortions and fragility.

In this sense, intervention gradually begins consuming the very foundation upon which it depends.

If this diagnosis is correct, its consequences should already be visible in the Philippine banking system's balance sheet.

The April and May BSP data suggest precisely that.

Part 3: Wile E. Coyote Begins to Lose Altitude

For several years, Philippine banking has what I have aptly described through the metaphor of Wile E. Coyote.

The analogy remains instructive.

A cartoon character running beyond the edge of a cliff continues forward motion until gravity is finally acknowledged. Momentum temporarily sustains the illusion of stability, even after structural support has disappeared.

The same dynamic has characterized Philippine bank lending.

For much of the previous cycle, rapid loan expansion repeatedly outpaced the growth of non-performing loans, producing the appearance of stable asset quality through what we previously described as a denominator effect. As long as total lending grew faster than impaired assets, reported ratios remained contained, masking underlying deterioration.

Eventually, however, arithmetic reasserts itself.

The May data suggest that this transition may now be

underway.

Figure 3

Gross non-performing (NPL) loans rose 14.0 % year-on-year, outpacing total loan growth of approximately 11.9 %. As a result, the gross NPL ratio continued its steady ascent—from 3.29 % in March to 3.37 % in April and 3.44% in May. (Figure 3, topmost window)

Gross NPLs (in pesos) also reached a new record for the second consecutive month.

The denominator is no longer keeping pace.

Wile E. Coyote is beginning to feel gravity.

Loan-loss reserves likewise reached record levels in peso terms. However, provisioning continues to lag overall loan expansion, suggesting that while buffers are increasing, they are not rising fast enough to fully offset the growth of risk exposures. (Figure 3, middle diagram)

The deterioration therefore extends beyond headline ratios. It is increasingly embedded in the structure of the balance sheet itself.

3A. Sovereign-Bank Doom Loop: Financing the State Before Financing the Economy

The asset side of bank balance sheets reinforces the same structural shift.

Net claims on the central government (NCoCG) reached another record in April, while holdings of debt securities (mostly government) under amortized-cost classifications (formerly Held-to-Maturity or HTM) also hit a milestone last May. (Figure 3, lowest chart)

This is not incidental.

Under Basel-aligned prudential frameworks, sovereign obligations receive preferential regulatory treatment through lower capital charges and favorable liquidity classification. Banks responded exactly as incentives dictated.

Over time, this has resulted in a gradual but persistent reallocation of bank balance sheets toward sovereign financing.

Government borrowing increasingly absorbs domestic savings that might otherwise have supported private-sector credit formation. The banking system, in effect, has become a primary intermediary of fiscal financing.

The result is not merely concentration risk.

It is a structural transformation of intermediation itself—from financing entrepreneurial activity to financing the state.

In this configuration, the savings–investment gap is increasingly mediated through public debt rather than private capital formation.

The implication is straightforward: sovereign funding needs and bank balance-sheet structure become progressively intertwined, with each reinforcing the other over time.

Or, this dynamic evolves into a sovereign-bank doom loop: banks’ balance sheets become increasingly saturated with sovereign risk, while the state becomes progressively dependent on domestic banks for financing. Each side reinforces the other, tightening the link between fiscal conditions and banking-sector stability.

Sovereign risk becomes bank risk, and vice versa.

3B. The Hidden Losses Continue to Grow

The second channel of stress is less visible but equally

important.

Figure 4

Available-for-sale (AFS) portfolios reached its second highest level in May, while unrealized losses rose to approximately Php 175 billion—exceeding the valuation losses recorded during the post-pandemic inflation shock following the Russia–Ukraine conflict. (Figure 4, upper graph)

This unparalleled deterioration coincided with a sharp rise in Philippine Treasury yields. Yet, while 10-year yield spiked to the same level as 2022, the losses were much greater today. (Figure 4, lower image)

The mechanism is direct.

As yields rise, the market value of existing government securities declines. Given the unprecedented share of sovereign instruments on bank balance sheets, this translates into immediate valuation losses, reduced capital flexibility, and greater sensitivity to further rate movements.

The BSP classifies these losses as temporary volatility.

Economically, however, they are not temporary. They represent the opportunity cost of prior duration decisions shaped by the prevailing regulatory environment.

Capital relief alters their regulatory treatment.

It does not restore the lost economic value. It exacerbates them.

3C. Liquidity Reveals What Capital Ratios Conceal

Asset quality and valuation effects are only part of the picture. Liquidity conditions provide an earlier signal of stress.

Here, the evidence is increasingly consistent.

Figure 5

The cash-to-deposit ratio remains near historic lows despite modest improvement in April. Meanwhile, the liquid-assets-to-deposit ratio continued to weaken, falling to approximately 46.7 % in May—its lowest level since the pandemic period. (Figure 5 upper image)

This is a notable weakening of liquidity buffers.

During the pandemic, extraordinary BSP liquidity injections exceeding Php 2.3 trillion produced an unprecedented expansion in system-wide liquidity. That buffer has since unwound.

Banks now face weakening liquidity conditions even as official narratives continue to emphasize systemic ‘resilience.’

The divergence between narrative and balance-sheet conditions is widening.

3D. Deposits Rise—But Why?

At first glance, deposit growth appears supportive.

Deposit liabilities continued expanding at double-digit rates through May.

However, the source of this growth is crucial.

Broad money (M3) continued to expand at more than 12% annually, even as currency in circulation slowed. At the same time, the BSP’s Monetary Authority Survey (MAS) shows a sharp increase in BSP net claims on the National Government (NCoCG), reaching approximately Php 663 billion last May, largely driven by declining government deposits at the BSP. (Figure 5, lower graph)

In other words, liquidity increasingly entered the banking system through official channels rather than through underlying economic expansion.

The composition of money creation therefore matters as much as its quantity.

Deposit growth driven by public-sector liquidity operations is fundamentally different from deposit growth driven by rising productivity, voluntary savings, or private investment.

One reflects economic activities.

The other primarily reflects liquidity redistribution—wealth consumption concealed beneath a façade of sanguine statistics.

3E. Funding Conditions Become Increasingly Demanding

The liability side of bank balance sheets reinforces the

same pattern.

Figure 6

Bonds and bills payable rose to nearly Php 2 trillion, the second highest levels on record. (Figure 6, upper visual)

Banks have increasingly relied on wholesale funding, while interbank borrowing has remained volatile and reverse-repurchase activity has fluctuated sharply over the interim—though both are on an uptrend overtime. (Figure 6, lower chart)

These developments indicate a gradual shift toward more expensive and less stable funding sources.

Banks are increasingly competing with the National Government and the private sector for access to scarce domestic savings, placing upward pressure on funding costs.

Like asset composition, funding structure reflects the evolving incentive environment facing the banking system.

Part 4: Conclusion: The Balance Sheet Speaks

The evidence, viewed collectively, is difficult to dismiss.

- Record sovereign exposure.

- All-time high amortized-cost securities.

- Biggest unrealized bond losses.

- Record non-performing loans in pesos.

- Milestone lows liquidity buffers.

- Increasing reliance on wholesale funding.

In aggregate, they portray a banking system operating with progressively narrower margins of safety despite successive rounds of regulatory accommodation.

This is why Moody's and Fitch should be understood as confirming rather than discovering emerging stress.

The ratings agencies did not originate the signal. They merely acknowledged conditions that had already become visible in bank balance sheets, market prices, and the increasingly frequent interventions undertaken by policymakers.

More fundamentally, the recent downgrades reveal the limits of confidence management.

- Regulatory relief can postpone recognition.

- Accounting flexibility can soften reported capital ratios.

- Official reassurance can influence expectations.

But none can permanently suspend the underlying economics of deteriorating asset quality, mounting sovereign exposure, or tightening liquidity conditions.

Policies are never neutral. They reshape incentives, redistribute risks, and influence how financial institutions adapt over time. Successive interventions may stabilize the system temporarily, but they also deepen institutional dependence on future intervention, reinforcing the very dynamics they seek to contain.

The Philippine banking system did not arrive at its present condition because of a single oil shock, corruption investigation, or ratings downgrade. Those events merely exposed vulnerabilities that had accumulated over years through the interaction of fiscal policy, monetary accommodation, prudential regulation, and repeated financial intervention.

Ultimately, the ratings agencies reacted to the symptoms.

The balance sheet reveals the disease.

- Markets can postpone reality.

- Accounting can defer recognition.

- Regulation can delay adjustment.

But none can permanently suspend economic constraints.

Eventually, the chickens come home to roost.

____

References:

Stagflation Part 9: The Good News Mirage — Statistical Stability Amid Structural Fragility

Stagflation Then and Now: Why Philippine

Markets Are Repricing Like the 1970s (Part 4)

Stagflation by Design: Policy Contradictions and the Return of the Pandemic Rescue Playbook

Stagflation Is Already Here—Emergency Policies Are Now Entrenching It

Seed Article