The total wealth of a

country is the total value of goods and services it produces. When real estate

prices rise much faster than this value, there has effectively been a large

wealth transfer from those who don't own real estate to those who do—Michael

Pettis

In

this issue:

Q3 2024: Philippine Real Estate Enters Deflationary Spiral

Post-Pandemic Recession!

I. Q3 2024: Philippine Real Estate Sees First Deflationary

Spiral Since the Pandemic Recession!

II. A Brief Insight into the Differences Between

Pandemic-Recession Real Estate Deflation and Today’s Economic Landscape

III. Despite Declines in New Housing Loans, Total Real Estate

Consumer and Supply-Side Loans Surge, Unaffected by High Cap Rates

IV. Real Estate’s Falling

GDP Contribution and Increased Bank Lending Share Point to Heightened

Concentration Risks

V. Q3 2024 Real Estate Deflation Means Lower Sectoral and

National GDP; Slower Retail Sales Amidst Greater Supply Side Expansion

Translates to More Vacancies

VI. Real Estate Deflation Amidst Near Full-Employment? What

Happens When Unemployment Soars?

VII. Property Sector Woes: From Price Deflation to Income

Losses and Increased Debt Loads

VIII. Property Sector Woes: From Liquidity Strains to Soaring

Bank NPLs?

IX. Will the BSP Launch QE 2.0 Soon?

X. Conclusion: Two Ways to Bankruptcy: Gradually, then Suddenly

Q3 2024: Philippine Real Estate Enters Deflationary Spiral

Post-Pandemic Recession!

Philippine

real estate prices experienced their first deflationary spiral in Q3 2024 since

the pandemic recession, highlighting worsening imbalances in the sector. We

explore the potential economic implications and possible policy responses.

I. Q3 2024: Philippine Real Estate Sees First Deflationary

Spiral Since the Pandemic Recession!

The

Philippine consumer economy is hurting—and hurting badly.

This

pain is being reflected across several fronts, including the country’s most

popular investment: real estate.

Businessworld, December 30: HOUSING

PRICES nationwide declined in the third quarter, the first

contraction in over three years, data from the Bangko Sentral ng

Pilipinas (BSP) showed. The Residential Real Estate Price Index (RREPI) fell by

2.3% year on year in the July-to-September period. This was a reversal of the

2.7% growth in the second quarter and 12.9% expansion in the same period a year

ago. This was also the first time the RREPI posted a decline since the 9.4%

drop recorded in the second quarter of 2021. (bold added)

And

more news excerpts (all bold mine)

GMANews.com December 12, 2024: The

oversupply of condominium units has shot up to an equivalent of 34 months as

of November amid the sudden increase in availability of units, according to

data released by Leechiu Property Consultants (LPC)… There

were 4,971 new units launched in October and November, versus the 4,375 units

sold during the period. Year-to-date, condominium take up was recorded at

25,565 units, equivalent to 63% of that recorded in the comparable period of

2023 while project launches stood at 13,226 or half of the previous year. Golez

earlier also noted that the oversupply was due to a mix of high interest

rates and external concerns, as well as a shift in preference to

single-detached homes and properties in nearby provinces.

Inquirer.net November 16, 2024: Vacancies

in Metro Manila’s prime and grade A office market hit a 20-year high as of the

end of the third quarter this year, with rental rates declining for the fourth

straight quarter. A report from global commercial real estate services firm

Cushman and Wakefield puts the average office vacancy rate at 18.2 percent, the

highest since the second quarter of 2004. “The Metro Manila office market is

exhibiting a slower-than-expected recovery in Q3 2024,” Cushman & Wakefield

director and head of tenant advisory group Tetet Castro said in a statement.

Businessworld, November 12, 2024: DEMAND

for office space outside Metro Manila has been “less robust” as office

occupiers now have smaller space requirements, real estate

services firm JLL Philippines said. “After the pandemic, I think the demand

has weakened in general because for the key cities outside Metro Manila

like Cebu and Iloilo, we’re still seeing a bit of takeup, but for the other

peripheral areas, it’s not as robust anymore,” JLL Philippines Head of

Research and Strategic Consulting Jan-Loven C. de los Reyes said at a briefing

last week…

Businessworld, October 30, 2024: THE

OFFICE VACANCY rate in Metro Manila is projected to reach 20.5% by the end

of the year, driven by the influx of new office space and the departure of

Philippine offshore gaming operators (POGOs), according to property consultancy

firm Colliers Philippines…As of the end of the third quarter, Colliers data

showed that office space vacancy rose to 18.6% from 18.3% the previous quarter

due to space resulting from POGO lease terminations and non-renewal of

pre-pandemic leases.

My Initial Insights:

1. Polls indicate that the challenges faced

in Q3 are likely to extend throughout the rest of 2024 and beyond.

2. Mounting mismatches between

weakening demand and rising supply have led to either increasing vacancies

or a glut.

3. Even the most bullish industry advisors

have been forced to admit or confront the harsh reality facing the

sector. However, they often put on a cosmetic face or a polished façade,

promoting hope of recovery with little explanation beyond reliance on

GDP growth.

4. While real estate prices may seem

"sticky," they are actually sensitive to liquidity and interest

rates. Consequently, price declines reflect intensifying liquidity strains. In

other words, vacancies have drained liquidity from many leveraged landlords

and real estate owners, forcing them to sell properties at lower prices.

5. The inflationary boom has morphed into

a deflationary bust, where fear has replaced greed.

6. Mainstream thinking has consistently

overlooked the root of the issue: trickle-down policies that foster a

"build-and-they-will-come" ideology, relying on the assumption of

perpetual credit-driven demand fueled by low inflation and interest rates-or an

everlasting regime of easy money.

Although we have been addressing this topic

for some time, I will be quoting extensively from my May 2023 article: (bold and italics original)

There has been little

realization that the industry has invested primarily in the foundation of the

so-called "integrated community structure," anchored on urbanization

and its extension of "satellite communities."

Espousing the

contortion of Say's Law, "supply creates its own demand," through

"build and they will come," the race to build became the industry’s

bedrock.

Yet, the dynamic

preference of consumers became one of the challenges of this model.

And so, influenced by

digitalization and pandemic policies, the transformation to

hybrid/remote work has rendered a massive "sunk cost" or capital

decumulation—signified by oversupply.

…

The thing is, though

office spaces are the concern here, all other segments of the property sector

constitute part of such "integrated communities," which therefore

extrapolates to interconnection.

By extension, it also

means that the paradigm of "integrated community" is codependent not

only on the vibrancy of the office properties but also residential, shopping

malls, hotels, logistics and commercial hubs, and other related structures.

Indeed, the dilemma

of the office segment, the weakest link of the commercial real estate sector

(CRE), should spread to other areas.

Aside from the

misallocation of capital, financing these imbalances through debt signifies a

double whammy or the acceleration of capital consumption.

The point having been

made, these clusters of entrepreneurial errors are products of the distortion

of money via the BSP's easy money regime.

II. A Brief Insight into the Differences Between

Pandemic-Recession Real Estate Deflation and Today’s Economic Landscape

Here’s

a deeper dive into this developing seismic event.

The

first article noted: "This was also the first time the RREPI posted a

decline since the 9.4% drop recorded in the second quarter of 2021."

Figure

1The

last time deflation plagued the BSP’s Real Estate Price Index was in Q3 2020

(-0.4%), Q1 2021 (-4.2%), and Q2 2021 (-9.4%). (Figure 1, upper window)

However,

the difference between then and now is that policymakers responded to the

pandemic-induced economic shutdown that led to five consecutive quarters of GDP contraction—a full-blown

recession with aggressive measures.

Authorities

reacted to this unprecedented disruption with a record fiscal deficit.

Simultaneously, the BSP flooded the banking system with a historic Php 2.3 trillion of liquidity, aggressively cut interest rates to historic lows (2% from November 2020 to April 2022), significantly reduced the banking system’s Reserve

Requirement Ratio (RRR) from 14% to 12%,

implemented unprecedented capital, operational, and regulatory relief measures and subsidies, and placed a cap on the US dollar-Philippine peso exchange rate. The Finance Chief even ordered the SSS and GSIS to buy stocks and

support the PSEi 30.

All

these collective actions were taken to prevent credit deflation and support

collateral values—which back bank-issued loans—by reflating the

bank-dominated financial system.

Fast

forward to today, there has been no recession yet. Despite elevated interest

rates, bank credit flows have been oozing.

III. Despite Declines in New Housing Loans, Total Real Estate

Consumer and Supply-Side Loans Surge, Unaffected by High Cap Rates

Still,

the RREPI fell into deflationary territory, led by properties in Metro Manila,

which posted a 14.6% contraction—the second-largest decline since the

18.3% shrinkage in Q2 2021. (Figure 1, lower chart)

Areas

outside the National Capital Region (AONCR) have experienced a sharp slowdown but remain on a growth path.

Importantly,

AONCR was barely affected by deflation during the pandemic era. Given the

recent dynamics, it might not be exempt this time.

Figure

2The

BSP tacitly attributed this turn of events to the shrinking demand for new

housing loans. (Figure 2, topmost table)

In Q3 2024, the number of residential real estate loans

(RRELs) granted for all types of new housing units in the Philippines

contracted by 15.7 percent y-o-y. Specifically, loans granted in the NCR

and AONCR decreased by 20.3 percent and 13.0 percent, respectively. Notably,

the double-digit y-o-y contraction in RRELs in the Philippines, NCR, and

AONCR in Q3 2024 was significant, yet not as severe as the decline in

housing loan availment observed during the pandemic, which began in Q2 2020.

(BSP, 2025) [bold added]

However,

a mere lack of demand for new loans is insufficient to cause a

contraction.

Nevertheless,

theoretically, since real estate prices are duration-sensitive and

influenced by changes in long-term interest rates, these shifts also impact capitalization

rates (cap rates), which in turn affect property values.

Rising

interest rates typically lead to higher cap rates, as investors demand a higher

return to compensate for the increased cost of borrowing and the higher risk

associated with interest rate changes.

Consequently,

higher cap rates generally lead to lower property values, as expected returns

must adjust to match the new rates. Therefore, the adverse impact of higher cap

rates on property values translates to diminished demand from investors.

Notwithstanding

the contraction in new property consumer loans, aggregate real estate consumer loans hit a record high of Php 1.061 trillion in Q3, although its growth rate fell

from 13.5% in Q2 2024 to 8.07%. (Figure 2, middle graph)

On

the supply side, real estate bank loans reached a record Php 2.686 trillion in

Q3 2024, with quarterly YoY growth accelerating from 3.86% in Q2 2023 to 13.9%

in Q3 2024.

In

aggregate, total bank loans (net of interbank lending) rose to a record Php

13.24 trillion, with quarterly YoY growth also accelerating over the past five

quarters.

Thus,

higher cap rates were hardly a factor; instead, the vibrant growth in

supply-side bank lending likely contributed to more

"build-and-they-will-come" supply.

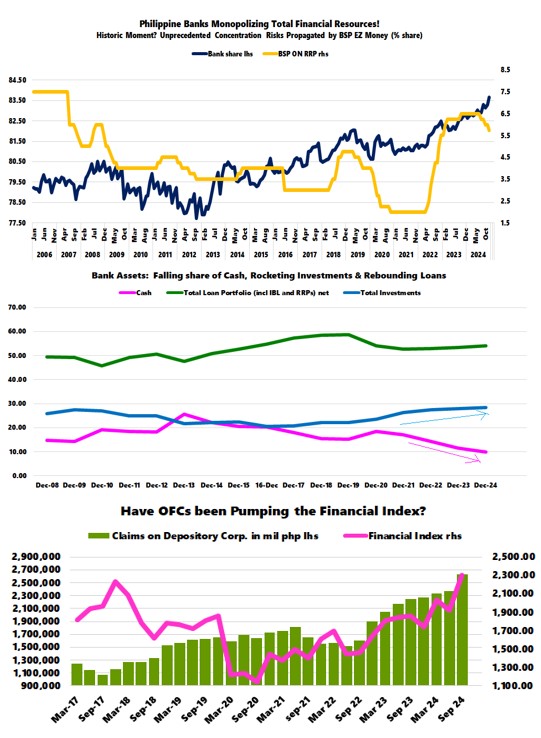

IV. Real Estate’s Falling

GDP Contribution and Increased Bank Lending Share Point to Heightened

Concentration Risks

Furthermore, reports like this can be

misleading: "Banks’ real estate exposure ratio dropped to 19.55% at

end-September from 19.92% at end-June and from 20.55% at the end of September

2023—the lowest real estate exposure ratio recorded in five years, or since the

19.5% level as of September 2019."

This

is because the data on Real Estate Loans (REL) as a share of the Total Loan

Portfolio (TLP) can signify many

things. In this instance, the decline in REL/TLP is not primarily due to

banks lending less to the sector or becoming more judicious or cautious.

Rather, banks have been lending more aggressively to other sectors,

particularly consumer credit cards and salary loans.

In

the realm of consumer loans, the share of real estate loans fell from a record

high of 45.06% in Q4 2021 to 36.4% in Q3 2024, despite record peso real

estate consumer loans. The 8.6% gap was filled by credit cards, which

increased their share from 22.3% in Q4 2021 to 29% in Q3 2024. (Figure

2, lowest diagram)

Meanwhile, the share of salary loans jumped from 8.3% to

13.22% over the same time frame.

In statistics, there are many ways to "skin

a cat."

Unless funds are designated through escrow

accounts, banks have virtually no control over how loan proceeds are

spent. Some of the credit card and salary loans—or even loans declared

for production purposes—could have been diverted to real estate mortgage

payments, property purchases, or even stock investments.

The

fact that real estate credit growth remains buoyant suggests that most of the

borrowed money may have been used for refinancing, with modest amounts

allocated to acquiring second-hand properties (for consumer loans) and

for property development expansion (supply-side loans).

This also tells us that while new buyers

played a smaller role in borrowings, more experienced buyers and property developers

significantly contributed to the sector’s bank borrowings.

On

this note, despite lackluster growth, the real estate sector’s relative

strength—compared to the overall weaker performance of other sectors—prompted a

surge in its share of GDP in

Q3 2024.

The

value-added contribution of the sector, which posted a 5.4% real GDP

growth, amounted to 5.9% of national GDP.

In

the meantime, the real estate sector’s share of Universal-Commercial bank

portfolios amounted to 20.46% in Q3.

Figure 3

Thus, a sector contributing 5.9% of GDP holds

a 20.5% share of UC bank portfolios—representing significant concentration

risks. (Figure 3, topmost chart)

Notably, this is based on the official

definition of the banks’ real estate portfolios, whose actual exposure may

already be understated.

V. Q3 2024 Real Estate Deflation Means Lower Sectoral and

National GDP; Slower Retail Sales Amidst Greater Supply Side Expansion

Translates to More Vacancies

Of

course, we’d also argue that the price deflation in Q3’s RREPI, which indicates

slower spending across the industry, means less than the advertised GDP. Again,

the sector reported 8.8% nominal GDP and 5.4% real GDP. (Figure 3, middle

image)

A

lower real estate GDP should shave off a few more percentage points from Q3’s

GDP of 5.2%.

But

here’s another potential discrepancy: According to the BSP, buyers of new

properties have been less influential in driving demand for real estate.

In

particular, condominium prices plummeted by 9.4% in Q3 2024—the third largest

of the five quarterly contractions from 2020 to the present.

However,

as a proxy, the performance of the top five listed developers (SM Prime, Ayala

Land, Megaworld, Robinsons Land, and Vista Land) tells a different story. Their

Q3 2024 real estate sales surged by 19.76% YoY, suggesting no signs of

retrenchment in new property sales.

This

raises a critical question: Were the BSP numbers inaccurate, or have

property developers been overstating their real estate sales? (Figure 3 lowest

graph)

As

a side note, the property sales of the top five developers are not limited to

residential condos; however, the comparison provided is for estimation purposes

only.

Figure

4But

there’s more.

The

slowing rental income growth of the top four developers (SM Prime, Megaworld,

Robinsons Land, and Vista Land) appears to align with the moderating revenue

growth of the top six non-construction retail chains (SM Retail, Puregold,

Robinsons Retail, Metro Retail, SSI Group, and Philippine Seven). (Figure 4, topmost diagram)

In

Q3, rental income for developers increased by 7.12%, while retail chains saw 6%

growth. Both figures peaked in 2022 (Q2 and Q3, respectively) and have been on

a downtrend since.

This

slowdown also reflects the growing mismatch between sales

growth rates and the expansion of selling areas for retail chains

and shopping malls, which has resulted in increasing vacancies.

VI. Real Estate Deflation Amidst Near Full-Employment? What

Happens When Unemployment Soars?

Intriguingly,

despite unprecedented consumer bank borrowing rates and levels, the data signals

intensifying signs of strained consumers—despite the supposedly near-full

employment rate. (Figure 4, middle window)

This

also suggests that either the government’s labor data has been significantly

stretched, or that consumers are increasingly burdened by the sustained

loss of purchasing power in their wages and incomes, or by escalating balance

sheet leverage.

Worst

of all, it could be both.

What happens when the employment rate falls?

Even more important, what happens when consumer credit slows or even

retreats?

VII. Property Sector Woes: From Price Deflation to Income

Losses and Increased Debt Loads

Of

course, deflation in the industry translates to weakened demand.

While

property firms may attempt to mask this through possible overstatements of

sales, internal pressures—such as diminishing liquidity, rising debt burdens,

and increasing servicing costs—are likely to result in the eventual

emergence of losses.

When

deflation gripped the industry in 2020–2021, the top five developers recorded

net income losses over four quarters.(Figure 4, lowest chart)

Currently,

while net incomes are at all-time highs, their growth rate has been eroding.

Figure

5Furthermore,

debt levels continue to climb to record highs, accompanied by rising interest

rate expenses. On the other hand, cash reserves have recently dropped and

stagnated. (Figure 5, topmost and middle graphs)

Coming

down the pike, the likelihood of income deficits combined with a drain in

business liquidity may result in even greater reliance on debt financing to

sustain operations—even as collateral values deteriorate.

If

these developments have already impacted the top five developers, what more

for marginal industry players—the mom-and-pop operators?

VIII. Property Sector Woes: From Liquidity Strains to Soaring

Bank NPLs?

Considering

that banks hold significant exposure to real estate, the next phase will

likely result in a surge in non-performing loans (NPLs).

When

deflation engulfed the sector in 2020-2021, real estate consumer NPLs surged

and continued to rise even when the RREPI index peaked at 14.1% in Q2 2023. (Figure

5, lowest chart)

NPLs

hit a record Php 21.7 billion in Q2 2024 but slightly declined to Php 21.28

billion in Q3 2024.

Due

to credit expansion outpacing NPL growth, these numbers have been obscured as a

function of ratios. They will likely become more prominent once credit

expansion materially slows.

Or

what is likely to follow, after mounting losses and the depletion of liquidity,

is a rise in NPLs—starting with smaller players and gradually affecting

larger industry participants, in a "periphery-to-core" dynamic.

IX. Will the BSP Launch QE 2.0 Soon?

In

addition to surging public debt, the RREPI Q3 2024 deflation provides context

for the BSP’s recent actions, which mirror a shadow of the pandemic recession

playbook. These include the reduction of the Reserve Requirement Ratio (RRR)

from 9.5% to 7%, effective October 2024, and the ongoing easing cycle, marked by the second and third interest rate cuts in

the ONRRP in Q4 2024.

Furthermore,

it explains the record-high 11-month public expenditures, reflecting the "Marcos-nomics" fiscal stimulus

aimed at offsetting the decline in private sector demand.

Figure

6 These

policies have combined to momentarily bolster liquidity, which had been eroding

from 2021 to 2023, as reflected in the YoY changes in M1. (Figure 6, topmost

visual)

Lastly,

the Php 2.3 trillion injections by the BSP were partly channeled through its net claims on the central government (NCoCG).

Interestingly,

despite the supposed economic normalization, the BSP’s NCoCG remains elevated,

prompting the IMF to request that the BSP become more transparent about its

"balance sheet strategy."

For

instance, notes Inquirer.net,

"the IMF said the BSP may want to publish more information about the size

of its portfolio of government securities (GS), which remains 'substantial'

despite declining since the central bank’s large purchases of state bonds

during the COVID-19 pandemic."

The

BSP’s NCoCG stood at Php 650 billion as of November 2024, which is vastly above

its 2002-2019 monthly average of Php 32.7 billion. (Figure 6, middle chart)

The

BSP also holds Php 1.178 trillion worth of domestic

securities (as of September 2024), accounting for 14.6% of its total

portfolio. (Figure 6, lowest graph)

The

essence here is that by partly maintaining its quantitative easing (QE), the

BSP remains heavily involved in controlling liquidity conditions in the banking

system, where the real estate industry represents a significant counterparty.

This

signifies the 'ratchet effect theory' in action, where temporary solutions to

address specific problems become a permanent part of the legal landscape. (Matulef,

2023)

The

Php 64 trillion question is: should current developments in the real estate

sector deteriorate, would the BSP launch QE 2.0?

X. Conclusion: Two Ways to Bankruptcy: Gradually, then Suddenly

All

told, despite the profusion of liquidity and the embrace of easy money

policies, deflation in the Philippine real estate industry has emerged and could

worsen.

This

highlights the widening mismatch between vigorous debt-financed

supply-side growth and weakening consumer demand—primarily driven by the

erosion of the peso's purchasing power and the extended balance sheet leverage

resulting from trickle-down policies, including the crowding-out effect.

Although

the challenge for policymakers would be to allow market forces to take

command—cleansing household, corporate, and government balance sheets while

rebuilding savings through productive undertakings—this would translate to a

vastly diminished GDP and, more importantly, reduced political boondoggles. As

such, this route is unlikely to occur.

Nonetheless,

authorities are likely to "fight the last war" by pursuing

path-dependent, free-money policies aimed at boosting aggregate demand and GDP,

while ignoring all other factors.

Lastly,

because the consensus believes these trends represent a temporary phenomenon,

isolated from the pandemic's events and previous easy money policies, the

"build-and-they-will-come" mentality is likely to prevail, driving an

even greater debt-financed "race-to-build supply"—thereby

exacerbating existing imbalances.

As American

novelist Ernest Hemingway wrote in The Sun Also Rises:

"How

did you go bankrupt? Two ways. Gradually, then suddenly."

___

References:

Prudent Investor, Philippine Real Estate:Mainstream Expert Worried Over Increasing Demand-Supply Gap; Q1 2023 Data ofTop 5 Listed RE Firms and the Property Index, May 28, 2023

Bangko Sentral ng Pilipinas, Residential Real

Estate Prices Decline in Q3 2024, December 27, 2024, bsp.gov.ph

Michael

Matulef, Beyond

Crisis: The Ratchet Effect and the Erosion of Liberty August 18, 2023,

Mises.org

Ernest

Hemingway, The Sun also Rises

Chapter 13, 1926 Project Gutenberg Canada