The problem is not people being uneducated. The problem is that people are educated just enough to believe what they have been taught, and not educated enough to question anything from what they have been taught—Prof. Feynman (Twitter)

In this issue

What Surprise is in Store for the 2023 Year of the Water Rabbit?

I. Recalling the Year of the Tiger and the Outbreak of the Russia-Ukraine War

II. Year of the Rabbit: A Return to Global Peace in 2023? Or Will Geopolitical Strife Escalate?

III. Year of the Rabbit: A History of Mixed Global Financial and Economic Climate

IV. Which Force will Dominate China’s Economic Landscape: Reopening and the Housing Rescue Package or the Deflating Housing Bubble?

V. Will the Bank of Japan Overpower Market Forces or Will its Policies Backfire?

VI. Skating on Thin Ice: Inversions in Treasury Spreads of Advance Economies Herald a Global Recession?

VII. Has the Year of the Rabbit Been Favorable to The Philippines?

What Surprise is in Store for the 2023 Year of the Water Rabbit?

Chinese astrology believes that Rabbit year will bring about peace, rationality, and luck. We hope so. But history and current developments oppose such projections. Will the Rabbit prevail?

I. Recalling the Year of the Tiger and the Outbreak of the Russia-Ukraine War

Remember this? The following excerpt emanates from our post about a week before the Chinese New Year in 2022.

Aside from the eroding concerns over the pandemic, potential geopolitical flashpoints for a hot war may occur.

For instance, the US-Russian impasse over Ukraine (Russia’s vehement objection over the slippery slope of NATO’s expansion into her borders), China’s flexing of its military muscles over Taiwan (Figure 2, topmost pane) while simultaneously asserting its sphere of influence at the disputed territories of the South China Sea and the Senkaku Islands. There are also ongoing border disputes between China and India at the Himalayan Aksai Chin and the south of the McMahon Line and between India and Pakistan over Kashmir.

So yes, if diplomacy fails, the higher the risks that standoffs morph into a hot war.

The Year of Tiger has been no stranger to such events, historically.

…

Finally, with deteriorating economic growth, will governments shift the blame to other nations by escalating the geopolitical divide to preserve their hold on power?

Specifically, will the Communist Party of China advance its claim on territorial disputes or on Taiwan to save its skin? Will US Democrats push for a showdown with Russia over Ukraine to cover their plummeting approval ratings?

If so, will the 2022 Year of Tiger usher in Fat-Tailed risks? (Prudent Investor, 2022)

On February 24, 2022, or three weeks after our note, the Russian government launched a massive military campaign, which it called the Special Military Operation (SMO), against the NATO-supported Ukraine government.

People-driven events don't occur in a vacuum. Most are products of long-drawn political-economic processes. In the case of the Russo-Ukraine conflict, it represents a "hegemonic war" or a struggle over the dominance of the international distribution of power.

In our humble opinion, the conflict wasn't incited by the year of the tiger but instead coincided with it.

So, will the year of the rabbit bring forth peace?

Nota Bene: This author is agnostic on Feng-shui or zodiac signs. But the insights from these may not be from the zodiac signs but the cyclical episodes embedded in the evolution of the (international and domestic) political economy.

II. Year of the Rabbit: A Return to Global Peace in 2023? Or Will Geopolitical Strife Escalate?

But what does the Year of the Water Rabbit really mean for us? According to Chinese Astrology, the Rabbit represents peaceful and patient energy. The Rabbit is a gentle creature known for thinking things through before acting. This energy will encourage us to approach challenges and opportunities calmly and rationally.

In addition to the Rabbit’s peaceful energy, the Water element brings intuition and inner peace. Water is all about tapping into our inner wisdom and trusting our instincts. It encourages us to be more in tune with our emotions and sensitive to those around us. (The Chinese Zodiac, 2023)

Historical precedents indicate that the year of the rabbit hasn't been exactly peaceful.

World War II began in its watch with the invasion of the Hitler-led German government of Poland on September 1, 1939. Two days after, France and Germany declared war on the German government.

The assassination of former US President John F. Kennedy occurred in the year of the Water Rabbit in 1963.

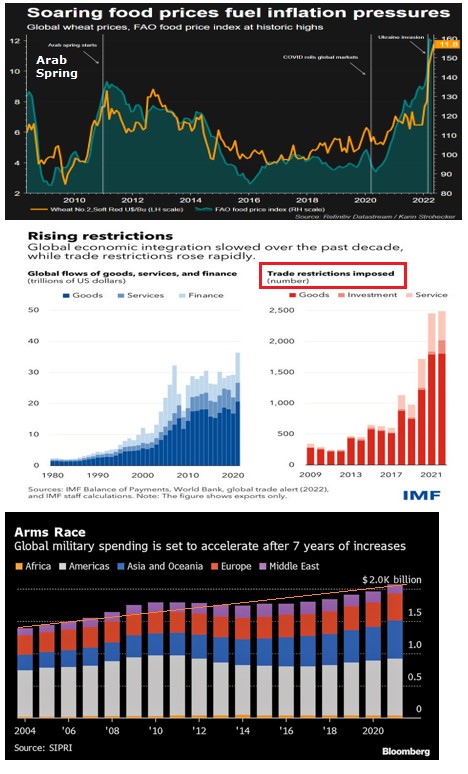

The Year of the Rabbit also saw the outbreak of the Arab Spring protests in 2011. Although the trigger for the unrest started with the self-immolation of a street vendor in Tunisia in December 2010, the social strife spread like wildfire throughout several Middle East nations in 2011 (Bahrain, Saudi Arabia, Egypt, Syria, Libya, Tunisia, United Arab Emirates, and Yemen).

Figure 1

One of the contributing factors could have been the surge in food prices. (Figure 1, topmost pane)

Yet, the most peaceful development in the Year of Rabbit occurred with the closure of the Vietnam war, which climaxed with the Fall of Saigon on April 30, 1975, highlighted by the final withdrawal of US troops and the unconditional surrender of the South Vietnamese government to its communist Northern rival.

Today, there are barely any signs that primary participants in the "hegemonic war" will sue for peace.

The lack of interest in negotiations by opposing parties, the sustained shipment of arms, the continued provocations and counter provocations, the widening coverage of the war to include economic and trade protectionism, and the weaponization of finance (US dollar) and commodities, and intensifying political propaganda—all point to mounting risks of escalation (nuclear exchange).

While trade protectionism has been on the rise, the war aggravated it. (Figure 1, middle chart)

Further, with the global economy skating on thin ice, wars serve as a convenient scapegoat to extend or expand the political tenures of the leaders.

Even worse, with expanding vested interests of the politically influential "triumvirate" sectors, perhaps the backbone of the deep state—the military-industrial complex, oil and energy, and finance industries—benefiting immensely from the "proxy" conflict, amicable settlement becomes less of an option for their political leaders.

The surprising path that may end the war this year is when one party succeeds in subjugating the other.

But from our understanding, one of the protagonists has been engaged in a grinding "war of attrition."

Perhaps, this excerpt from a CNN op-ed represents the zeitgeist of the present state of geopolitics.

It’s an arms race bigger than anything Asia has ever seen – three major nuclear powers and one fast-developing one, the world’s three biggest economies and decades-old alliances all vying for an edge in some of the world’s most contested land and sea areas.

In one corner are the United States and its allies Japan and South Korea. In another corner, China and its partner Russia. And in a third, North Korea.

With each wanting to be one step ahead of the others, all are caught in a vicious circle that is spinning out of control. After all, one man’s deterrence is another man’s escalation. (CNN, 2023)

So, the roadmap to a truce is as elusive as the warring factions' demonstrated preference (choice of actions).

Will the essence of the rabbit change their priorities? How?

III. Year of the Rabbit: A History of Mixed Global Financial and Economic Climate

Let us move on to the economic and financial world.

The Year of the Rabbit showed some silver lining in this space.

In the economy, the Year of the Rabbit coincided with the end of the Great Depression in 1939. It also saw the terminal phase of the 1973-1975 US recession.

But in finance, the Year of the Rabbit hosted the biggest stock market crash (in %) in the US: Black Monday, October 19, 1987.

The embedded risks vented via economic and financial volatilities have hardly subsided from last year.

Although the world appears to be banking on a goldilocks outcome—the tempering of inflation amidst a mild economic downturn—decades of malinvestments, outsized debt growth, "higher for longer" inflation and interest rates, hissing asset bubbles, public spending increasingly diverted into the defense industry, the accelerated developments of geopolitical, economic, and financial "fragmentation" (diminished cooperation and collaboration) instead magnify the risk profiles of the world. (Defense industry spending, Figure 1, lowest window)

And once again, geopolitical evolution will have a significant role in shaping the global economic, financial and monetary landscape. Credit Suisse Zoltan Pozsar gives us a clue.

If we are drifting from a unipolar world to this multipolar one, and if the G20 fractures into the camps of the G7 plus Australia, Brics+ and the non-aligned, it’s impossible that these rifts will not affect the international monetary system. Growing macroeconomic imbalances in the US further add to these risks.

The dollar-based monetary order is already being challenged in multiple ways, but two in particular stand out: the spread of de-dollarisation efforts and central bank digital currencies (CBDCs). (Pozsar, 2023)

(Even) Assuming that only a part of this scenario comes true, will the ensuing feedback loops or the transitional phase be smooth, disorderly, or a mixture of both?

Or, to what extent will these developments impact the Year of the Rabbit?

IV. Which Force will Dominate China’s Economic Landscape: Reopening and the Housing Rescue Package or the Deflating Housing Bubble?

In the meantime, let us scan the international risk climate.

China's deflating property bubbles remain a critical concern.

Public unrest compelled authorities to abandon its rigid Zero-Covid policies abruptly. But that could have signified the surface only.

Figure 2

The communist leadership, perhaps, realized that constricted mobility could worsen its dire real estate conditions that could trigger a financial crisis.

The heavily levered property sector accounted for about 45% of household net worth (2019 estimates) and could represent the largest asset class in the world. (Figure 2, topmost chart)

So, the Chinese authorities have not only "reopened," they launched a massive rescue package for the industry.

The property sector has languished in 2022, as exhibited by the negative growth of the average home price index. (Figure 2, middle pane)

Likewise, authorities reported that their GDP grew by 2.9% in 2022, the lowest in 46 years.

A slump in economic growth diminishes the ability of households and firms to support mortgages and acquire new property.

So, last week, its central bank, the PBoC, flooded the banking system with unprecedented liquidity. (Figure 2, lowest chart)

And though this may perk up activities in the interim, its benefits will likely fade out. And thus, the need for repeat injections will arise. Yet, authorities appear to be buying for time.

The thing is, how will the reopening and liquidity infusions impact the global marketplace and the economy in 2023? Will China "export" inflation? Or will the unfolding housing bust dominate?

V. Will the Bank of Japan Overpower Market Forces or Will its Policies Backfire?

And then, the attempt by the Japanese government through its central bank, the Bank of Japan (BoJ), to sustain its easy money regime via Yield Curve Control (YCC).

Its ramifications include the sharp weakening of the yen, draining the Japanese Government Bond (JGB) market of liquidity (as the BoJ monetized a record amount of public debt to inflate its assets), the combusting of inflation (December inflation reached a 41-year high!), and the market forcing the BoJ to raise its cap on the curve. (Figure 3)

Despite this, the yen recently has tagged along with its peers to stage a substantial rally against the USD.

So, will the BoJ succeed in its derring-do campaign to trample market forces and maintain its easy money regime? Or will risks via unforeseen consequences emerge in the Year of the Rabbit, which could ripple into the world?

Something has got to give.

VI. Skating on Thin Ice: Inversions in Treasury Spreads of Advance Economies Herald a Global Recession?

The economies of other developed countries (the US and Europe) have been struggling too.

And inverting bond markets have been signaling the likelihood of a recession.

Figure 4

Lately, the inversion has covered 90% of the US yield curve (higher short-term yields relative to the long-term), while the spread of the 2-and 10-year German bund has also turned negative. (Figure 4, topmost and second to the highest window)

And as central banks sop liquidity off the marketplace through higher rates, housing prices fell in response. The marginal decline in the ECB's assets have also prompted a plunge in Germany's housing prices. And the global housing bubble appears to have been pricked. (Figure 4, second to the lowest and lowest charts)

The IMF also predicts that a third of the world will fall into recession this year, which means many emerging markets will be affected.

If so, how will their central banks and political leadership respond? Will they be immersed in foolhardy policies such as bold fiscal stimulus financed by the printing press of their central banks?

The point of these is that risks have been mounting from multiple fronts.

Will the Water Rabbit be lucky enough to defer or alter the possible outcomes?

VII. Has the Year of the Rabbit Been Favorable to The Philippines?

Has the Year of the Rabbit been favorable to the Philippines?

As for political events, 1987, 1999, and 2011 signified post-presidential elections years.

But on August 28, 1987, the Reform the Armed Forces Movement (RAM) launched a deadly but unsuccessful coup attempt against the newly seated Aquino Government that resulted in 53 deaths and more than 200 wounded.

Other than the botched coup attempt, the political events of these years were not as compelling to be of note.

How about the domestic economy and financial markets?

Figure 5

Inflation signified the defining characteristic of the Rabbit year.

The contrasting eras (inflation and deflation) underlying the year didn't matter. The highest CPI of 7.6% occurred in 1963, which like today, represents the year of the Water Rabbit. (Figure 5, topmost window)

The average CPI of the last five Rabbit years was 5.5%.

Another hallmark of the year was the unanimity of positive returns of the USD Php. (Figure 5, second to the highest chart)

But the 2011 gain of .1% was almost negligible and seemingly representative of declining returns. The high inflation rates have likely been the primary driver of the positive returns in the USD Php.

As an aside, the USD Php data was based on the BSP's end-of-period calculation.

Another key feature of the five Rabbit years appears to be the diminishing returns of the GDP. (Figure 5, second to the lowest chart)

The high rates of the headline GDP of the earlier years had mainly been due to the Nominal GDP—powered by high rates of the CPI.

The average GDP of the last five Rabbit years was 4.82%.

Finally, another vital aspect of the Year of the Rabbit has been extensive volatility in stock market returns. (Figure 5, lowest window)

On the positive side, 1963's 138.4% equity headline returns ranked the fourth highest, while 1987's 91.4% was the sixth highest since 1959.

On the other hand, the PSEi 30 (previously the Phisix) suffered a 29.3% deficit in 1975.

Since 1987, the rate of return of the headline bellwether reflected the overall long-term dynamic of diminishing returns. The PSEi 30 posted returns of 8.9% and 4.1% in 1999 and 2011, respectively.

Nonetheless, the average return of the five Rabbit years was 42.8%.

Will the elements of high inflation, positive but diminishing returns of the USD-Php and GDP, as well as the extensive volatility of the stock market, be carried over to the Rabbit year of 2023?

___

References

Prudent Investor Newsletter, What Surprise is in Store for the 2022 Year of the Water Tiger? January 23, 2022

The Chinese Zodiac, The Year of the Rabbit, 2023, thechinesezodiac.org

Lendon, Brad Why Asia’s arms race risks spinning out of control, January 15, 2023, CNN.com

Poszar, Zoltan Great power conflict puts the dollar’s exorbitant privilege under threat Financial Times, January 20,2023