Balance of payments crises are created in (soft) pegged arrangement because the monetary authority simultaneously targets both the exchange rate and interest rate and fails on both counts—Steve Hanke

In this issue

How the BSP's Soft Peg will Contribute to the Weakening of the US Dollar-Philippine Peso Exchange Rate

I. Closing 2024: Major Interventions Boost the Philippine Peso and PSEi 30

II. A Brief History of the USDPHP's Soft Peg

III. USDPHP Peg: Tactical Policy Measures: Magnifying Systemic Risks

IV. The Cost of Cheap Dollars: Financing Challenges and Soaring External Debt

V. USDPHP Peg: The Other Consequences

How the BSP's Soft Peg will Contribute to the Weakening of the US Dollar-Philippine Peso Exchange Rate

The Philippine peso mounted a strong rally in the last week of 2024, a hallmark of the BSP's defense of the USDPHP soft-peg regime. Why such policies would boost it past 60!

I Closing 2024: Major Interventions Boost the Philippine Peso and PSEi 30

In the last week of December, I proposed in a tweet that the BSP and their "national team" cohorts might engage in "painting the tape" to boost Philippine asset prices during the final two trading sessions of the year.

The BSP and their Philippine "national team" have 2 days left in 2024 to steepen Treasury markets, limit $USDPHP gains, and boost #PSEi30 returns after Friday's massive 5 minute pre-closing pump (correction: should have been Monday instead of Friday)

Figure 1

This post turned out to be prescient. The "national team" apparently didn’t allow any major corrections on the PSEi 30 following Monday’s powerful 5-minute pump, subsequently, following it up with another two-day massive pre-closing rescue pump. (Figure 1, topmost charts)

However, the USD Philippine peso exchange rate (USDPHP) market exhibited even more prominent interventions. Despite the USD surging against 19 out of 28 pairs, based on Exante Data, the Philippine peso stood out by defying this trend, delivering the most outstanding return on December 26th. It was a mixed showing for the other ASEAN currencies. (Figure 1, middle table)

On that day too, the USDPHP traded at its lowest level from the opening and throughout the session, with depressed volatility—a clear indication of an intraday price ceiling set by the market maker, or possibly the BSP. (Figure 1, lowest graph)

By the last trading day of the year, the USDPHP weakened further, resulting in an impressive 1.64% decline over three trading sessions!

Figure 2

Notably, the Philippine peso emerged as the best-performing Asian currency during the final trading week of the year. Still, the USDPHP delivered a 4.47% return compared to the PSEi 30’s 1.22%. (Figure 2)

Figure 3

Over the past 12 years, the USDPHP has outperformed the PSEi 30 in 9 of them. Given its current momentum, this trend is likely to persist into 2025. (Figure 3, upper chart)

It is crucial to understand that such price interventions are not innocuous; they have lasting effects on the market and the broader economy.

II. A Brief History of the USDPHP's Soft Peg

The BSP employed a ‘soft peg’ or limited the rise of the USDPHP back in 2004-2005 (56.4 in 2004 and 56 in 2005). (Figure 3, lower image)

Because of the relatively clean balance sheet following the post-Asian Crisis reforms, the BSP seemed successful—the peso rallied strongly from 2005 to 2007.

Despite the interim spike in the USDPHP during the Great Financial Crisis (GFC), it fell back to the 2007 low levels in 2013. This episode marked both the culmination of the strength of the Philippine peso and its reversal: the 12-year uptrend for the USDPHP.

Figure 4

Thanks to the expanded deployment of new tools called Other Reserve Assets (ORA), the BSP managed to generate substantial gains for the Philippine peso from 2018 to 2021. (Figure 4, upper window)

ORA includes financial derivatives (forwards, futures, swaps, and options), repos, and other short-term FX loans and assets.

However, this did not last, as the BSP launched a multi-pronged bailout of the banking system in response to the pandemic recession. The bailout comprised Php 2.3 trillion in injections (Quantitative Easing via Net claims on Central Government), aggressive RRR cuts, historic interest rate reductions, and various capital and regulatory relief measures, including subsidies. (Figure 4, lower diagram)

The USDPHP soared by about 5.4% from its 2004-2005 cap to reach the 59 level, marking the second series of its soft peg.

The USDPHP hit the 59 level four times in October 2022.

This second phase of USDPHP soft peg signified a part of the pandemic bailout measures.

Fast forward today, as the BSP maintained its implicit support via relatively elevated net claims on central government (NCoCG), the USDPHP’s 2023 countertrend rally was short-lived and rebounded through June 2024.

Promises of easy money from both the US Fed and the BSP sent a risk-on signal for global assets, including those in the Philippines sent the USDPHP tumbling to its low in September 2024.

Unfortunately, renewed signs of ‘tightening’ sent it re-testing the 59 levels three times in November-December 2024.

In short, despite recent interventions to maintain the 59 level, the numerous attempts to breach it signal the growing mismatch between the BSP’s soft peg and market forces.

III. USDPHP Peg: Tactical Policy Measures: Magnifying Systemic Risks

Yet, the BSP’s upper band limit signifies a subsidy on the USD or a price distortion that undervalues the USD while simultaneously overvaluing the peso.

This policy impacts the economy in several significant ways.

Widening Trade Deficit: First, the cap widens the trade deficit by making imports appear cheaper and exports more expensive. An artificial ceiling exacerbates imbalances stemming from the historical credit-financed savings-investment gap.

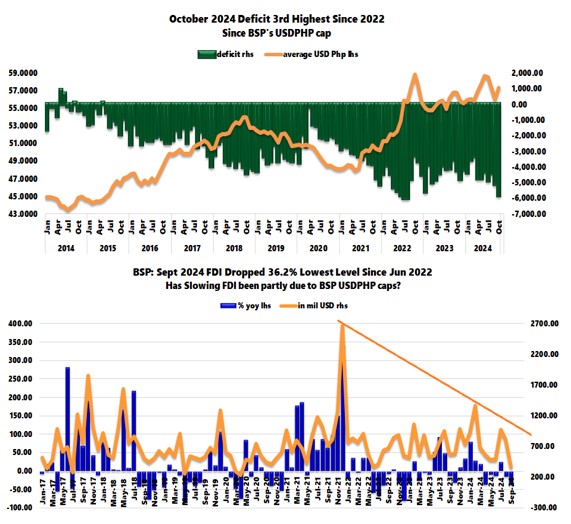

Figure 5

It is no surprise that the trade deficit hit its all-time high in the second half of 2022 as the BSP cap went into effect.

Meanwhile, in October 2024, the trade deficit reached its third highest on record, following the USDPHP run-up through June 2024 with a quasi-upper band limit of 58.8-58.9. The USDPHP hit the 59 level twice in October. (Figure 5, upper chart)

Reduced Tourism Competitiveness: Second, an artificially strong peso (due to the cap) could make the Philippines a more expensive destination for tourists. This could reduce the country’s competitiveness in the tourism sector, ultimately impacting tourism revenue negatively.

Resource Misallocation: Third, prolonged price distortions lead to resource misallocations. In the short term, an overvalued currency might fuel consumption-driven growth due to cheaper imports. However, businesses may over-import because of the cheap USD, while exporters face challenges, with some potentially shutting down, resulting in job losses.

Over time, this could lead to overinvestment in import-related and dependent sectors while underinvestment could spur declining competitiveness in exports and tourism-related industries. These represent only the first-order effects.

The intertemporal ripple effects extend through supply and demand chains, compounding the long-term economic impact.

Inflation Risks: Fourth, the policy could exacerbate domestic inflation. While one goal of the cap is to suppress rising import costs, dwindling reserves make defending the cap increasingly difficult. Once reserves are depleted, the risk of abrupt devaluation grows, potentially defeating the policy’s original purpose.

Reduced Foreign Direct Investment (FDI): Fifth, pricier peso assets and heightened inflation risks translate to higher ‘hurdle rates’ for Foreign Direct Investments (FDI). This diminishes competitiveness and results in slow or stagnant FDI inflows, hindering long-term economic growth. Since peaking in December 2021, FDI flows have been stagnating and have shown formative signs of a downtrend since falling most last September 2024. (Figure 5, lower graph)

Increased Market Volatility: Sixth, the artificial ceiling could inadvertently magnify market volatility. Although designed to maintain stability, the widening misalignment between the USDPHP and economic fundamentals may prompt speculative pressures. If markets perceive the cap as unsustainable, the result could be a destabilizing devaluation.

Capital Flight and Financial Instability: Finally, the growing perception of an imminent, sharp devaluation might spur capital flight from prolonged price controls, increasing the risks of financial instability.

The Long-Term Costs of Short-Term Policies: Tactical policy measures, such as an artificial cap, magnify risks over time. These stop-gap measures are not "free lunches." Instead, they increase economic inefficiencies, contribute to stagnation, and amplify systemic risks.

IV. The Cost of Cheap Dollars: Financing Challenges and Soaring External Debt

On top of that, there is the critical issue of financing.

>By keeping the dollar artificially cheap, authorities ENCOURAGE USD debt accumulation. This policy may amplify medium- to long-term vulnerabilities, particularly in the face of rising global interest rates or a stronger dollar.

>Depleting Reserves and Surging External Debt: The artificial ceiling requires substantial central bank intervention through the use of foreign reserves. However, prolonged interventions deplete these reserves and may compel the government to borrow externally to replenish them, thereby increasing public debt.

Unsurprisingly, external debt soared in Q3 2024.

What’s more, since the National Government’s (NG) net foreign currency deposits with the BSP include proceeds from the NG's issuance of ROP Global Bonds, external debt inflates the BSP’s Gross International Reserves (GIR).

Figure 6

Still, the level and growth of Q3 external debt continue to outpace the GIR. (Figure 6, topmost image)

As a side note, GIR fell by USD 2.6 billion to USD 108.5 billion last November.

>Increasing Refinancing and Liquidity Strains:

As I recently noted,

rising external debt compounds the government’s predicament, as the lack of revenues necessitates repeated cycles of increased borrowing to fund gaps in the BSP-Banking system’s maturity transformation, creating a "synthetic US dollar short." (Prudent Investor, November 2024)

Increasing requirements for refinancing have only magnified the US dollar shortage, amplifying a race to borrow that heightens the risk of abrupt exchange rate adjustments or repayment shocks.

Additionally, banks (+34.14% YoY) and non-financial institutions (+5.5%) have also been ramping up their external debt. However, government borrowings (+18.7%) continue to outpace those of the private sector (in mil USD). (Figure 6, middle diagram)

>Growing Short-Term Debt Concerns: Worse yet, while the BSP describes the present growth pace of external debt as "sustainable," short-term external debt has hit a record, and its share of the total has also expanded in Q3. (Figure 6, lowest window)

The rapid rise in short-term debt is a symptom of mounting US "dollar shorts" or developing liquidity strains, which are likely to be magnified by the BSP’s caps.

>Rising Debt Crisis Risk: Although one implicit objective of maintaining a USDPHP cap is to artificially lower the cost of debt servicing, the removal of this cap or an eventual devaluation could cause the cost of servicing foreign-denominated debt to skyrocket in local currency terms, potentially triggering a debt crisis.

Figure 7

Eleven-month debt servicing costs have already hit a record (compared with same period and against the annual), partly due to the increasing share of foreign-denominated debt. Imagine where these costs would land if the USDPHP exchange rate breaches the 60 level!

V. USDPHP Peg: The Other Consequences

And that’s not all.

The artificial peg may lead to additional consequences:

>Moral Hazard: Economic actors might engage in risky financial behavior, such as excessive USD borrowing, expecting government intervention to shield them from losses by perpetually maintaining a cheap dollar policy.

>Policy Tradeoffs: The BSP’s prioritization of exchange rate stability could worsen imbalances brought about by past and present monetary policy stances.

>Black Market Emergence: As USD supply becomes restricted due to prolonged interventions, a parallel or black market for the dollar may emerge.

>Social Inequality: The benefits of an artificially cheap dollar often skew toward wealthier individuals, who gain access to inexpensive foreign goods and international investment opportunities. In contrast, low-income households may face rising prices for basic goods—especially domestically produced ones—because local producers struggle with higher input costs or reduced competitiveness.

>Economic Inequality: Moreover, such policies disproportionately favor certain groups, such as importers or holders of foreign currency-denominated assets (and related industries), and USD borrowers, at the expense of others, including exporters, local producers and savers.

>Trade Relations and Currency Manipulation Risks: A significant trade deficit driven by an undervalued dollar could strain trade relationships, potentially inviting retaliatory measures from trading partners or complicating trade negotiations.

In extreme cases, accusations of "currency manipulation" could lead to sanctions by organizations such as the WTO. These sanctions might allow affected countries to impose tariffs on imports from the Philippines.

All these factors point to one conclusion: the USDPHP is likely headed past 60 soon.

____

References

Prudent Investor US Dollar-Philippine Peso Retests Its All-Time High of 59, the BSP’s "Maginot Line": It’s Not About the Strong Dollar November 25, 2024